Source: TradingView, CNBC, Bloomberg, Messari

The Fake Bitcoin ETF News

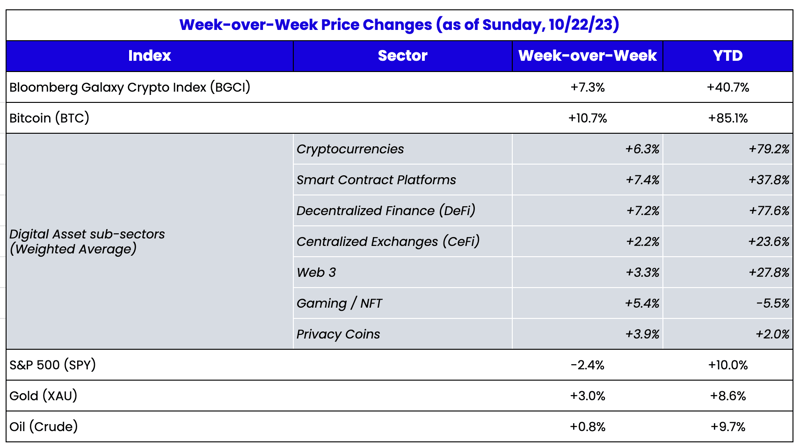

Stocks way down

Bonds way down

Crypto way up

Three years ago, no one would bat an eye at that statement. But after 2022 tricked so many into thinking that digital assets are correlated to stocks and bonds, many are left scratching their heads at the

new old normal. We opined last week

why this may be happening, and were not terribly surprised to see another week of digital assets strength at the expense of bonds and equities. In short, a debt spiral leads to a loss of confidence in banks and governments and a repricing of risk-free rates amidst record supply, which is bad for bonds and equity valuation models, but good for alternative forms of wealth and money creation. While stocks overall have held in better than most expected, bonds continue to rack up losses. Below are the long bond historical drawdowns for the past 100 years. We’re in pretty unchartered territory.

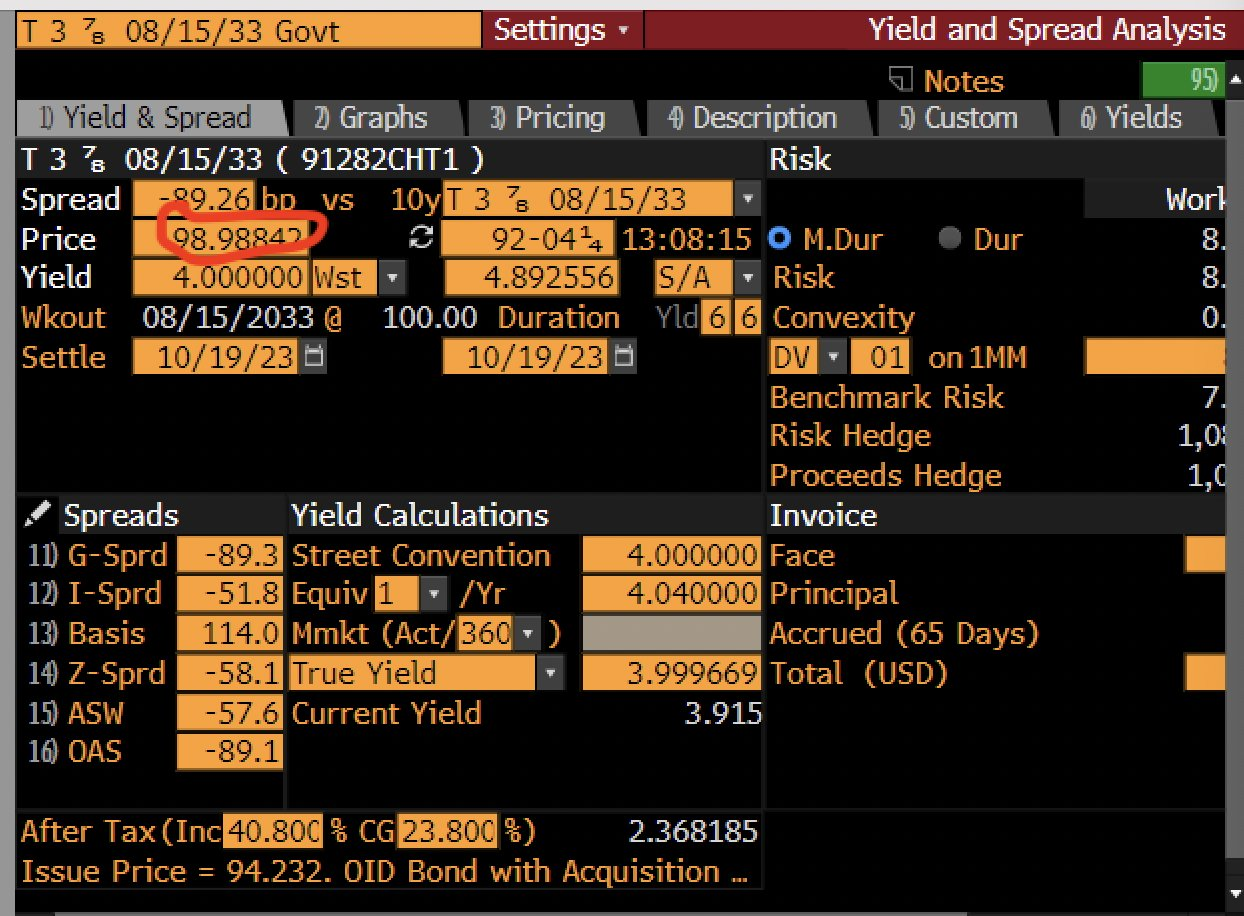

The past few months haven’t been much better. The ability to get 4% yields on the 10-year U.S. Treasury was a bogey for many investors. It reached 4.00% on Aug 9th.

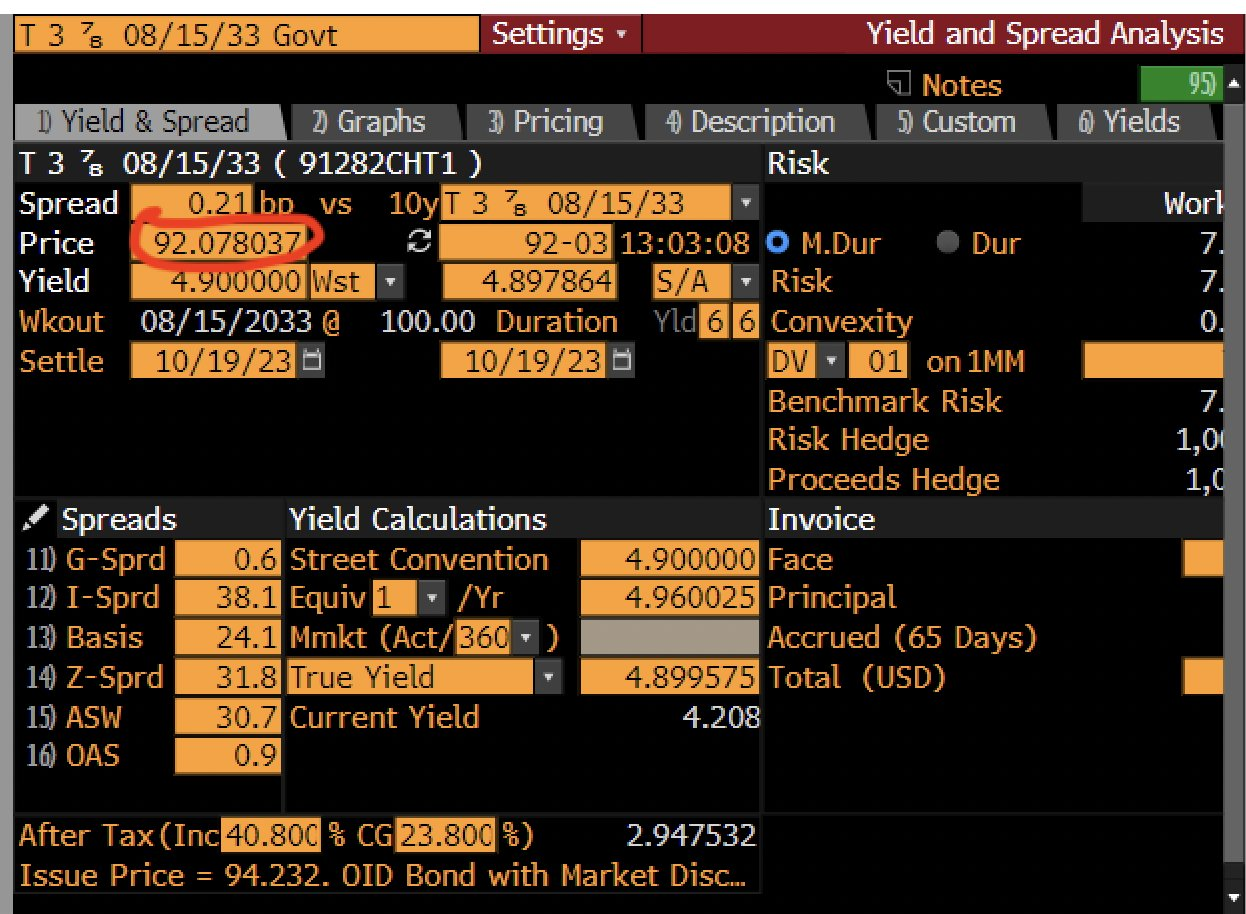

A little over 2 months later, the 10-year U.S. Treasury is at 4.99%. This equates to over a 7% loss if you bought bonds at 4%. Almost two year's worth of coupons were lost in two-and-a-half months.

Source: Bloomberg

That said, one week of data is not enough to confirm a trend. In fact, there was a very important piece of idiosyncratic news that may have muddied our thesis. The Bitcoin ETF was finally approved! Or at least, that is what was

inaccurately announced by CoinTelegraph.

Source: Twitter (Deleted)

Blackrock denied it. The

SEC denied it. Yet immediately following the post, Bitcoin surged 7% in roughly 30 minutes and caused over $100 million in short liquidations. While the market immediately gave back the gains, over the course of the rest of the week, we saw a steady climb higher in price back to the weekly highs, culminating in a weekend push to new highs. It’s hard to believe that the ETF itself isn’t priced in, given Bloomberg’s own ETF research team (Eric Balchunas and James Seyffart) continues to put the odds of spot BTC ETF approval before end-of-year 2023 at 75% and 95% by EOY 2024. But perhaps we all underestimated just how underinvested investors are in digital assets, and how little new money is needed to cause significant swings in price.

The fake news itself has been covered at length. So we won’t go further on the news itself. But I do want to delve deeper into the “market manipulation” claims that many were quick to point out after the mistake made by CoinTelegraph.

First, this type of “market manipulation” isn’t unique at all to digital assets. There is plenty of precedent when it comes to misleading headlines causing large market reactions. In 2013, for example, the Associated Press X/Twitter account was hacked and a headline said the White House was attacked. This resulted in

hundreds of billions of losses in equities and debt. More recently, there was an

AI-generated image of the Pentagon exploding, which caused another ripple effect on equity and bond markets. Perhaps the best analogy outside of digital assets is when there is a leak about FDA drug approvals, which can result in huge moves in biotech stocks. It doesn't matter what asset class you are trading; erroneous headlines can create whipsaw price action, and regulation is designed to catch and punish bad actors, not prevent it.

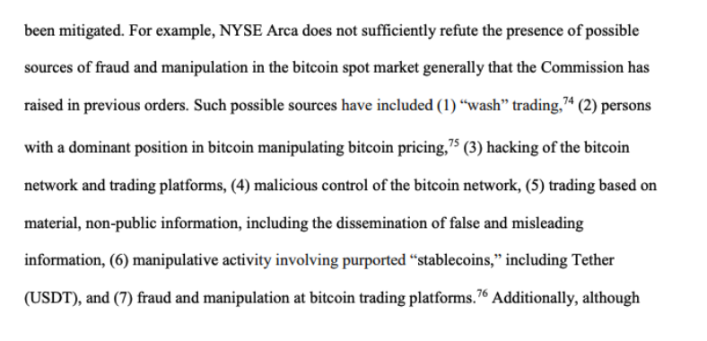

Second, the market manipulation that the SEC has historically referenced in its steadfast refusal to approve a Bitcoin ETF has nothing to do with a rogue media outlet inaccurately reporting news that people/bots then trade on. If you read the SEC’s “arbitrary and capricious” comments on why they have denied a Bitcoin ETF, only 1 of the 7 concerns about fraud and manipulation have anything to do with false headlines (#5: trading based on material, non-public information, including the dissemination of false and misleading information). But it is highly unlikely that a one-off trigger-happy intern at a trade media outlet can be considered “false and misleading information”.

Source: SEC

That being said, it of course is not the first time that this has happened in crypto markets either. The most prominent example was the

September 2021 Walmart-Litecoin incident, where an unknown individual was able to get a news wire service to issue a press release under Walmart’s name, claiming to have integrated Litecoin as a form of payment at the megastore giant. This incident swung LTC up and then down 30% in about the same time as BTC went up and then down 7% this time. So there is some reason to believe that this will happen again.

But again, regulation isn’t going to stop these events from happening, and these manipulation events have nothing to do with digital assets themselves. The digital assets industry is simply a new place where investors and traders can take risks, and as such, it will attract some criminals, some computer hackers, some fraudsters and pump and dumpers, and some sloppy interns… just like every other industry.