Source: TradingView, CNBC, Bloomberg, Messari

The Ethereum Shanghai Rally

If all you’ve done thus far in 2023 is fade consensus, you’re doing pretty well as a digital assets investor.

- The consensus view heading into 2023 was that digital asset investing was dead amidst a regulatory crackdown and a string of high-profile bankruptcies.

- The consensus view from a macro perspective was higher rates for longer, a drop in stocks, and an imminent recession.

- The consensus heading into early March was that a banking crisis would be bearish for risk assets, including digital assets.

- The consensus view within digital assets was that Bitcoin was dead and would continue to underperform ETH and other assets.

- And the consensus heading into the Ethereum Shanghai fork this past week was that ETH would fall precipitously once early stakers could unlock and sell

The contrarian trade has worked all year. While some of the contrarian success has been due to the unwind of crowded trades, most of it was due to consensus just being flat out wrong, especially regarding interpretation of investor behavior around key events.

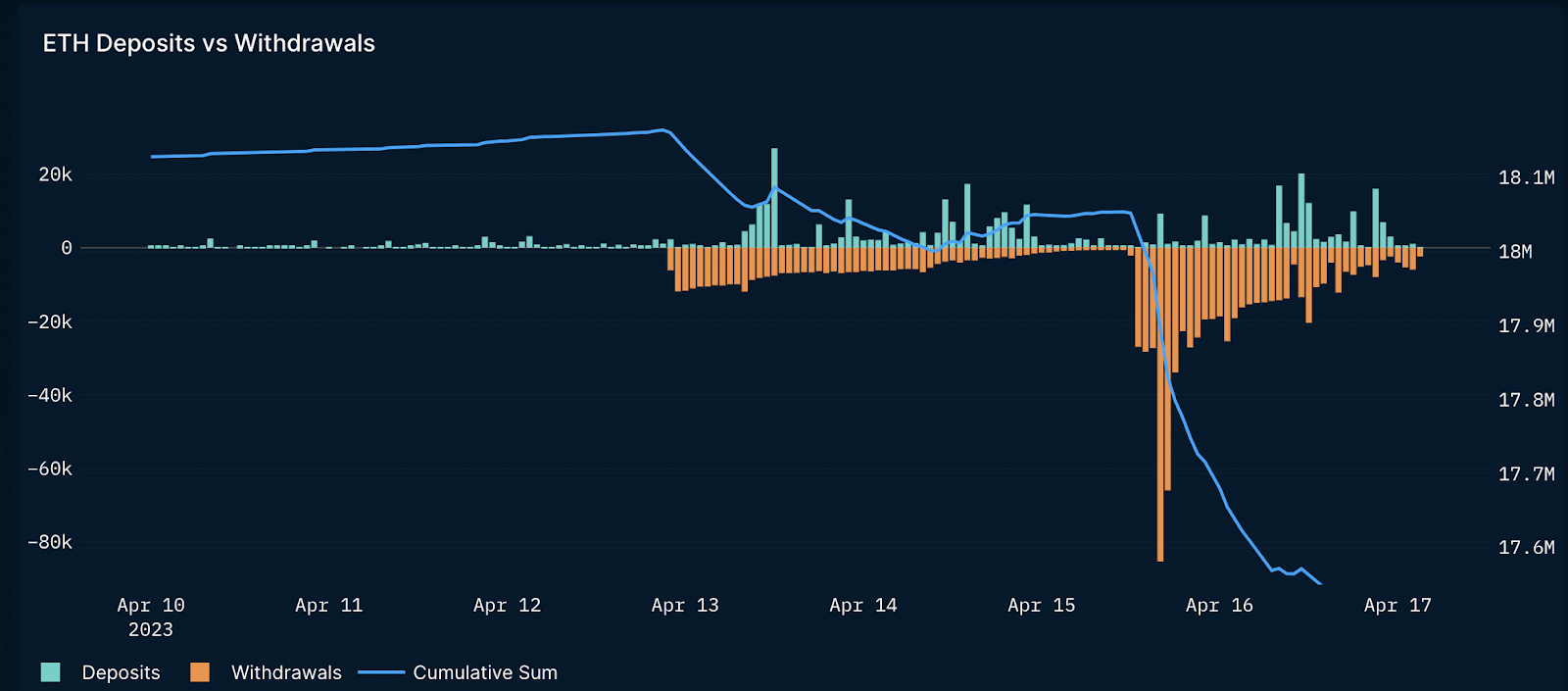

This past week, the Ethereum blockchain successfully completed its 15th hard fork—Shanghai—which primarily activated staked ETH withdrawals and marked the completion of Ethereum’s transition to a proof-of-stake (PoS) consensus protocol. For some reason, there were numerous claims that 1 million ETH (~$2B) would be sold instantly and it would be bearish for ETH. This analysis never made sense for a variety of reasons. First, it is impossible because Lido (which controls 30% of staking rewards) isn't unstaking until next month. Second, it assumed that individual home stakers who locked up ETH in late-2020 for an unknown amount of time would suddenly dump all of their ETH (and forgo future yield) at a loss and convert into fiat or stablecoins (which became even more unlikely post the March banking crisis of confidence). Further, these claims didn’t recognize that stakers cannot withdraw ETH instantly; staked ETH takes 4-5 days to access.

Expectations of large outflows did not materialize. As Galaxy Digital wrote in their weekly note to clients:

“Deeper analysis of withdrawal activity on Ethereum since Shanghai indicates that the vast majority of withdrawals processed are partial, representing Beacon Chain issuance rewards, not full, which would conversely represent validators exiting the network and unstaking their principal balance of 32 ETH. Of the full withdrawals process on Ethereum in the first 24 hours after Shanghai, 97% of them have been initiated by cryptocurrency exchange Kraken, which earlier this year was forced to shut down their staking-as-a-service product due to enforcement actions by the SEC. Therefore, contrary to some Ethereum critics’ expectations, it is clear that Ethereum validators have not been ardently waiting for the activation of Shanghai to dump their ETH. Rather, the vast majority of Ethereum validators are continuing to stake, and the ones that are not are predominantly validators operated by a crypto exchange retiring their staking operations.”

More importantly, even if the ETH withdrawal and sales prognostications were remotely accurate, it still failed to account for how much new demand for staking services would be generated upon the release of more favorable liquidity terms. Due to the illiquidity, only 15% of ETH was staked before Shanghai. Most other proof-of-stake blockchains have north of 50% staking rates. So even if all 15% of ETH holders unstaked, it’s still a drop in the bucket relative to expected new demand. Again, it comes down to understanding investor behavior and workflows. Most ETH holders do one of several things with their ETH holdings:

- Hold it on exchange as collateral for futures/options trades

- Utilize it in DeFi applications

- Keep it in a wallet to be used for gas

- Hold it passively as an investment

While 1-3 aren’t likely to start staking, group #4 is. Given a chance to earn 0% versus 4-5%, for the same risk (not including the risk of counterparty failure), a passive ETH holder will immediately choose option 4. Not to mention all funds that hold ETH and want to be more productive with their ETH investments. Opening up liquidity for those who would have otherwise already staked (if not for the illiquidity) is likely to have a more positive impact than the negative effect caused by any withdrawals.

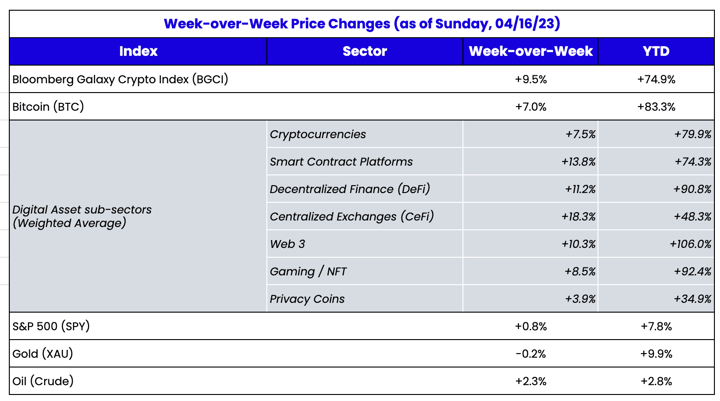

The result: ETH jumped +15% last week. Ethereum layer-2 protocols (ARB and OP) gained 33% and 13%, respectively. Liquid staking providers (LDO, RPL and FXS) rose 4%, 24%, and 13%, respectively. And many other Ethereum-based applications generically gained 10% or more as well.