There has been a lot of speculation about what role Bitcoin will play in the future of money. These views range from digital gold to an unalterable store of value to nothing at all. While all of these views are interesting and worthy of examination, the one I want to discuss here is the idea that Bitcoin will become the global reserve currency. Many have suggested this possibility, and Anthony Pompliano expresses this idea succinctly and in a representative manner below:

But what does this mean? We need to examine the role and history of reserve currencies before we can talk about the ramifications of Bitcoin ascending to this status. A reserve currency is:

A currency that is held in significant quantities by governments and institutions as part of their foreign exchange reserves. The reserve currency is commonly used in international transactions, international investments and all aspects of the global economy. It is often considered a hard currency or safe-haven currency. People who live in a country that issues a reserve currency can purchase imports and borrow across borders more cheaply than people in other nations because they do not need to exchange their currency to do so.

This definition obviously envisions a world with sovereigns issuing currency and trade and accounting requiring a common currency to make it efficient. But what does this mean in the world of digital currencies? Will governments hold a reserve of Bitcoin in support of national currencies? Will national currencies survive? These questions and others are what the creation of digital currencies have spurred.

Let’s take a brief look at reserve currencies and the role they played throughout history. The World Bank published an interesting report in 2011, called Multipolarity: The New Global Economy. I highly recommend it if you have a couple of hours to kill. The lion’s share of the report discusses trade balances, multilateral trade agreements, and the shifting nature of the increasingly global economy. The third section is about the role currency plays and how it will evolve in an increasingly multipolar world.

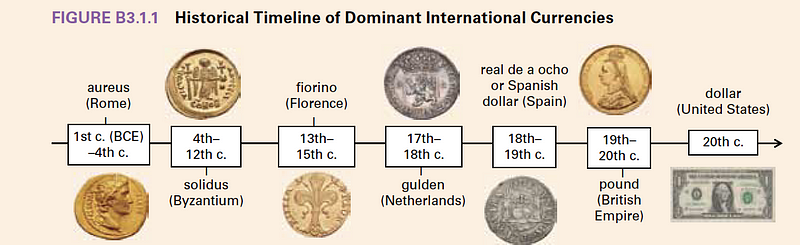

The report includes a historical overview of reserve currencies

Prior to the British pound, reserve currencies were minted in precious metals from the dominant trading power of the time. The rise of Great Britain as a mercantile power and the advent of gold-backed and interest-bearing notes was the first time that a reserve currency became one factor removed from the underlying store of value. This link became even more ephemeral when the US Dollar emerged as the dominant currency in the 1920s and the abandonment of the fixed exchange Bretton Woods system in the 1970s. The report envisions the rise of an international reserve currency, the Euro, with the rise of a multi-polar globalized world. But something has happened on the road to the fair.

2011 was in the immediate wake of the financial crisis. Since then, debt-fueled spending, tenuous political unions like the EU, and an increasingly polarized world have made the future unclear. It is no longer evident that the EU (Think Brexit, Five Star in Italy, PIIGS crisis and Yellow Vest Protests) will survive and the US dollar is being challenged by the Chinese Yuan. All the major central banks are in the midst of unprecedented monetary stimulus and seem to be trapped, it is a moment where there is no clear path forward.

This opens the door for Bitcoin, or some other independent candidate to step in. Original reserve currencies were in specie made from a precious metal. Was the attachment to these metals something special or the fact that they were scarce and unable to be replicated? The other quality of reserve currencies is that they are used in international transactions. The US dollar is king and the petrodollar is real but is its use in international trade enough to overcome infinite production? This remains to be seen.

The other aspects of a digital currency like Bitcoin becoming a reserve currency also highlight aspects of the financial system that a digital currency’s attributes bring into question. Reserve currencies are held by the non-dominant country in order to strengthen their own sovereign currencies. In a world where Bitcoin is ascendant, is there a need to hold it in reserve? Would we not all just transact in Bitcoin? What would be the benefit of trading into a sovereign currency that was suspect? Would we need sovereign currencies at all? Again, the fundamental nature of these new technologies is challenging our understanding of what currencies are and the role of the state.

What is highlighted again and again, is that all of these long-term trends are really narratives. What will drive the adoption of Bitcoin as a “reserve currency” will be how these narratives play out. All current signs point to the fact that change is in the air, and for the first time, this role really might be filled by a currency outside the control of a sovereign power. And if I may paraphrase Pomp, “There is a non-zero chance that a non-sovereign digital currency will fill the role of what we used to call a reserve currency.” At the moment, the leading candidate is Bitcoin.

.png)