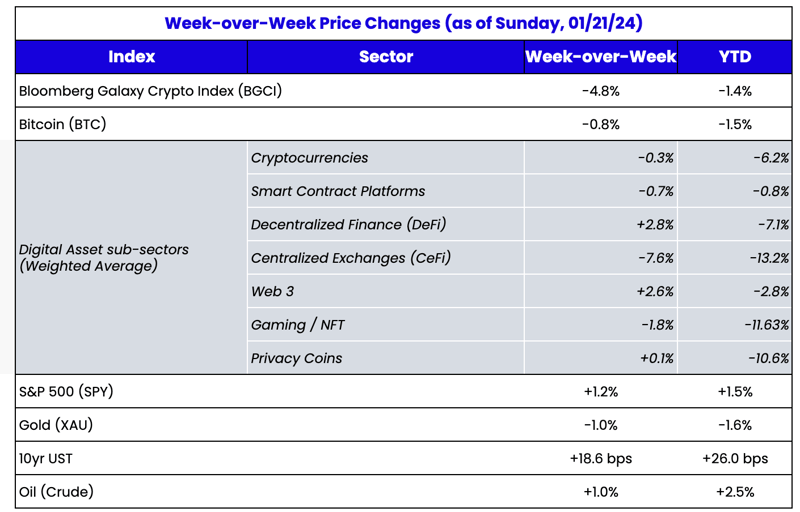

Source: TradingView, CNBC, Bloomberg, Messari

Dispersion is the Name of the Game

We typically discuss the digital assets market in terms of reference points. From 2021 to the present, we’ve seen a few large reference points:

- October 2021: Give or take, this marked the all-time high for the majority of the market.

- May 1st, 2022: Prior to the deleveraging / bankruptcy cycle beginning with Terra Luna’s demise (May 11), and the subsequent defaults from Three Arrows Capital, Celsius, BlockFi and more.

- November 1, 2022: Prior to the downfall of FTX (Nov 8) and a further cascade of defaults from DCG/Genesis and others, followed by a period of window dressing where anything owned by TradFi was sold indiscriminately into year-end (SOL, GBTC, COIN, etc).

- March 2023: The regional banking crisis began, resulting in the start of the current Bitcoin (BTC) rally, fueled further by the Blackrock ETF application in June 2023.

- December 25, 2023: What appears to have been the local top of the digital assets market after a tremendous 4Q rally.

There has been great dispersion over the past 24 months. Some tokens are now comfortably higher than pre-FTX default levels, including Bitcoin (BTC +100%), Ethereum (ETH +55%) and even Solana (SOL +177%), which fell the hardest pos- FTX but has since rallied back in an impressive way. But there are plenty of others that are still meaningfully lower than pre-FTX levels, including Binance Coin (BNB -2%), Dogecoin (DOGE -41%) and Polygon (MATIC -12%). Very few tokens are meaningfully higher than pre-LUNA collapse levels, but there are a few exceptions, including BTC (+6%), Tron (TRX +53%), Chainlink (LINK +38%), IMX (IMX +24%) and MakerDAO (MKR: +37%).

This dispersion created a ton of alpha. There have been clear thematic winners (AI, Gaming, Layer-2s), and even bigger winners within sectors (eg. SOL versus just about every other smart contract platform).

Similarly, the period since Christmas Day 2023 has once again been a token pickers’ market, with some winners even as the majority of the market has sold off from the local highs. BTC is -6% while ETH is +6% over this time period, resulting in the ETH/BTC ratio rising off of 2-year lows. But we’ve also seen many of 2023’s best tokens fall 20% or more, including SOL (-27%), Avalanche (AVAX -34%), and Thorchain (RUNE -30%). Crypto stocks, including BTC miners and Coinbase (COIN), have been equally terrible, falling 25-50% over this time period. However, a crop of newer tokens have led the gains, with Celestia (TIA +21%), Arbitrum (ARB +27%), Sui (SUI +24%) and Sei (SEI +56%) amongst some of the biggest winners.

This dispersion is important. While we all love a good FOMO rally where everything goes higher at once, the reality is that those “student body right” broad-based rallies are unhealthy. When inter-asset correlation is high, causing market makers to trip over themselves to take all prices higher at once to avoid being lifted out of hard-to-replace inventory, it leads to highly leveraged bubbles that ultimately pop. We haven’t seen any of this price action or behavior this time around. The rotation has been much healthier, and this ultimately tends to lead to more sustainable long-term rallies where the “haves” meaningfully outperform the “have nots” over time.

Everything is a Security, And That (in Theory) Should Be Fine – But It’s Not

On Wednesday, the Southern District led by Federal Judge Katherine Polk Failla heard oral arguments in Coinbase’s motion to dismiss the suit brought by the Securities & Exchange Commission. The SEC alleges that 13 tokens traded on Coinbase are unregistered securities. Coinbase argues that the trading of the specified tokens are secondary market trades in which no “investment contract” exists between issuers and investors and, thus, they cannot be securities.

While the

judge grilled the SEC, the lack of a dismissal weighed on the crypto market. The market will now wait with bated breath a few more months for a ruling.

But here’s the problem. The SEC is probably more right than wrong, but they handled everything regarding digital assets so incredibly poorly that it’s hard to root for them to win.

According to Bloomberg analysts, the SEC case seems incredibly weak, and there is a 70% chance that Coinbase will win. That’s seemingly great news for crypto die-hards who want to beat the SEC every chance they get. But it’s not actually good news. Despite the weak case, the SEC, intuitively, is probably right. Most tokens ARE securities. And that’s fine – there is nothing illegal about being a security.

Outside of crypto Twitter’s hatred of the SEC’s overreach, the industry would actually be much better off if most tokens were labeled securities because it would lead to:

- The ability for all digital assets, stocks, and bonds to trade in one place, eliminating the fragmented nature of trading of digital assets vs traditional assets, which will result in more efficient use of capital. It would also eliminate many of the crypto-native firms that rise and fall spectacularly due to smaller balance sheets and poor risk management.

- Mandatory and accurate reporting and greater transparency from projects that are centralized and should be treated no differently than corporations.

- Profit-sharing from projects to token holders, instead of many founders pretending they can't distribute profits while hiding behind lawyers who tell them they can’t due to the SEC.

- A re-emergence of ICOs and direct sales of tokens, eliminating the unnecessary stranglehold that venture capital firms have over token projects. There's a reason PIPEs aren't popular in the equity world (because they are unnecessary in most cases). Yet, in crypto, this has become the norm where token issuers continue to issue unnecessary discounted private deals to VCs while they have perfectly good publicly traded liquid tokens.

- More token issuances from reputable businesses and entities that would benefit from having a token, like municipalities, universities, small and medium-sized companies looking to attract and align customers with their growth, and public companies like Delta, United, Netflix, Disney, Starbucks, and others with subscription services and/or loyalty programs.

Securities law works pretty well for investors and issuers. And while the SEC has done nothing to earn the right to govern crypto nor prove that they should have jurisdiction, let's not lose sight of the fact that what we have now isn't better either.

“I don’t give a damn what is a security, and what isn’t. I trade securities all the time. There’s nothing illegal about being a security as long as securities laws are followed. Please feel free to call all tokens securities if you want. It won’t bother me in the least, it doesn’t change the long-term value proposition, and I welcome a registered exchange and rock-solid, “tried and true” U.S. securities regulations to help shepherd in the next wave of blockchain adoption…

… BUT…

… if you (the SEC) are hellbent on calling every digital asset a security and regulating the whole industry, then for the love of god, find a way to make it cheaper and easier for exchanges to get licenses in order to trade them, and for token issuers to be able to issue them, and for truly decentralized projects to be able to comply. The everyday people in this industry do not need to continue to suffer simply because Congress hasn’t issued new laws yet, and the SEC is unwilling to adapt its 80-year old laws to new technology.

Seven months later, nothing has changed, and all of the above is still true. The government and the regulator of choice need to understand the nuances between a centralized entity issuing tokens that has defined employees that can handle regulatory filings versus the handful of truly decentralized projects that would have no way to comply with current regulations. As Galaxy Digital wrote to their clients this weekend:

“We believe that cryptocurrencies are fundamentally novel and, while some may be securities, they fundamentally do not fit within current US securities regulatory frameworks. There are effectively two paths regulators can take to bring clarity to digital assets on this topic:

1) create a new, bespoke regime starting from first principles (which is the approach the EU has taken with its Markets in Crypto Assets (MiCA) regulation), or

2) fit digital assets into existing regulatory frameworks (the approach the United Kingdom has been taking).

The first approach is certainly valid if done deliberately in a way that balances capital formation and promoting innovation with consumer protection and orderly markets. The latter can also be effective, but requires the production of significant interpretive guidance so existing regulated entities understand how to apply old rules to new technologies, asset classes, or processes. The SEC has taken the latter approach but has neglected to produce substantive guidance on how entities like broker/dealers, exchanges, transfer agents, or others could actually custody, list, trade, or use digital assets.”

Lost in the war between the SEC and crypto is that the current environment is just as bad as the one proposed by the SEC. Rooting for the SEC to lose doesn’t solve anything, but the SEC winning doesn’t either. Rooting for common sense is the only way we move forward, but unfortunately, those in the common sense corner don’t wield any power.