What happened this week in the Digital Assets market

What happened this week in the Digital Assets market

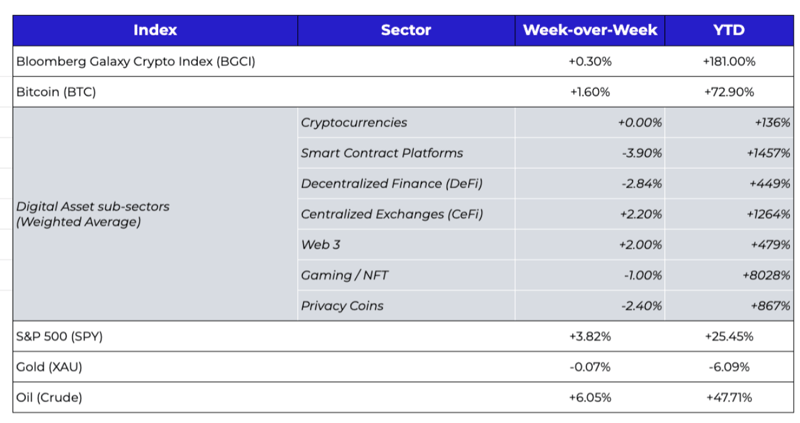

Week-over-Week Price Changes (as of Sunday, 12/12/21)

Source: TradingView, CNBC, Bloomberg, Messari

When the easy macro trade fails

Roughly 18 months ago, Paul Tudor Jones unveiled his inflation thesis, which included but was not limited to a thesis that Bitcoin would likely be the fastest horse. What many forget is that Bitcoin was just one of many ways in which PTJ was expressing this view. The point of his investment memo was not Bitcoin; instead, he was identifying the best inflation trades, of which Bitcoin was one of many items on the list. The others included:

- Gold - A 2,500 year store of value

- The Yield Curve - Historically a great defense against stagflation or a central bank intent on inflating (long 2-year notes, short 30-year bonds)

- Nasdaq 100 - The events of the last decade have shown that QE can rapidly leak into equity markets

- Bitcoin -- for many reasons which he went on to describe

Let’s check-in all of these trades since May 1, 2020:

- Gold: a palty +5%

- 2s/30s steepener: Only 5 bps steeper (basically unchanged), though it did steepen quite a bit up until recently when the curve flattened dramatically

- Nasdaq 100: +86%

- Bitcoin: +467%

This basket approach certainly performed well, though Bitcoin and the Nasdaq 100 have driven all of the returns. The outcome would have been far worse had he only expressed this view via Gold, or the 2s/30s steepener. Ideas are a dime-a-dozen… how you express those views is what matters.

Now let’s fast-forward to today. Inflation and Omicron have been the main topics on the minds of every investor, driving high levels of volatility and downward price action for most of the last four weeks. Every investor is trying to find the best way to express these macro events. Investors were glued to their screens during the last 2 monthly CPI prints, certain that higher inflation is now bad and lower inflation is good. Last week’s CPI report was ugly, as expected, yet the market reaction was strange.

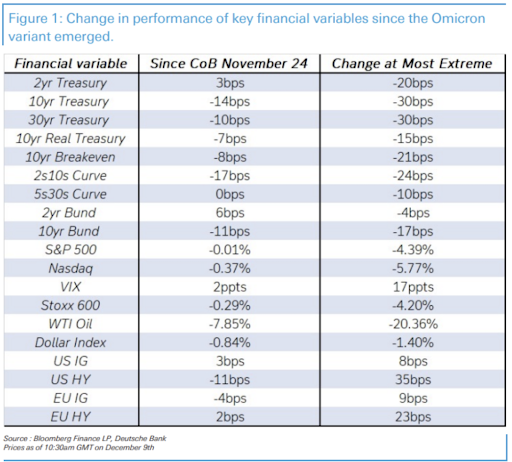

On the heels of two sharp weekly declines, the S&P 500 rose +3.8% last week to close at yet another record high, and other US indices rose 3-5%. It was the strongest weekly performance for the S&P 500 in 10 months, sending the VIX tumbling back down 39% to 18.7. In fact, just about every risk asset has fully re-traced the November/December macro slide driven by Omicron and inflation… almost as if none of the last month’s turmoil even happened.

Source: Deutsche Bank

But digital assets have not bounced back at all. Over the past 30 days, Bitcoin has fallen 25%, Ethereum has fallen 15%, and most digital assets outside of a few outliers (e.g. AVAX flat, MATIC +15%, LUNA +20%, SAND +120%) are now down -30-50% from their November peaks. Last week, even as equities bounced hard, digital assets continued to struggle. So if it’s all one “macro trade”, how you expressed that view clearly mattered a lot these past few weeks.

Now, we’ve argued numerous times that the correlations between digital assets and all other risk assets including equities are far too inconsistent to draw any long-term conclusions, and yet, we’re also very quick to point out whenever these relationships change. And this past month has been a doozy when it comes to changing relationships. Last week we pointed out that broad equity indices are masking the real carnage in the equity market, as the broad market is dominated by a handful of large caps, which are moving higher and subsequently hiding a much more bearish picture under the hood. Perhaps the continued struggles of tech ETFs like ARKK, SPAK, and meme stocks like AMC, are far more indicative of the risk tolerance digital asset investors are willing to take heading into a more murky macro regime. Over the past few weeks, all of the sector dispersion within digital assets that we’ve experienced year-to-date has been completely thrown out the window, with most digital assets now being lumped together as one giant trade. Instead of dispersion of “haves” and “have nots” like we’re seeing in equities, the entire digital assets market is being treated as a “have not”.

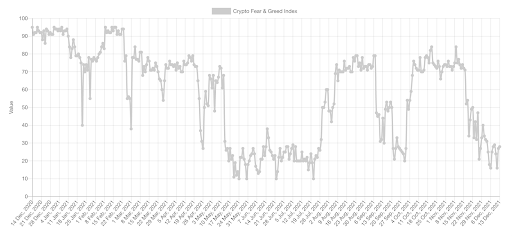

Perhaps those selling digital assets are just flat-out wrong again, like they were in July and September 2021, the last two times negative sentiment reached this low of a level. Back in the summer of 2021, it was quite easy to debunk all of the ridiculous bear-market narratives that were dominating price action. Today, it’s more challenging, largely because there really isn’t a solid broad-based bear-market thesis to break down. It’s been our thesis for years that there will be no broad-based market crashes or broad-based market rallies anymore, as investors are now able to distinguish between different types of digital assets, some of which will perform better than others in different environments. Many now agree with us. But these past two weeks have tested that thesis. Most investors seem to be taking profits after a banner year (or to pay taxes), or are just flat out scared, without being able to articulate what it is they are actually scared of. So the question becomes “where do these sellers put their money when they stop being scared or need to re-invest their proceeds?”

We rely on a lot of indicators to help us understand where the market is headed, and either our indicators no longer work (and they’ve worked great over the past two years), or this is once again a great buying opportunity of certain beaten-down digital assets. Of 26 indicators that we monitor daily, 11 are bullish, 14 are neutral, and only 1 is bearish. The lone bearish indicator is “inter-asset correlation”. The fact that all digital assets are moving down together recently is a strong negative signal, though if this persists, it would also erase two years of increased market breadth. This is probably the most important factor to monitor over the next few weeks. Was the maturation, evolution and sophistication of digital asset investors simply a mirage, and we’re about to head back towards a 2018-like highly-correlated march lower… or is this simply a buyer’s strike into year-end?

It’s worth noting, we’ve seen this pattern over the past four years -- where the first 2 weeks of December are very choppy, only to resolve incredibly bullish over the back-half of the month and into the new year. Since this is the last “That’s our Two Satoshis” of 2021… we’ll have to check back in the new year to see if the pattern holds for a 5th straight year.

Year-end rallies (using ETH as a proxy) for the past 4 years

Source: TradingView/Arca

Can anyone actually protect DeFi users?

We’re big believers that DeFi usage is going to continue to grow quickly, and that the risks will subside as user education increases and UI/UX improves. But another area of focus is insurance. The biggest risk in DeFi is loss of principal, a risk that can be fully neutralized in many cases via insurance coverage. Nexus Mutual is the largest insurer to date, with over $700 million of active cover currently. However, Nexus came under fire earlier this month after BadgerDAO announced they had suffered an unauthorized withdrawal of user funds, but Nexus announced that this hack is likely not covered by insurance.

As Coinbase wrote:

“Further investigations found that the attackers acquired Cloudflare account access for the badger.finance website and periodically injected malicious code into the website front end to collect token approvals from victims interacting with the website. After almost two weeks of collecting token approvals, they transferred approved tokens in a single batch out of the victim’s wallets on December 2nd and then proceeded to swap these tokens using RenVM to move the funds on the bitcoin blockchain. Normally any BadgerDAO user could have insured its funds using Nexus Mutual, which offers insurance on Badger finance for 2.6% annually. However, according to Nexus Mutual’s terms and conditions, the insurance only covers “contract bugs, economic attacks, including oracle failures [and] governance attacks.” Hence, if the attack is confirmed to be a front end attack, BadgerDAO’s contract may not have been triggered and the event will not be covered by the insurer.”

This seems pretty straight forward from Nexus’ standpoint -- as the policy clearly states what is covered and what is not. However, this also reveals a broader problem, which is how does a user fully cover all of the risky scenarios present within DeFi, when many are in fact just user error. Home insurance doesn’t cover a 5-year old playing with matches, and auto insurance doesn’t cover loss of car keys. Unfortunately, some DeFi users have the equivalent level of technical expertise. As has been the case throughout the young history of digital assets, we’re likely headed towards a solution here, with a broader array of coverage options on their way. However, the DeFi platforms themselves need to step up and start demanding/encouraging that their users insure themselves, in the same way that a rental car agency asks you to buy insurance before you rent the car. The onus should not be on the user.

TradFi and Governments are severely underestimating how much everyone hates them

Former Lyft CFO, Brian Roberts, will be transitioning out of his seven-year tenure at Lyft and joining OpenSea, the world’s largest NFT marketplace. OpenSea is dominating NFT sales, with over $10 billion in life-time sales, and almost 1mm users to date. Given the success of the company, Roberts said in an interview that he was considering an IPO. It didn’t take long for the OpenSea community to unleash their backlash, leading to Roberts and OpenSea backtracking from their statement.

This trend of community pushback is going to increase precipitously in 2022 and beyond. The days of VCs funding a project, passionate users turning that project into something valuable, and then sitting idle as VCs and founders walk away with all of the money are over. We wrote about this misalignment between companies and their customers over a year ago following the DoorDash and AirBNB IPOs. Those passionate users who make companies great are not going to be pushed around for much longer.

As Galaxy Digital wrote in their weekly note:

“the fierce backlash of OpenSea users to Roberts’ comments about a possible IPO also highlights the cultural differences and inevitable clashes between the ethos of the crypto industry and big tech. Crypto-native users and developers hold fast to values of decentralization, democratization and data privacy, while the values of big tech have arguably been more focused on centralization, walled gardens and data surveillance. Some Coinbase users raised similar complaints when the company listed on public markets, suggesting it should have offered some form of tokenized equity as well. Rather than emulating the practices and strategies of big tech, OpenSea users have long anticipated the release of a native marketplace token similar in design to the governance tokens of decentralized finance projects such as MakerDAO, Uniswap, and Sushiswap.”

Said another way, traditional finance/banks/governments have severely underestimated how much people hate them, and how that alone can power the growth of an entirely new system within digital assets. We now live in a world where anons and influencers with zero experience are given the benefit of the doubt over someone with credible experience who happened to have gained that experience on Wall Street, in Big Tech or in Government. For example, I personally get ridiculed just about every day on Twitter just for having "Lehman" and "CFA" on my twitter bio... as if that alone somehow discredits me despite dedicating my life and career to digital assets over 5 years ago. In some ways, it probably does.

One of the coolest, grassroots efforts of the year came recently with the rise of ConstitutionDAO, breaking records with over $45 million raised from 17,437 unique Ethereum addresses, with the goal of purchasing a rare copy of the Constitution. And in a move so tone deaf that he must have been drinking a Pepsi while doing it, Ken Griffin of Citadel outbid this group to purchase it for his son. One TradFi billionaire decided to alienate 17k individuals, most of whom are already looking to take down Wall Street every chance they get.

The new world simply does not care about old finance and government. It’s worth really absorbing some of these recent comments on the new state of finance:

The top 10% wealthiest Americans own 90% of all US stocks. Did you really think in the age of instant coordination and communication that younger investors were going to try to compete in a rigged game? Good luck to those in 2022 still trying to stop this trend… because it’s only growing stronger.

What’s Driving Token Prices?

- MATIC (-9%) - Polygon’s monetization has seen record growth, setting new ATHs in network revenue for four weeks running. In MATIC terms, revenues jumped 24% week-over-week. In USD terms, revenues increased 44% to $136k per day, as average cost per transaction last week was $0.035. Average transaction prices have grown 53% month-over-month. Polygon’s CEO also announced he would stake all his tokens, which was received well by the community as it has positive implications for Polygon's native token

- HNT (-7%) - Helium announced a new partnership with Techtenna which "guarantees connection and simplifies end-to-end IoT solutions for companies like Honeywell and Brabant Water" and plans to deploy over 2 million sensors on Helium's IoT network by 2023.

- YGG (-8%) - announced two new game partnerships with Fancy Games DAO and Alethea. YGGSEA, YGG's first subDAO focused on South-East Asia, also announced its launch and funding round.

What We’re Reading This Week