Source: TradingView, CNBC, Bloomberg, Messari

Markets Are Efficient

From the Random Walk Theory, suggesting that all prices are random, to “it’s all priced in”, suggesting that all information is immediately known by everyone and therefore cannot affect price, there are a lot of theories regarding what actually drives price action in stocks, bonds and now crypto. The market is efficient, or it isn’t. Who knows.

But the Bitcoin Spot-ETF may go down as one of the funniest examples of all time. On three different occasions, the Bitcoin ETF was allegedly “approved”:

- When CoinTelegraph erroneously tweeted that the Bitcoin ETF was approved in October 2023, leading to a 7% gain in BTC and then an immediate retracement

- When the SEC was “hacked” last week and announced on X/Twitter that the Bitcoin ETF had been approved one day before it was actually approved, leading once again to a knee-jerk reaction higher and an immediate retracement

- The actual Bitcoin ETF approval on Wednesday last week led to - you guessed it - another knee-jerk reaction higher and an eventual retracement

Three times, the market received the same news, and three times, the reaction to Bitcoin’s price was the same. Now if that’s not efficient, I don’t know what it is.

The Aftermath

Now that the ETF has been approved, and trading has begun for the ten product available to the market, we can move on from the binary approval process to the post-approval reactions. Some of these were predictable, others less so.

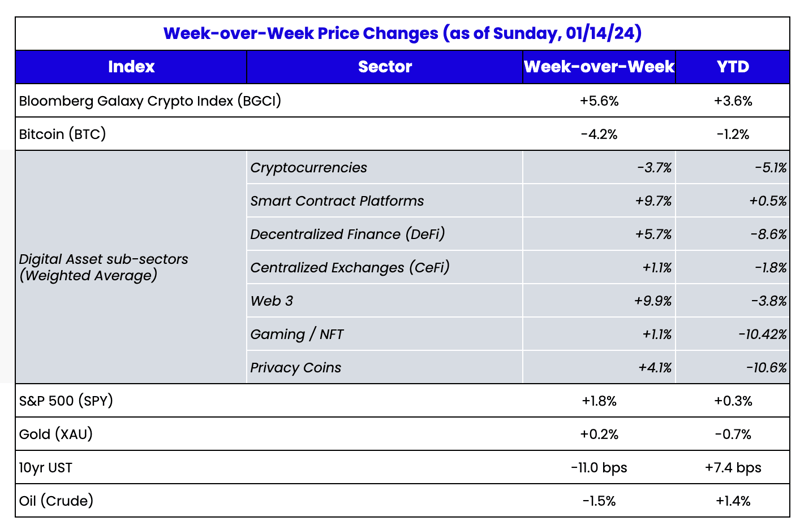

To start, BTC fell -9% last week while ETH rose +8%. While perhaps counterintuitive, this too was not an entirely surprising outcome, especially since ETH has underperformed BTC for most of the past 12 months. The ETH/BTC ratio fell from a high of 0.08 in late 2021, to a low of 0.05 recently, but jumped back up to almost 0.06 last week. We even predicted this a week ago in our

2024 predictions:

“I expect there to be a knee-jerk reaction higher upon the actual approval, largely led by algos, which will last several days, and then ultimately price will stall until the ETFs actually begin accumulating assets. ….after the Bitcoin ETF goes live, ETH will likely become the next asset in focus for Wall Street.”

Source: TradingView

Next, you can look at the flows themselves. Digital asset investment products

saw $1.18 billion in inflows last week. Trading volumes were $17.5 billion last week, the highest on record, compared to an average of US $2 billion per week in 2022.

Blackrock and Fidelity have accumulated the most AUM thus far and the highest trading volume, while Grayscale has seen net outflows as investors who have had their assets trapped for years via the GBTC trust can now get immediate liquidity and lower fees elsewhere. Again, these outcomes were fairly predictable.

Perhaps less intuitive, though a

few who called it correctly, was the reaction of “crypto stocks”, which collectively fell 15-25% last week post-ETF approval. For years, Microstrategy (MSTR) was treated as a Bitcoin proxy for public equity investors, given their

enormous holdings of BTC on the balance sheet relative to the actual earnings potential of their core business. Coinbase (COIN) and Bitcoin mining stocks have real cash flows driving their business models, and are not just a “bitcoin proxy”, but the case can still be made that they were perhaps just placeholders until BTC ETFs were launched. Some investors may be swapping out of these stocks and into the new ETFs to gain more direct exposure to Bitcoin. Longer-term, I’d expect MSTR to still trade largely in-line with BTC prices, though its premium to the BTC holdings should shrink now that there are better alternatives. Meanwhile, investing in miners will be highly leveraged bets on the price of Bitcoin, given their costs are largely fixed while the revenues are variable. But COIN is more of a wild-card given that it directly benefits from the Bitcoin ETFs since it serves as custodian for many of the ETFs, and derives a lot of its revenue from BTC trading fees, but also has a much more diversified and growing business model.

Source: TradingView

Looking ahead, the event itself is now over. The BTC ETFs are approved and are now trading. By all accounts of volume and hype, these are a

smashing success and one the record as one of the largest on record for ETF launches. A shoutout is warranted to

Eric Balchunas and

Jaymes Seyffart of Bloomberg for their excellent coverage of all things Bitcoin ETF.

How will this affect other areas of the digital assets market beyond Bitcoin? The next crop of Bitcoin investors is almost assuredly going to be from financial advisors and RIAs investing on behalf of their clients via these new ETFs, many of whom will not be on Crypto Twitter and won’t be 100% plugged into the nuances of blockchain and crypto assets. While crypto insiders think of blockchain as a technology that underpins

all sorts of asset classes, sectors, and token types, most Bitcoin ETF buyers will largely think that Bitcoin = blockchain, and their new ETF gives them exposure to the growth of blockchain. And to some extent, this is true. Bitcoin, for the most part, still has a high correlation to ETH and SOL and to the DeFi, gaming, and web3 sectors- at least for now. However, the gentrification of Bitcoin will ultimately change its behavior relative to other blockchain-based crypto assets. So when everything is going up together or going down together, no one will notice. But inevitably, there will be a time when other digital assets are going higher while BTC is flat to down. When that happens, someone who owns the BTC ETF will ask,

“Why is everyone saying that crypto is going up, but my BTC fund is not?” And that will force the advisor community and their clients to explore the rest of the digital assets market and learn about the differences between Bitcoin, smart-contract protocols, applications, and other crypto assets. When this happens, fund flows will trickle down to the rest of the market. Investors love diversification, so it won’t end with just Bitcoin.

A Win For Price, A Loss For Blockchain

Perhaps more important than the price reaction last week was the sentiment reaction. I’m incredibly happy for FAs and RIAs who can now give their clients BTC exposure via ETFs, and I’m incredibly grateful for all of the legal and financial minds who pushed this through against the will of the SEC, but let's not kid ourselves. This is a giant win for BTC price long-term, but a setback for actual blockchain applications.

Many are calling the ETF a win for real-time settlement assets, but the opposite is actually true. The BTC ETFs just jammed a real-time settlement system (blockchain) into an antiquated T+1 settlement product (the ETF). Aren’t we going the wrong way? As an industry, we should be striving towards bringing the world’s assets on-chain, not bringing on-chain assets to Wall Street’s outdated rails. There was plenty of sarcasm:

Before the ETF hype started in June 2023 (upon the Blackrock application), most blockchain enthusiasts were focused on the benefits of blockchain and being a superior technology.

But there is a tradeoff. Tokenizing real-world assets is going to take time. We’re not there yet. In order to get there, we need Wall Street to care about tokenization. Already,

Larry Fink at Blackrock has begun to discuss the potential of tokenization. Wall Street, to date, has been largely unable to profit off of blockchain’s growth and success. They write research, they trade a few crypto stocks here and there, and earn a few advisory fees on bankruptcies and IPOs, but for the most part have not been able to participate in the profits. The ETF is at least a step in the right direction in terms of focus and attention. And once they get a taste for the excitement and revenue potential, the real growth can begin.

The Bitcoin ETF was one small step for blockchain, one giant leap for BTC price.