Source: TradingView, CNBC, Bloomberg, Messari

Consensus was wrong for 2 straight years!

Over the last few years, we’ve released annual predictions focused on the source of growth, and potential risks, for digital assets. Over the years, we got a few big ideas right, and a few things very wrong:

What’s most interesting about the last two years is that consensus was dead wrong in 2022, and somehow even more wrong again in 2023. In a Deutsche Bank survey at the beginning of 2022, only 19% expected a negative return for the S&P 500 in 2022, and only 3% thought the return would be less than -15%. The S&P 500 ultimately lost -19.6%. In 2023, the same survey from DB showed that 39% expected a negative return of more than 10% for the S&P 500, and of course the S&P 500 ultimately rose +24.23%.

Consensus expectations for digital assets are a little harder to summarize, but it’s safe to say that very few expected digital assets to crash as far as they did in 2022, and almost no one predicted that digital assets would be the best performing asset class in 2023, with near triple-digit returns. Heading into 2024, there are perhaps more obvious reasons for optimism, but also still plenty of reasons for skepticism. Overall, we believe investors will continue to be rewarded in 2024 for investing in this asset class.

But in order to navigate the many ups and downs throughout the year, we must correctly pick the themes and narratives that will drive performance. Admittedly, many of these will change as the year progresses.

Prediction #1: Bitcoin is no longer boring, and will once again outperform most stocks, while owning Bitcoin mining stocks will once again outperform Bitcoin

Like most who entered the digital assets industry prior to 2018, the first blockchain network I ever used was Bitcoin when I first purchased BTC. It made sense from both a technology and a macro perspective, especially when there were no other established use cases for blockchain technology at that point. But over the past six years, our investing focus predominantly shifted towards other applications and sectors that were enabled via smart contract protocols. Quite frankly, Bitcoin became a boring financial asset that maybe you owned, but certainly didn’t need to discuss or research, because it never changed. Whereas the growth of NFTs, stablecoins, DeFi and much more was being built on other chains, and required constant analysis and education.

That changed in 2023. Throughout the year, we

discussed and debated Bitcoin more than any other asset and chain, starting with reasons to own it (March regional banking crisis, Blackrock Bitcoin ETF application) followed by new technological innovations (inscriptions, Ordinals). As a result, Bitcoin is no longer boring, and there are several reasons to own BTC and Bitcoin-related assets, starting with the most obvious, to the least obvious:

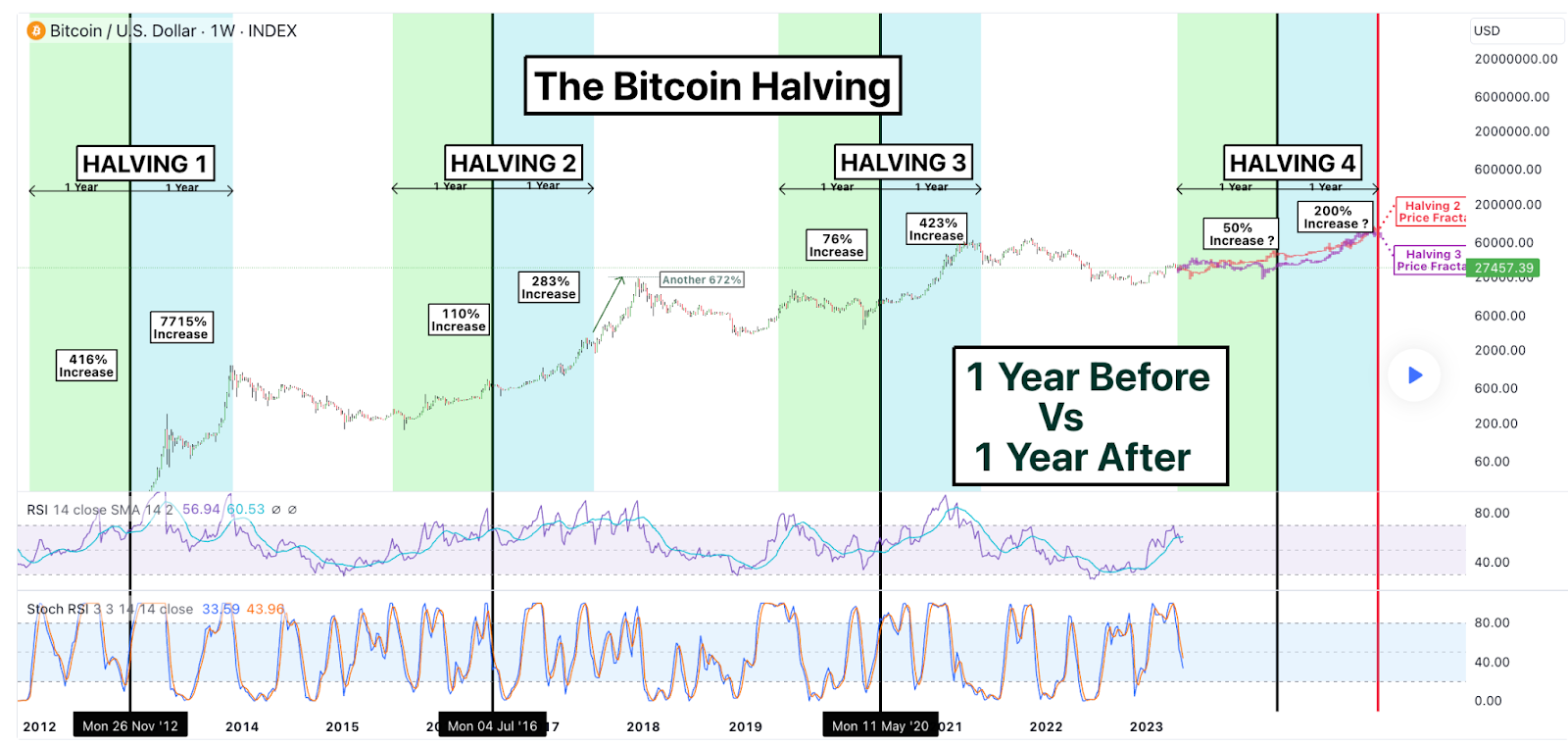

- There have been three prior Bitcoin halvings, and all of them have preceded large gains in price. You don’t necessarily have to believe that the halving changes anything fundamental (I certainly do not), but it has become a self-fulfilling prophecy at this point. The Bitcoin halving in April 2024 is widely viewed as a catalyst.

- The Bitcoin spot ETFs that are going to be approved imminently will spark demand from new investors, primarily financial advisors and RIAs. I expect there to be a knee-jerk reaction higher upon the actual approval, largely led by algos, which will last several days, and then ultimately price will stall until the ETFs actually begin accumulating assets. The second half of 2024 will likely see larger gains than the first half. Over 30% of total Bitcoin supply hasn't moved in five years, which may contribute to a liquidity squeeze as ETF issuers scramble to buy Bitcoin upon each new ETF creation.

- The U.S. presidential election in November combined with expectations of 3-5 rate cuts should provide a boost to all risk assets, as inflation will take a back seat to politics. Bitcoin more than any other asset remains hyper-sensitive to macro liquidity conditions.

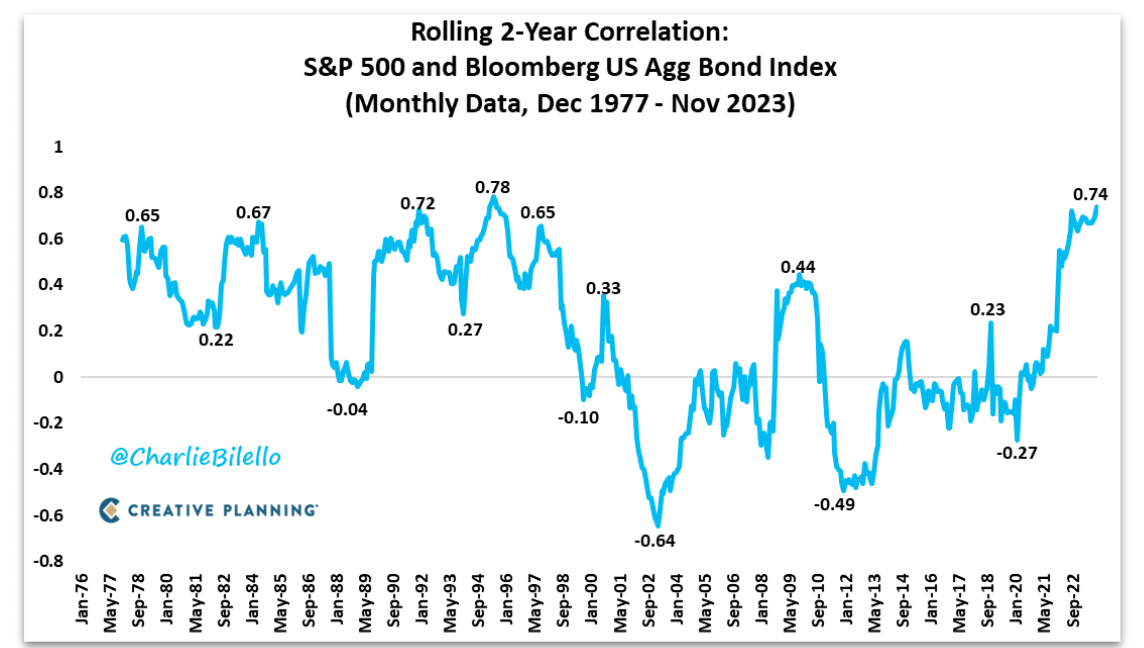

- The 60/40 portfolio is dead, and has been for over two years. The correlation between U.S. stocks and bonds over the last 2 years is the highest we've seen since 1993-95. The financial advisory world is built upon portfolio construction with uncorrelated assets, and if bonds and stocks no longer provide negative correlations, new financial assets will be pitched for inclusion in model portfolios. And there is no asset with higher returns and lower correlations than Bitcoin. The Bitcoin ETFs will naturally slide into every modern portfolio allocation.

- The long awaited Mt. Gox bankruptcy distributions will not impact the price of Bitcoin. While 142,000 BTC (>$6 billion) is expected to be distributed this year to creditors, most of this will not be sold. First, a large chunk of Mt. Gox claims has been purchased by distressed investors over the past five years and much of the Bitcoin price risk has been hedged already. Second, anyone who owned Bitcoin as early as 2013, and has held their bankruptcy claim for 10 years, is likely a blockchain and Bitcoin enthusiast so there is no reason to believe that the majority of creditors will sell an asset that they cherish regardless of how much price has increased. Third, Bitcoin Cash (BCH) forked from Bitcoin right after Mt. Gox filed for bankruptcy, which means that 143,000 BCH will also be distributed. Very few (if any) original BTC holders care about BCH, so it is far more likely that the BCH will be sold immediately than BTC.

- Bitcoin mining stocks (i.e. MARA, RIOT, CLSK, CIFR, BITF, IREN, etc) will outperform BTC again in 2024. Mining stocks were collectively up 399% in 2023 (compared to BTC +155%). Whereas historically a BTC halving would be bad for miners since the block subsidy (historically 98% of miner revenue) will be cut in half, this will be less of a problem now due to the rise of Ordinals and BRC-20s which has become a major portion of mining revenues. Mining stocks used to be very simple to analyze – fixed costs versus variable revenues that fluctuates with the price of BTC – but equity analysts now need to account for these other revenue streams, something that has yet to happen. Bitcoin’s transaction fees soared to an all-time daily high in the 4Q of 2023, driven by BRC-20 transactions and fungible memecoins issued using the Ordinals protocol.

Prediction #2: Tokenizing Real-World Assets (RWAs) will happen, but not until you can trade tokens, stocks and bonds all in one place

Tokenization of RWAs was one of the most talked about new narratives in 2023. But the data is misleading.

Tokenizing real-world assets is meant to include the tokenization of everything from financial assets to real estate to individual belongings like art and jewelry. In theory, by converting physical assets into digital tokens, blockchain provides enhanced liquidity, transparency, and efficiency. This innovation would allow for fractional ownership, broader distribution, and easier access to investments that were traditionally illiquid or exclusive. The secure, immutable nature of blockchain transactions, coupled with the potential for smart contracts to automate and streamline processes, further entices institutional adoption, signaling a new era of asset management and investment.

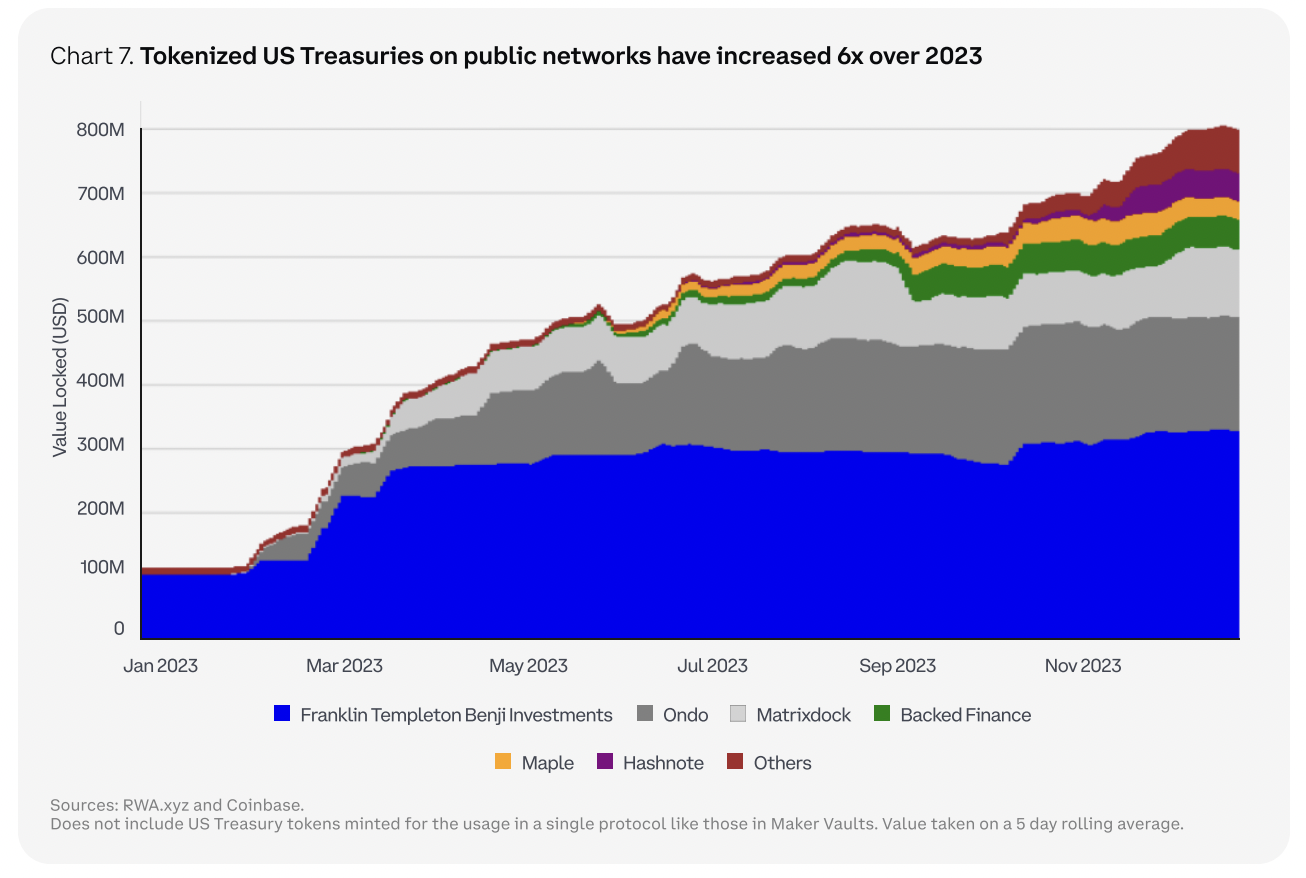

While the promise of RWAs is broad, what has occurred to date is the rise of tokenized U.S. Treasuries. And the reason for doing this is not any of the above, but that DeFi applications and on-chain stablecoin issuers are flush with cash that they cannot invest outside of the blockchain ecosystem. With rising U.S. Treasury yields, tokenized Treasuries provide them with an on-chain solution. The market for on-chain U.S. Treasury-based yield bearing

tokens increased 7x in 2023 to $832 million. This is great, but it is one VERY specific example of tokenizing real-world assets, and not at all solving for any of the inefficiencies of the traditional financial system.

At the moment, only people that are already in the crypto ecosystem care about tokenization of RWAs, specifically U.S. Treasuries, because it solves a particular use case for them. For the broader world to care, tokenized RWAs must offer a compelling value proposition. One or both of these conditions will have to occur:

- Someone tokenizes an asset that has real demand. Tokenizing a one-off hotel property didn’t excite anyone. Tokenizing an NBA contract didn’t excite anyone. But if you tokenize something of actual value to people – like Apple stock, or the Mona Lisa, or project finance debt for a municipality that comes with perks for its residents if you own the token – then you can generate new demand. Tokenization for the sake of tokenization isn’t going to drive demand.

- A bit chicken-and-egg, but as long as the brokerage world and the crypto world are completely separate, there is no need to tokenize anything. Ultimately, all assets need to be ownable and tradable on-chain, or none should be. Those with brokerage accounts don’t need to go on-chain for stocks and bonds, and those who are entirely on-chain aren’t a big enough financial audience to entice tokenization of brokerage assets. The real value driver is when you can bring ALL of your valuable assets onto the same layer such that you transcend the traditional barriers for liquidity and outreach. For example, selling a collector’s item car on-chain to the mass market, borrowing against your property using DeFi rates of 2-3% APR (versus market rates worldwide of 5-30%), or spending “money” as a pro-rata reduction of all of your assets. Money is online, communication is online, news is online...the world is now online. But money and assets are still separated, and that simply doesn’t work.

Prediction #3: This is the last “supercycle” for digital assets before TradFi normalizes the industry, and returns

The parallels between 2019 and 2023 are growing, with sentiment hitting rock-bottom, followed by a Bitcoin resurgence, and ultimately a rise of other layer-1 protocols and applications. After BTC outperformed everything in 2019, we saw the rise of DeFi, Stablecoins and ultimately NFTs in 2020-2021. Ultimately, 2024 may follow in 2020’s footsteps with a resurgence of decentralized applications, and a few new sectors emerging.

We are seeing a similar environment developing currently and are possibly on the verge of another huge upswing in adoption and subsequent appreciation in digital assets. One of the major headwinds, concern about regulation here in the U.S., may become a tailwind, meaning that as the regulatory environment becomes clearer and TradFi players become more comfortable, this could bring a huge amount of new capital into the ecosystem. After this last “supercycle,” returns may become more normalized.

While the libertarian dream of crypto with no rules and no government sounded good in theory, in order for digital assets to truly exist, it was inevitable that Wall Street would get involved and we’re beginning to see this happen.

- Blackrock, the world’s largest asset manager, will likely be managing the largest BTC fund (an ETF) by the end of the year.

- Citadel Securities, Jane Street, Goldman Sachs and others will become the biggest market makers.

- BNY Mellon will become the largest custodian of Bitcoin.

- The CME has already overtaken Binance in Bitcoin futures volume.

- The next wave of digital asset issuance will likely be from corporations, municipalities and universities, and underwritten by investment banks. To date, most tokens have been issued by decentralized and/or jurisdictionally ambiguous entities to date, however, token issuance from companies, municipalities and universities as tokens help align stakeholder incentives.

But in 2024, the bulk of the focus and institutional money will be into BTC via the new ETFs. The rest of the digital assets industry will still be a blip on most investors’ radars, and will likely remain too small for the majority of investors. As such, for the next 12-24 months, digital assets can still produce outsized returns for the small subset of non-Bitcoin digital assets investors. Following this expected surge, I believe the rest of the industry will become institutionalized as well. For 2024, however, investors will still be able to have early access to airdrops, rewards, and parse on-chain data. For one more cycle, the old investing style will still work, but soon, too many eyeballs and homogenous valuation techniques will shrink returns.

Prediction #4: Interoperability solutions will improve

Ultimately, no one really cares what chain they are on, nor should they. Interoperability between chains was a theme we focused on last year, but the focus has shifted from layer-1 and layer-0 chains (such as Cosmos and Polkadot) to the middleware providers (Chainlink CCIP, Layer Zero OFT, Circle’s CCTP etc). In the last two years we’ve seen a rise in the number of new layer-1s and layer-2s which overall leads to fragmentation in the market. Although users have greater options in terms of new chains that are faster and less expensive, they now run into the problem that there is a general lack of compatibility. Not all chains talk to each other and quite a few are incompatible for simply passing assets back and forth. The rise in bridge exploits illustrates the weakness in this area and the need for technology that doesn’t rely on pegged assets.

Imagine if you could only send emails between two Yahoo Mail users, or between two Gmail users. Or imagine if you could only play video games between people using the same game consoles or phones. It wouldn’t work, and it doesn’t in the blockchain world either. End users should not have to pick which chain they are on in order to use blockchain applications.

For institutions entering the space, they will want technology that is more seamless without security risks. A huge focus to date is on issuing assets of their own that are compatible in many different environments including the crop of existing public blockchains as well as private enterprise versions (e.g. JP Morgan’s blockchain, Figure’s Provenance blockchain).

While the ultimate solution isn’t necessarily obvious, one or more solutions need to become the norm in order for increased usage to flourish.

Prediction #5: User experience will finally improve, leading to some killer apps in Gaming, AI and DePIN

In the early days of the internet, users relied on IP addresses to connect to different sites. These were strings of numbers that, to the everyday user, meant nothing. In late 1987, the U.S. Advanced Research Projects Agency Network had two proposals, RFC 1034 and RFC 1035. These were the start of the Domain Name Service. DNS, as it’s called, transformed those strings of numbers into names, such as amazon.com. This transformation made the internet far more usable and searchable for billions today.

In 2023, digital assets had a similar proposal with the introduction of ERC-4337, creating “smart accounts.” These are designed to simplify the user experience in web3 radically. With a smart account, users don’t need a seed phrase, they don’t need to download a browser extension, and in many cases, they don’t need to pay gas for speedier transactions.

Solutions like this are needed before the majority of new users will be comfortable on-chain. But the question remains - will we see a killer app come before user experience and infrastructure improve, or will better user experiences and infrastructure lead to killer apps? From the

Myth of the Infrastructure Phase:

“A common narrative in the web3 community is that we are in an infrastructure phase and the right thing to be working on right now is building out that infrastructure: better base chains, better interchain interoperability, better clients, wallets and browsers. The rationale is: first we need tools that make it easy to build and use apps that run on blockchains, and once we have those tools, then we can get started building those apps. But when we talk to founders who are building infrastructure, we keep hearing that the biggest challenge for them is to get developers to build apps on top.”

The common view is that new computing platforms start with a discrete infrastructure phase, followed by an ecosystem of apps. However, the reality is that new computing platforms start with killer apps that inform the type of infrastructure that needs to be built. This then kicks off the “apps <> infrastructure cycle”.

The digital assets market has been building infrastructure for years, and this infrastructure is mostly battle tested and ready for real consumer applications to be built upon them. The most successful application of blockchain technology to-date has been U.S. dollar stablecoins. We saw early traction in 2020 and 2021 with NFTs and DeFi, but still need a lot more user growth before these are “mainstream”. In 2024, expect similar early-stage growth trajectories for AI, Gaming and DePIN (Decentralized Physical Infrastructure Networks). While this will likely boost token prices for individual projects, the entire digital asset market won’t grow until a few of these become “hits”.

Gaming - Perhaps web3 gaming has the best shot at bringing in the next 1 million+ users. Axie Infinity paved the way for blockchain-based games a couple of years ago, recording 1 million active users at its height, but design flaws and an overextension in hype saw the game fall flat. Many companies have been working to address the flaws in the first iteration of web3 gaming. As a result, we are anticipating the commercial launch of several games in 2024, with a number of them having undergone alpha and beta testing phases in 2022 and 2023. We predict that mobile gaming will be a major focus, with Asia leading the way in introducing a new wave of users. These games are likely to be listed on the Apple App and Google Play stores, and stablecoins will be used for in-game purchases. Major players in the web2 gaming industry, such as Ubisoft, EA, and Zynga, have already embraced web3 gaming and are partnering with traditional firms to bring these games to the masses. Furthermore, blockchain technology is allowing gaming communities to have a greater say in the direction and development of games, which will help create more loyal users who will become evangelists for the games.

DePIN - this is an area that can clearly benefit from blockchain and tokenization although projects are still early. The idea is to decentralize access to otherwise unavailable resources - compute, wireless, storage. Blockchains offer a way for users to access these resources, pay for them, and get rewarded for providing them. The current version of

DePIN projects show promise in design but have yet to gain real traction. However, a newer crop of projects is much more focused on creating a healthy demand side instead of just incentivizing the supply side. The increase in AI related technology is driving use cases for DePIN projects (such as the demand for compute).

AI - The intersection between

blockchain and AI is a natural fit. As anyone who traffics in data knows, “garbage in = garbage out”. While the handful of companies training today’s AI models (Microsoft, Google, Open AI) are not providing garbage, their inputs will be naturally biased. A 2016 Microsoft AI experiment on Twitter showed the

downfalls of training an AI model the wrong way. The incentive models created naturally by blockchain can help solve for this. By decentralizing and rewarding both the trainers and validators of a network, these models will organically become less biased, and ultimately lead to better models.

Prediction #6: Ethereum comes back en vogue as the generic asset to be “long blockchain”

While Bitcoin surged in 2023, and newer, faster layer 1 protocols rose even more (SOL, AVAX), Ethereum (ETH) lagged. But help is on the way. Ether is likely to outperform Bitcoin in 2024, driven by the anticipated EIP-4844 upgrade, which enhances Ethereum's network efficiency and benefits Layer 2 solutions, leading to expected fee reductions of 90%.

More importantly, after the Bitcoin ETF goes live, ETH will likely become the next asset in focus for Wall Street. While Bitcoin is a great asset to own, it does NOT give you exposure to the majority of blockchain’s growth. If you want to be long DeFi, NFTs, stablecoins, DePIN, AI, and RWAs, you need to own a lot of different types of assets, which essentially means you need to be an accredited investor and invest in a fund, or you need to quit your day job and immerse yourself 24/7 into the digital assets world.

-OR-

You can own ETH. In 2024, ETH will stop being explained as “hard money”, or as decentralized technology with hundreds of developer upgrades. Instead, it will be described as the #1 app store for all blockchain apps. And who wouldn’t want to invest in the “Apple app store of blockchain?”

If you just want to generically be “long blockchain”... you will own ETH and reap the benefits from every application that is being built on, or adjacent, to ETH.

Concluding thoughts

The best part about running multiple fund strategies at Arca is that we have the ability to invest in just about every type of innovation developed on blockchain in at least one of our fund strategies. But more importantly, the liquid nature of tokens gives us the ability to change our mind and pivot when we are wrong, or we see something that is more right.

Inevitably, many of these projections will prove to be wrong. But by challenging these theses, and looking for where we err, we will inevitably find new themes and narratives that are more interesting as investors and blockchain enthusiasts.