Source: TradingView, CNBC, Bloomberg, Messari

Crypto Continues To Ascend While Other Asset Classes Retrace

The week after the election saw double-digit gains across the digital assets ecosystem, but equities and bonds also staged a similar rally, perhaps diluting some of the crypto-specific excitement. Last week was different. Equities and bonds gave up a chunk of their post-election gains, and gold and oil fell hard, so it wouldn’t surprise you if digital assets surrendered some of their gains as well.

Only that didn’t happen. The crypto rally continued basically unabated.

Not only are we operating in a post-Biden / Gensler world fueled with optimism that some of the incredibly restrictive anti-crypto policies will abate, but President-elect Trump is also proactively filling various positions within the government with

pro-crypto appointees. This includes the creation of DOGE (

Department of Government Efficiency) run by Elon Musk, which just so happens to take on a new meaning for the Dogecoin memecoin (DOGE +33% w-o-w). Many of those who were already in government trying to push through crypto-friendly agendas are becoming more emboldened, like Senator Lummis, who proposed the

Bitcoin Act of 2024 bill to create a strategic Bitcoin reserve. Meanwhile, SEC Chairman Gary Gensler wrote what looks to be a

goodbye letter ahead of an expected resignation, though he takes the time to congratulate himself for successful crypto policy (something the

18 states suing him might disagree with). Moreover, many U.S.-based crypto businesses that have had to walk a fine line between fear and confusion are now throwing caution to the wind ahead of the expected political shift. Coinbase immediately

began listing memecoins like WIF and PEPE, while Robinhood listed new tokens and

re-listed SOL (after previously delisting it after the SEC demmed it a security).

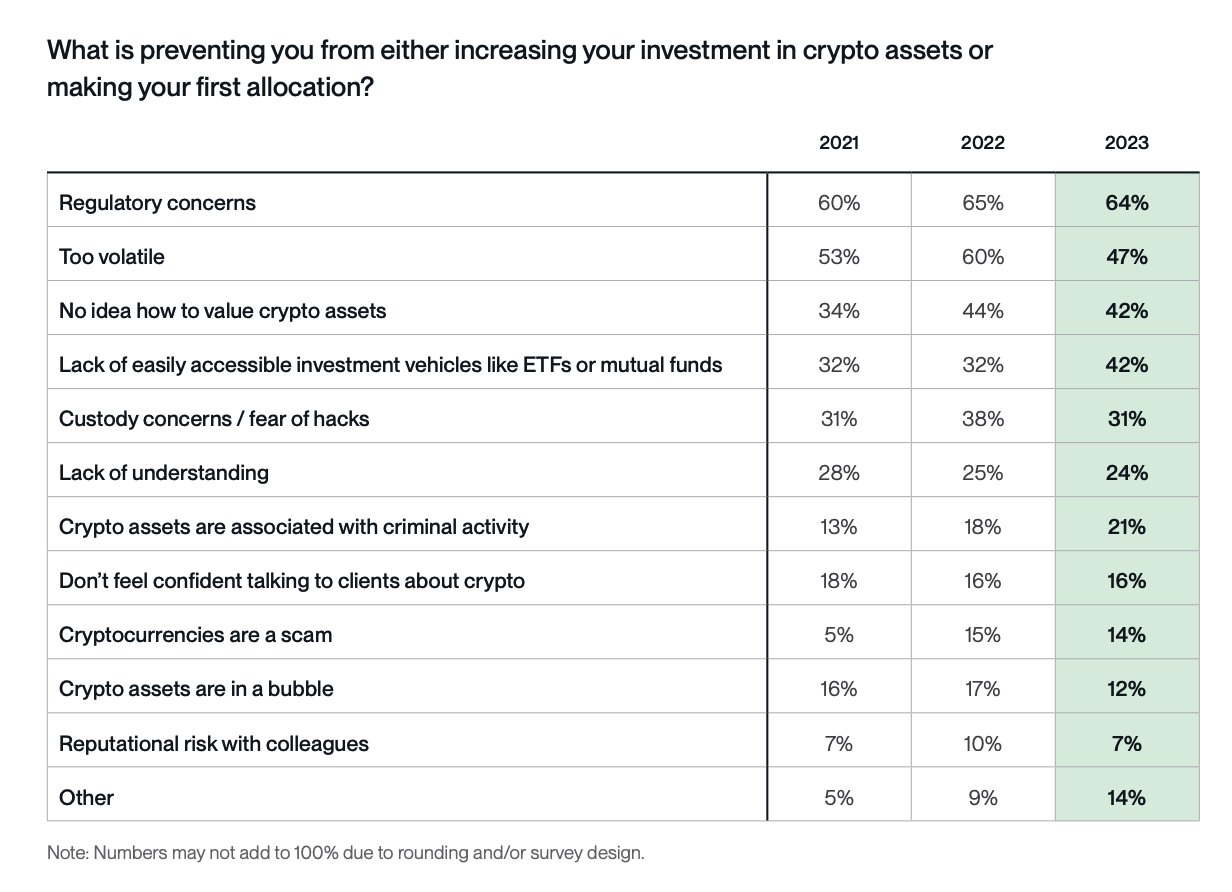

So yes, there’s reason for optimism beyond just a favorable macro dropback and equity rally. Real change is in the air, and it’s hard to ignore. As Bitwise Investments showed in their annual survey of hundreds of financial advisors, the number one reason holding back investment in crypto EVERY YEAR has been “regulatory concerns”... by a wide margin. Every other reason for not investing has been debunked over the past 5 years, but this one has been more sticky. And that, too is now going away. As we wrote about last week, the election was a game-changer for crypto investing in so many ways.

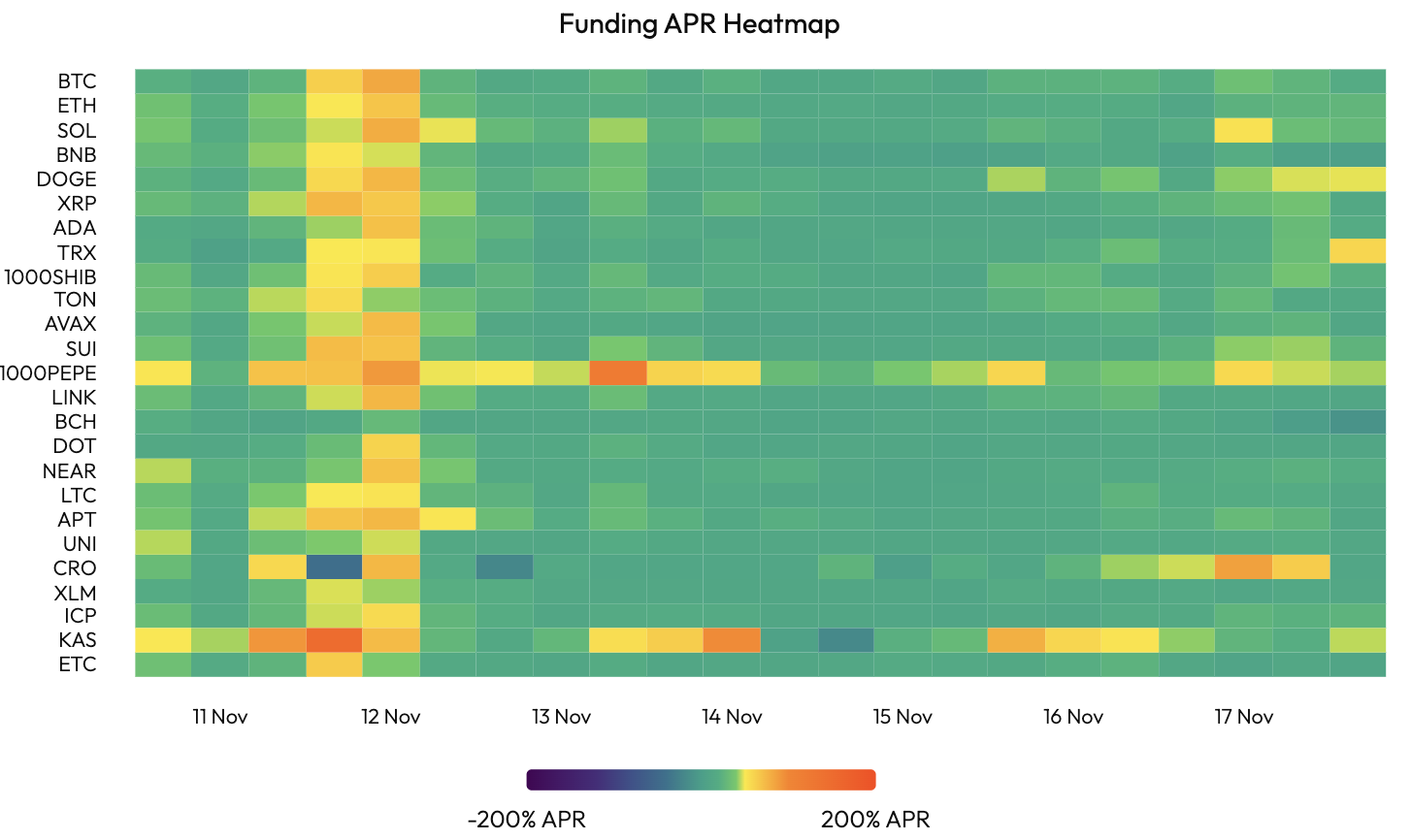

The problem with excitement in crypto is that, well, it’s still crypto. And markets tend to go from excitement to euphoria to overheating very quickly. You can see this in the funding rates on perpetual swaps, which jumped to levels not seen since the ETF-induced rally in March. Perpetual swaps (perps) are a popular way for traders to get leverage on their crypto exposure, with a positive funding rate indicating an optimistic bias by traders and a negative funding rate indicating a pessimistic bias (the rates indicate the cost for putting on the popular side of the trade, or the yield you earn if you take the other side). Not surprisingly, funding rates spiked last week briefly (yellow), but then cooled off after the market sold off briefly.

Source: Velo.xyz

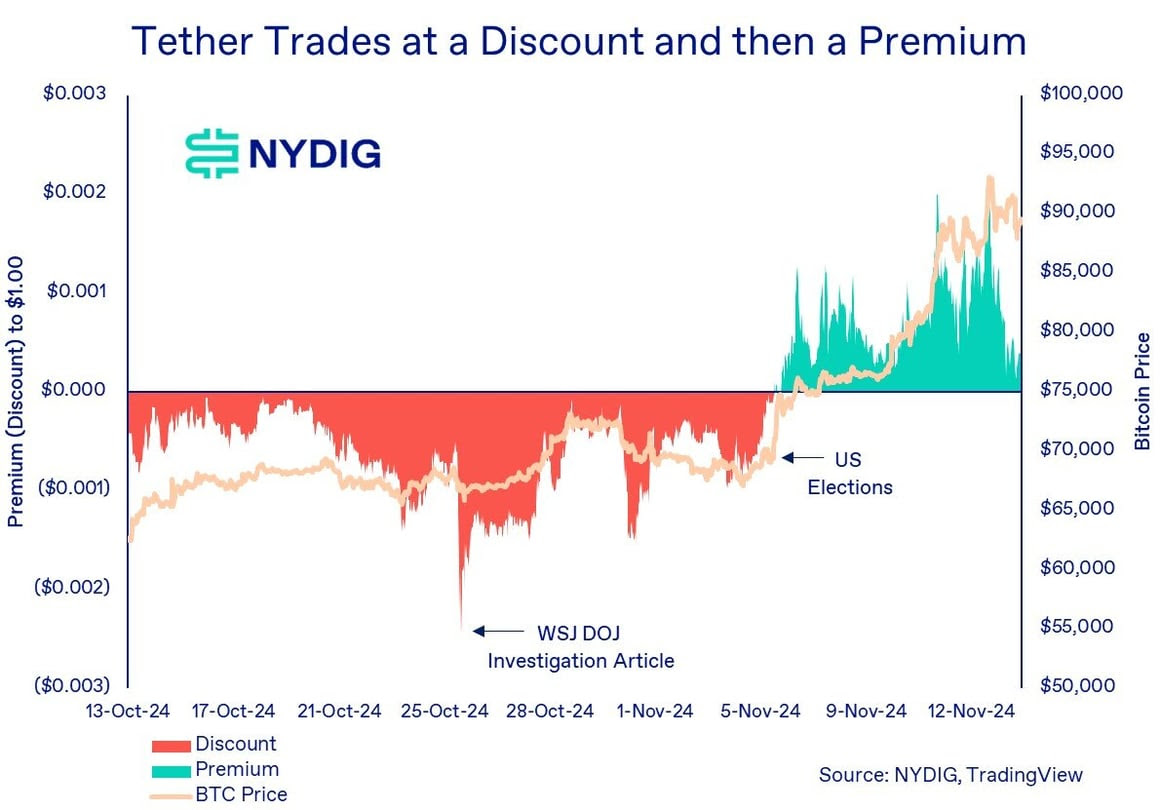

Meanwhile, the price of the largest stablecoin, Tether (USDT), has been trading at a substantial premium to $1.00, which indicates a strong demand for inflows into crypto exchanges. Tether’s price is similar to an ETF – when it is below $1.00, traders can buy USDT below “NAV”, and redeem it for dollars, capturing the arb, and when it is above $1.00, traders can short USDT above “NAV”, and create (or mint) new tokens to capture the arb. But when the price stays elevated like this, it shows that there is more new demand for new stablecoins than there is capital from trading firms who can arb it.

Source: NYDIG

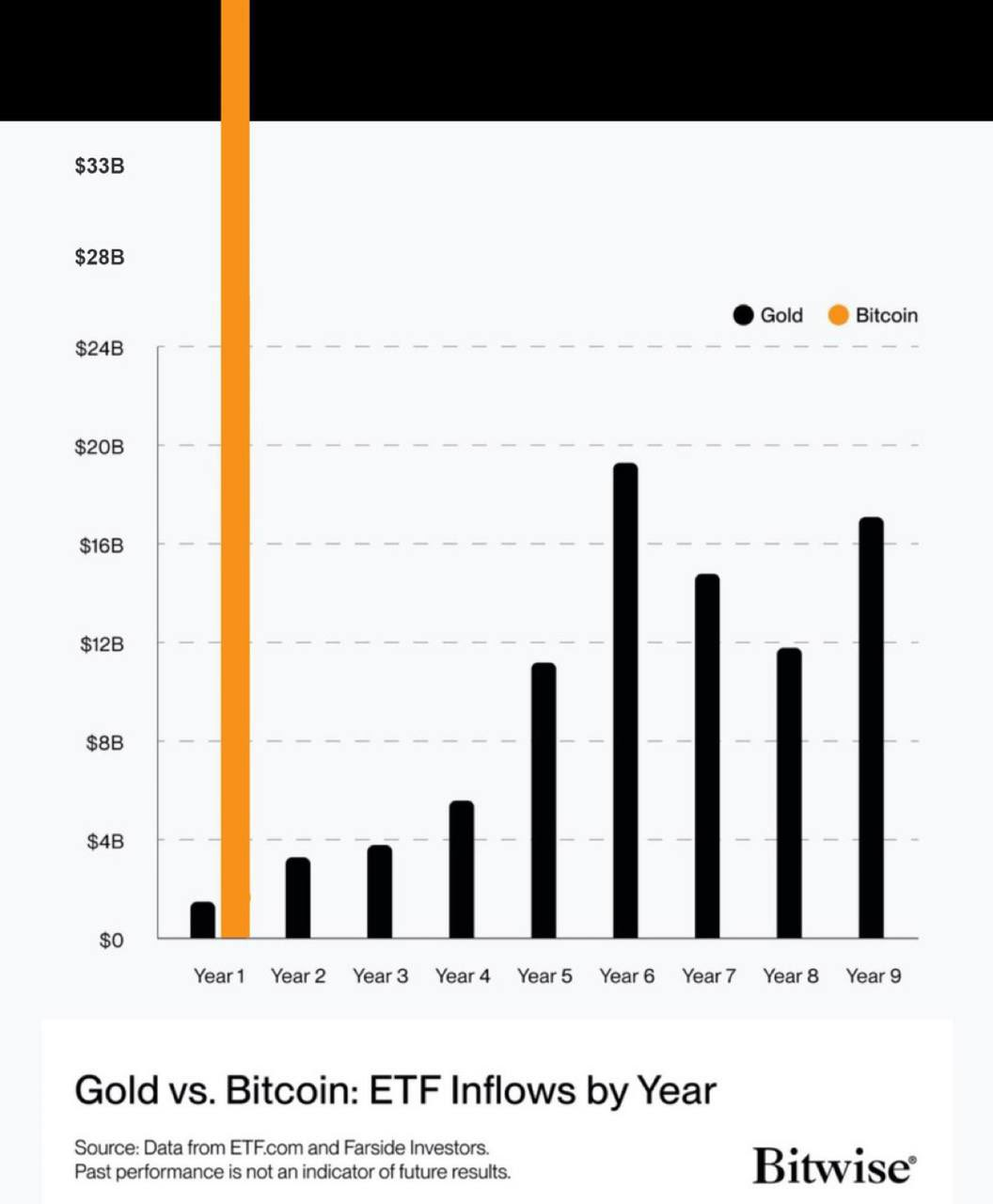

The Tether inflows show money entering directly into the crypto ecosystem, but of course, money continues to pour in indirectly as well via the BTC and ETH ETFs. Bitcoin and Ether ETFs

saw record inflows post-election, and the speed with which the Bitcoin ETFs have accumulated assets is completely unprecedented.

Source: Bitwise

But perhaps the most interesting development within crypto is the dispersion in prices. The total crypto market cap is

comfortably above all-time highs, but this does not mean every token is rallying. Sure, many of the large-cap, “mainstream” assets are higher, with BTC +104% YTD, SOL +120% YTD, and even ETH +32% YTD despite very low investor sentiment currently. But

less than 35% of our coverage universe is actually positive YTD. If your token is out of favor, it is severely out of favor, and the market continues to invest with an “out with the old, in with the new” mentality when it comes to token picking.

There has never really been a first-mover advantage in digital assets, outside of Bitcoin. Many of today’s leaders were second or third iterations, for example:

- Uniswap was not the first Automated Market Maker (AMM) decentralized exchange (Bancor was)

- Coinbase and Binance were not the first exchanges (Mt. Gox, Bitstamp, etc)

- Tether was not the first stablecoin (bitUSD)

- Hyperliquid was not the first perpetual decentralized derivatives exchange (dYdX)

- AAVE was not the first on-chain money market (Compound)

- Polymarket was not the first prediction market (Augur)

- Blur was not the first NFT exchange (OpenSea)

- Metamask was not the first EVM wallet (Mist)

But the “newer is better” investing mantra regarding unproven tokens has really changed the investment psyche. Unlike traditional equity investing, where investors tend to ride their winners, pushing the best of the best companies into trillion-dollar market caps, crypto seems to do the opposite, where last week’s winner is immediately dumped in favor of the new token du jour. Many investors just want to catch lightning in a bottle, and the best way to do this is to take a lot of shots on venture-like newcomers.

Moreover, we used to see sector rotation, especially during the bull markets of 2020 and 2021 (rise of DeFi, NFTs, stablecoins, gaming, file storage, etc). This made sense as new developments within crypto took place frequently. So far this year, especially in the last few weeks, we’ve seen less sector rotation and more single-name outperformance. When BTC rallies, it hasn’t led to rallies in other cryptocurrencies. When certain smart contract protocols rally (like SOL and SUI lately), it hasn’t led to broad participation (ETH, AVAX, and many others have lagged). Even when memecoins rally, it’s very token-specific.

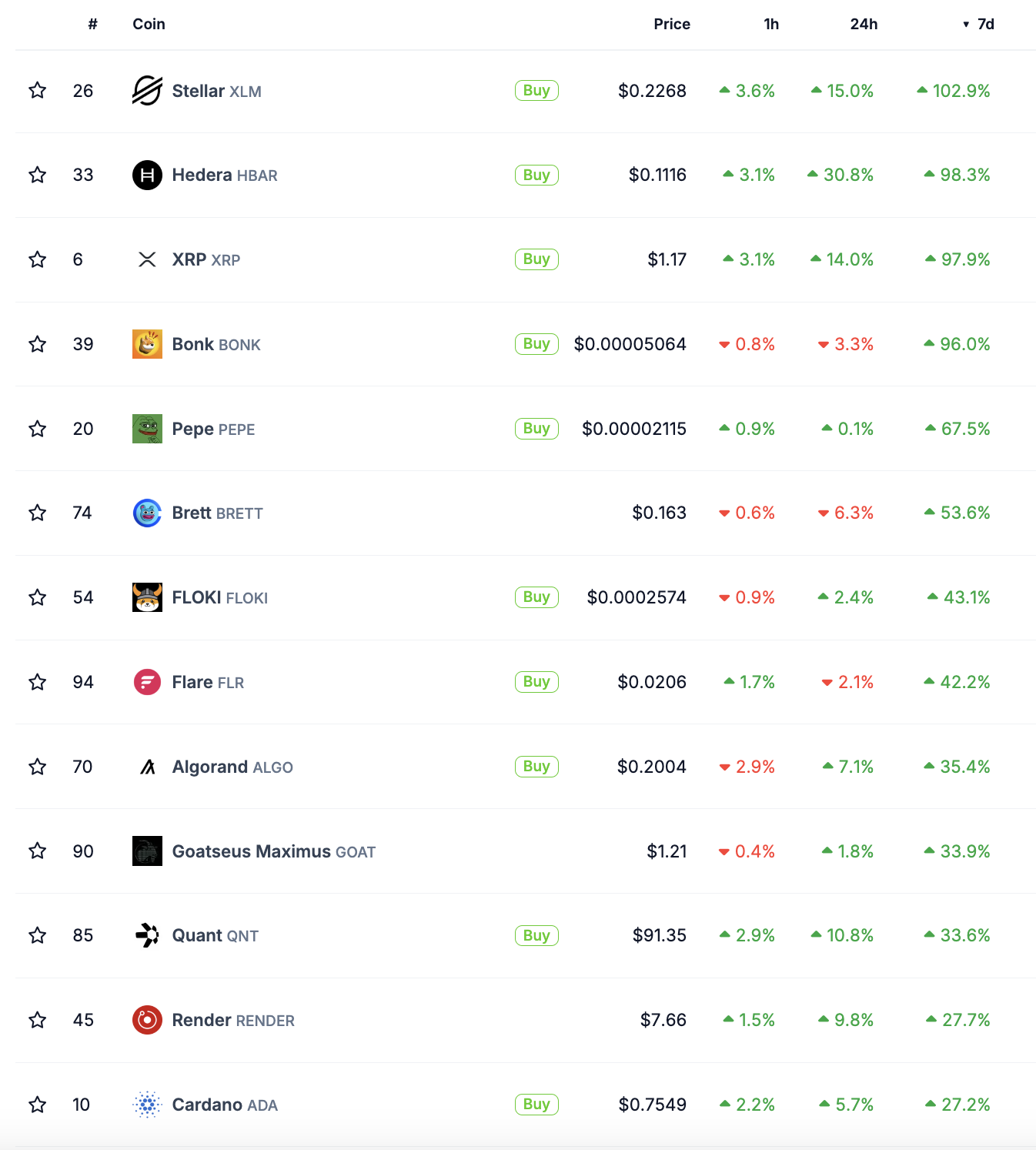

Last week introduced a new category – zombie tokens – which we may need to add to our

Digital Asset taxonomy. Zombie tokens are those that once tried to build something real, failed to gain any traction, yet never needed to file for bankruptcy or dissolve because the token sales kept the project afloat. Last week’s price leaders included EOS, XRP, XLM, ADA, ETC, HBAR, ALGO and LTC. If that looks like a who’s who from 2017, it is.

Source: Coingecko

Perhaps people logged back into Coinbase for the first time in years, and just went back to buying what they already owned, even if these projects have been pretty much left for dead within the more active and engaged crypto communities. While it's easy to compartmentalize memecoins (which are just fun to trade but make no effort to build an actual underlying product) from real products and services that use a token as a part of their cap structure (most projects within DeFi, DePin, AI, NFTs, gaming), it’s much harder to figure out what these zombie tokens are. They were once actually competing in the currency / smart contract race with real products, but now are just memes of crypto’s past?

The post-election hype continues, but the dispersion in price returns is baffling even the most knowledgeable crypto investors.