[Block] Chain of Events

Before diving into the weekly recap of the markets, we are pleased to announce a new monthly series “ [Block] Chain of Events “, written by Arca’s Research team led by Katie Talati and Hassan Bassiri. [Block] Chain of Events is a well-informed write-up covering thematic events affecting crypto prices. Because of Arca Digital Asset Fund’s event-driven investment strategy, the Arca Portfolio team is constantly monitoring, utilizing, and evolving this strategy based on new events and information. While “Two Satoshis” is written for all types of crypto investors, the “[Block] Chain of Events” is written for those looking to employ actual crypto investing strategies.

What happened this week in the Crypto markets?

Investing is getting really difficult, irrespective of asset class

Last week, oil finally rebounded after 4 straight weeks of massive losses, but high yield credit remains under fire, US & International equities gave back all of the prior week’s gains and then some, and the VIX is on the rise (+25% last week) meaning it is becoming very expensive to hedge. Meanwhile, the 2s/5s yield curve inverted, signaling recession. And crypto… well, as we stated a few weeks ago, crypto is at the top of the “risk off” trade list and continues to plummet, as sentiment has gone from euphoric to bearish to panic in just four weeks.

Bitcoin fell 13% week over week, adding to losses the last three weeks of 8%, 22%, and 13% respectively (compare that to oil which fell 5%, 11% and 7% over those same three weeks). The rest of the crypto market fell in lockstep, as correlations remain above 90% between BTC and other digital assets. It’s worth noting that crypto correlations to traditional asset classes remain very low, however, they are starting to rise, which typically only happens in declining markets when all risky assets get lumped together.

What’s next for crypto — is there a less bifurcated outcome?

It is common to see a broad spectrum of opinions in crypto, but they are becoming louder and more extreme as the severity of the price declines accelerate. There are some people out there who legitimately believe every single crypto asset (including BTC) will be dead soon because a group of organized pioneers of crypto is intentionally tanking the market, ready to replace it with a new Distributed Ledger Technology (DLT) that will be even better than current assets (we do love conspiracy theories). And there are plenty of others who adamantly believe BTC will be at $250,000 in a few years as its momentum amongst consumers and large Wall Street players can’t be stopped. In fact, this is 4th major 80% drawdown since 2011, and each subsequent Rise of the Phoenix has made prior crashes largely irrelevant in retrospect.

But the scariest and potentially damaging narrative around digital assets doesn’t make for great headlines, and thus won’t dominate the news like the extreme bull and bear calls. And that is — “Digital assets are interesting, they work, and some people do value them. But they just don’t provide ENOUGH value to ENOUGH people to grow beyond a small niche.” Meaning, some great technologies just never truly catch on in a big and meaningful way. In that scenario, Bitcoin and its derivatives won’t completely crash, and digital assets won’t be classified as a “tulip-like bubble.” Instead, digital assets may just languish as a second or third tier technology. The fact that there is an alternative outcome beyond the boom or bust scenario is largely ignored.

This is obviously a tough call to make (we try not to make outlandish calls at Arca — instead we try to present facts and offer opinions). In 25 years, there may be a great video like this entertaining interaction between Bill Gates and David Letterman discussing the usefulness of the internet. Will we look back in 25 years and cringe at our own naiveness? Perhaps.

The entire market cap of publicly listed digital assets is now just $114 bn (down from $800 bn earlier this year). If you add on the non-publicly listed tokens and equity in blockchain companies, that would push the entire market size to $125-$150 bn. Can anyone definitively say that there is less than $125 bn of value in this entire ecosystem? By comparison, there are almost 75 public and private companies alone that have individual market caps over $125 bn. Phillip Morris and General Electric, for example, have market caps just above $125 bn, and they are both in secularly declining businesses. So while it remains challenging to value each individual token and equity of blockchain companies that will eventually create enormous value, it’s equally difficult to argue that value won’t accrue to multiple assets in this space. The size of the pie is growing even as each piece of the pie shrinks. Where and how to capture this value increase is the million dollar (or 294 Bitcoin) question.

Total Market Cap of Crypto is Now Less than $125 billion

The “Max Pain Theory”

We remain very bullish long-term, which should seem obvious given everyone on the Arca team has dedicated their careers to this technology. But in the short term, of course, anything can happen. Given sentiment has shifted so starkly from “institutional investors are coming and everything is going higher” to “it’s all going to $0,” we’re starting to dust off the old “max pain theory” books from past financial crises. Said another way, the market usually moves in whatever direction “causes the maximum amount of pain for the most people.” For example, at the tail-end of 2011, almost every hedge fund was short and expected the worst outcomes from the European banking crisis, so of course, coordinated Global Central Bank Actions sent the market screaming higher, erasing the YTD gains of many hedge funds. Most recently in US Equities, FANG stocks were the market darlings and almost universally owned before a 25% correction took out gains from the majority of funds.

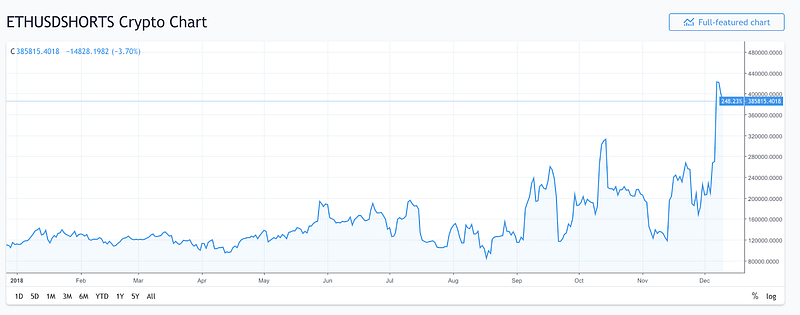

In crypto, just about everyone who can short is, with short positions rising across most liquid tokens, often using leverage. Others who can’t or don’t short seem vastly underweight. When you’re rewarded for continuing to push the market lower with no resistance as you have been for the past four weeks, there is no reason to stop until this strategy stops working. But the size of this market is now so small, theoretically, a single player could take out all of the shorts and push this market much higher, very quickly, on low volumes. The “Max Pain” Theory would suggest a bullish reversal soon.

Shorts are rising as price collapses for large liquid tokens like Ethereum (ETH)

The Bitcoin death spiral

While we don’t normally get in the technical weeds in our Two Satoshis write-up, this one is important for anyone looking into this space as a potential investment. There was a lot of talk last week about the Bitcoin “death spiral,” or what many believe is the unwinding of the fragile balance in Bitcoin between mining, block rewards and difficulty. The Block tackles this well, providing a basic breakdown of this idea and why it is overblown.

For those new to Proof-of-Work mining, BTC’s mining difficulty just saw its second largest drop in history, with a -15% adjustment on Monday, Dec. 3. The Bitcoin network’s Proof-of-Work difficulty “retargets” after every 2016 blocks, or over 2 weeks assuming each block takes 10 minutes to mine. The largest drop in the difficulty of Bitcoin mining in history happened on Oct. 31, 2011, with an adjustment of -18%, while another decrease (-13%) in mid-October 2011 is the third largest such decrease.

One of the most brilliant aspects of Satoshi’s original vision for Bitcoin is the notion of self-correcting mining rewards, keeping the Bitcoin ecosystem in check in a clever, variable way. Imagine a firm that lost half its employees, and immediately the firm self-corrects to the point where the work gets re-distributed to become easier for the remaining workers so they don’t get frustrated and leave the firm too, yet production doesn’t wane at all. Then others realize how easy these remaining workers have it, and immediately apply for jobs, making everyone’s jobs harder again but with less work to do, and again, production stays constant. That’s essentially how Bitcoin’s difficulty algorithm works, ensuring production never stops and the work (or hash rate) is proportional to the number of players involved.

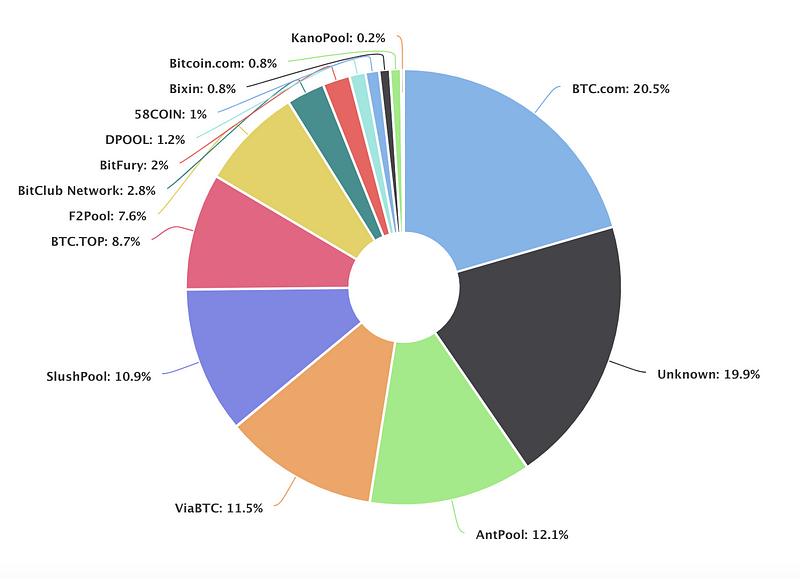

While we don’t agree with the “death spiral narrative,” it is true that people in this digital asset ecosystem will have to forfeit decentralization for security. But the reality is Bitcoin has always been centralized … as major mining pools dominate. That aspect of decentralization was never really solved in the first place, and the only part of the pie that shuts down when difficulty and costs rise is the 19% listed as “Unknown,” while other major mining shops keep going.

An estimate of hash rate distribution amongst the largest mining pools

Furthermore, the gap between the difficulty rate and the hash rate was always supposed to widen… that’s not new or unexpected. So if the question is “did it widen so far that it is no longer recoverable?,” we would say unequivocally “no.” The mining difficulty is based on block production, not time. If the previous 2016 blocks took more than two weeks to find, the difficulty is reduced (meaning it takes less computing/hash power to mine the next blocks) and if the blocks took less than two weeks, the difficulty is increased.

It’s true that given the increase in difficulty, some miners may choose to shut off their equipment. But based on a recently published research report by Coinshares, there’s a difference between (i) mining at an overall loss (Mining Profits < Fixed capital (equipment) + Operating Expenses (electricity, rent, etc.)) and (ii) mining at a cash-cost break even (Mining Profits > Operating Expenses). Miners shut down when they can’t cover their cash cost, but as long as the BTC price stays above their cash cost break even (~$3400 for miners in China) then they will remain on even at a negative ROI because any profits above their cash cost can be used to recover a portion of their capital equipment.

So did we just hit a fulcrum where each incremental day in the red for miners, caused by a longer period of time between adjustments leads to more miners pulling out and longer periods of red?

Again, we think no. Let’s say during the 17.5 day period required to mine the next 2016 blocks, some miners shut off their equipment resulting in a decrease in hash rate. That just means the miners who continue on when the difficulty level adjusts downward will contribute a greater overall portion of the hash rate and be entitled to more block rewards for the next 2016 blocks. Miners that endure a bear market are at a massive competitive advantage, and as it gets easier to mine, more come back in. It’s a remarkable piece of natural selection engineering and an example of the type of incentive systems that this technology makes possible.

Notable Movers and Shakers

Security selection may matter once again, as alts are outperforming other large-cap tokens.

What We’re Reading this Week

That’s the battle cry from most crypto bulls, many claiming that institutional custody options are necessary for the cryptomarket to take its next step. However, State Street has stated they will not be entering the arena just yet: “There is a very high level of interest but no need to move because currently none of our clients are looking for us to house these assets in custody.” Despite this, crypto custody still has a bright future with two qualified custodians (Bitgo and Coinbase) and involvement from traditional custodians Nomura, Northern Trust and Fidelity.

Calastone, a fintech back and middle-office provider to Wall Street financial services companies, said it plans to move its entire system onto the blockchain. Although the article makes no mention of it, presumably the move would be towards a private blockchain. The firm claims such a move would save them $217 billion. Blockchain has many applications to simplify and streamline outdated back office systems. It looks like we’re finally beginning to see these emerge.

A pre-solicitation document from the Department of Homeland Security was released this week discussing the ways in which cryptocurrencies can be transacted. They note that privacy tokens, such as Zcash and Monero, are particularly of interest to them as they have transaction masking features. What many probably don’t realize is that the document is a request for outside information and assistance with understanding crypto technology so that DHS might better evaluate forensic evidence from blockchains

ETCDEV, the largest development group supporting the Ethereum Classic chain, announced last week that they were out of funds and shuttering operations. This comes as no surprise to those that have followed the market over the last year. Over the summer while most of the market was down, ETC made considerable gains after listings on Robinhood and Coinbase, pushing token price above $16. The correction was swift and compounded during last month’s market correction. As of the time of writing, ETC is trading at $3.87. Although there are still a handful of development groups continuing work on ETC, ETCDev was the largest group providing the most support to the blockchain.

Despite the last month of painful losses in the token market, ErisX closed on $27.5m in new funding from Nasdaq Ventures and Fidelity. ErisX is building a regulated crypto exchange that will offer spot and futures trading for BTC, LTC, and ETC. This is a positive step for crypto as the need for quality trading tools and systems is abundantly clear. We eagerly await ErisX’s launch to see if they live up to the hype.

This article explores the similarities between the beginnings of the crypto markets and the traditional financial markets as we know them today. Specifically, it compares crypto to the development of the traditional stock markets, the high yield bond markets and finally the internet boom of the early 2000s. Although we don’t necessarily agree that we’re seeing institutional adoption in crypto now, we appreciate the comparison of crypto to other high risk, high reward asset classes.

Last week an episode of Jeopardy aired with where contestants were challenged with five different crypto questions.

Answer: A technology and an asset class that is not going away even though prices are tanking

Question: What are Digital Assets?

We’re constantly inundated in crypto with grand ideas regarding technology, transparency, and decentralization. But sometimes we need to step back and remember what good digital finance can actually serve the world. Bill Gates shared his thoughts last week on digital assets as a breakthrough innovation that has the potential to affect those living in poverty worldwide. Our team tends to agree:

Arca in the Press & on the Streets

- MarketScale sat down with Arca CEO, Rayne Steinberg, to discuss cryptocurrency and blockchain on a philosophical level in this podcast. Steinberg discusses why some investors aren’t keen on the risk of Digital Assets because it is difficult to understand what to make of an anarchic, trustless system

And That’s Our Two Satoshis!

Thanks for reading everyone! Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA — Portfolio Manager

Katie Talati — Director of Research

Hassan Bassiri , CFA — Junior PM / Analyst

To learn more or talk to us about investing in digital assets and cryptocurrency

.jpg)

Source: Coinmarketcap.com

Source: Coinmarketcap.com Source: TradingView

Source: TradingView