As an event-driven fund, Arca is constantly researching to find information that could impact asset price, independent of the broader market. Each month we’ll identify and share particular themes that emerge in the cryptomarkets, that lend itself to event-driven investments. Below we explore two event-driven themes that shaped our investment thesis over the past few months:

Coinbase Listings

Corporate Actions

Catalyst #1: Coinbase Listings

Once thought the golden ticket for cryptoassets, the price moves offered by a listing on Coinbase may now be dead. Below we explore the three latest tokens to list and how each one has had an increasingly diminished impact on price.

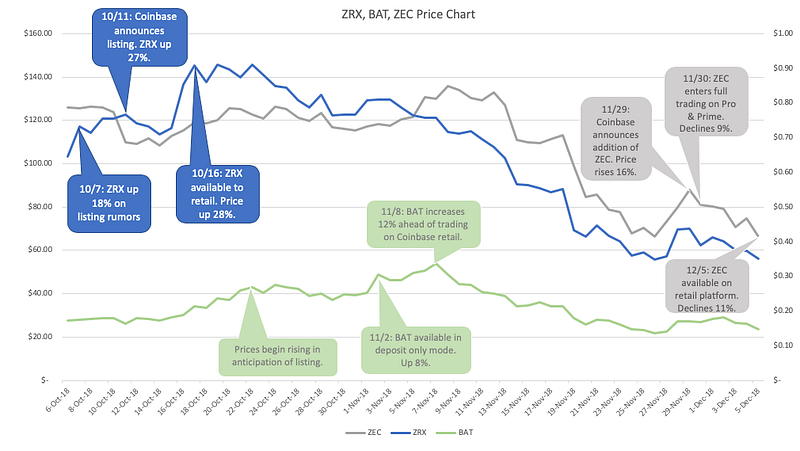

1. 0x Protocol (ZRX) — The catalyst was strong with this one

A Coinbase listing for 0x was long rumored: the project is an Ethereum darling, advisors to the project are also executives at Coinbase, and unlike most projects, 0x has a launched and operating product. A few days before an official announcement was made, the price of 0x ran up 18% after screenshots circulated showing 0x listed in a Beta version of Coinbase’s platform. The theory was borne out as four days later, Coinbase announced that 0x was open for trading on Coinbase Prime (the institutional platform), popping the price up 27%. On October 16, 0x became available on Coinbase’s retail platform during which the token shot up an additional 38% in less than half a day and was trading as high as $1.20 (up from $0.50 the prior month). Prices retraced almost immediately as sophisticated early investors began selling into the retail demand.

Screenshot that circulated showed ZRX on Coinbase prior to it actually being available

2. Basic Attention Token (BAT) — It worked once, let’s run it back

Basic Attention Token was on the Coinbase listing shortlist for well over a year. Back in March 2017, Coinbase CEO, Brian Armstrong, tweeted that BAT was “exactly the sort of token we’d like to support”. This early support, coupled with the project’s strong team and token design, promised a bright future for BAT. The price of BAT had been steadily on the rise following ZRX’s listing, as speculation spread that BAT would be up next. Following the ZRX price spike and subsequent fall, the Coinbase team recognized that listing a token with little information for retail was not the right strategy for a regulated exchange, and sought to remedy their listing process beginning with BAT. On November 2 (a quiet Friday afternoon), Coinbase announced via its Medium, Twitter and email lists that it would be listing BAT on Coinbase Pro and Prime. However, unlike during ZRX’s listing, BAT began in “deposit- only” mode for at least 12 hours to build up liquidity for the order book. Full trading did not become available until after the weekend on November 5. With this incremental roll out ahead of a weekend, price only increased 8% on the announcement and then another 9% once full trading was available. BAT increased again by 12% between November 5 and 8 when trading became available on Coinbase’s retail platform. The token hit a high of $0.34 before tumbling down with the rest of the crypto market throughout the remainder of November.

3. Zcash (ZEC) — Fool me once, shame on you, fool me twice, shame on me

Following ZRX and BAT’s listings, and subsequent 50%+ declines, the Arca team hypothesized that the Coinbase catalyst might be officially dead, right as the next cycle of the crypto bear market hit. But that didn’t deter Coinbase from listing Zcash. ZEC was shortlisted this summer along with ZRX and BAT so it was no surprise that it was the next cryptoasset to be added to the platform. On November 29, amidst a market that was down 40% on the month, Coinbase announced it would be listing ZEC, again keeping to a slow rollout plan. ZEC saw a short-lived pop of 16% on the initial news and remained flat as it entered full trading the following day. The anti-catalyst concluded on December 5, when Zcash was rolled out on Coinbase’s retail platform only to see an 11% decline over the course of the day. Twitter was up in arms over the price decline, some even declaring that a Coinbase listing was now “the kiss of death”. Only time will tell.

Bottom line: a Coinbase listing does not create additional fundamental value for an asset, therefore assets that are listed quickly drop back down in price. The long-term value of broad retail exposure offered by a Coinbase listing is something that may be felt over the course of many years, not from a quick flip during a two week period. That said, these three events were transparent, and profitable, as long as expectations and price targets were tempered with each subsequent listing. One might even question Coinbase’s motives here. Since every newly listed token is paired only with USDC, it’s possible these listings serve no purpose other than to build AUM for the USDC stabletoken as newly listed tokens are sold for USDC.

Catalyst #2: Corporate Actions and the Rise of Crypto Activism

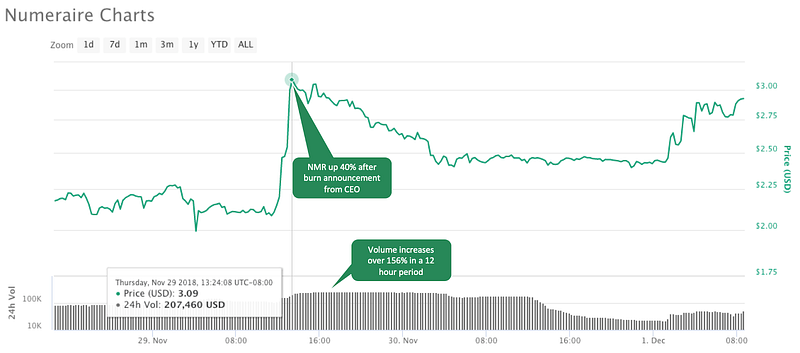

First of all, shout out to@TwoBitIdiot (Ryan Selkis),@ericturnr (Eric Turner) and the@Messariteam for raising this point. Last week, Numerai’s CEO, Richard Craib, announced that in an effort to decentralize its network, the company will reduce/burn about 45% of total supply down to approximately 11M. The market reacted favorably to the news as the Numeraire (NMR) token jumped 40% to $2.80 before settling in the $2.40 range on the announcement date.

The (non-legal) takeaway here is obvious… burning excess supply increases perceived scarcity value which should drive the token price higher. While unilateral corporate actions like this certainly help short term @price action, some could argue that the increase was insufficient. In other words, NMR may still be undervalued because the burned tokens should not impact total network value, so theoretically a roughly 50% supply decrease means each coin should have doubled in price (Note, at the time of this writing NMR is ~$3.20 so the market is starting to correct the perceived mispricing).

Nonetheless, we think Numerai’s decision will resonate with other token projects looking to improve investor optics and generate interest in the project as there is no downside to the decision (tokens are a zero basis asset). So as a catalyst driven hedge fund in a bear market, we started thinking about:

i) other pre-mined coins ii) whose treasury supply exceeded the circulating float which iii) didn’t have an obvious need for the massive excess supply

We discuss certain projects (among others) fitting these criteria: Spankchain (SPANK), Gnosis, (GNO) and Polymath (POLY).

Spankchain just downsized 33% of its workforce to reduce its cash burn. If $1M of its $3M reserves are held in crypto (presumably in SPANK/Booty tokens), then presumably a higher valued coin may help offset operating costs associated with running the platform (assuming increased selling pressure doesn’t deflate the price). This can and arguably should serve as a catalyst for a coin burn.

Polymath, a company which facilitates securitized token offerings (STOs), holds ~500M POLY or roughly 50% of total supply subject to a 4 year distribution schedule. Other than viewing the token as a free capital raise under the guise of “bootstrapping network effects”, we are not really sure why the platform even needs a token especially considering other STO service providers (Harbour and Open Finance) don’t have one. Considering there is no obvious need for that kind of a massive treasury supply (let alone a token), we think POLY could be a candidate for a token burn which would boost its price and drive interest to the platform helping them stand out from other STO competitors.

Gnosis is a decentralized prediction market similar to Augur, which raised ~$12.5M in April 2017 in exchange for issuing just 5% of the supply. The remaining tokens are held in Treasury to help develop the platform, pay employees and raise funds in the future. Per Gnosis’ timeline, the prediction platform has been in beta mode since Q4 2017 with only 3 live markets and its attempts to expand its developer ecosystem have generally failed to attract quality talent.

Let’s state the obvious… prediction markets need users to make predictions. A well-publicized coin burn should boost the price which would help drive interest and users to the platform. Combining a higher token price and a more active user base with a higher cash value payout for developer challenges should help bootstrap network effects during this bear market. Finally, to the extent Gnosis needs to raise additional funds in the future, a higher token price would obviate the need for selling a greater percentage of the remaining treasury supply. Again all upside and limited (if any) downside.

While we are in the early stages of crypto “corporate action”, we expect Numerai’s decision to kick-start similar activity from other projects looking to increase their visibility and improve “Hodler” optics. Projects can have many different reasons for burning (generate user interest, offset operating costs, etc.), but if the end result is increased interest, more usage and adoption, and a higher token price in the short run then that may be just enough to survive the cold bear market.

Subscribe For the Latest Blockchain News & Analysis

Disclaimer: This commentary is provided as general information only and is in no way intended as investment advice, investment research, legal advice, tax advice, a research report, or a recommendation. Any decision to invest or take any other action with respect to any investments discussed in this commentary may involve risks not discussed, and therefore, such decisions should not be based solely on the information contained in this document. Please consult your own financial/legal/tax professional.

Statements in this communication may include forward-looking information and/or may be based on various assumptions. The forward-looking statements and other views or opinions expressed are those of the author, and are made as of the date of this publication. Actual future results or occurrences may differ significantly from those anticipated and there is no guarantee that any particular outcome will come to pass. The statements made herein are subject to change at any time. Arca disclaims any obligation to update or revise any statements or views expressed herein. Past performance is not a guarantee of future results and there can be no assurance that any future results will be realized. Some or all of the information provided herein may be or be based on statements of opinion. In addition, certain information provided herein may be based on third-party sources, which is believed to be accurate, but has not been independently verified. Arca and/or certain of its affiliates and/or clients may now, or in the future, hold a financial interest in investments that are the same as or substantially similar to the investments discussed in this commentary. No claims are made as to the profitability of such financial interests, now, in the past or in the future and Arca and/or its clients may sell such financial interests at any time. The information provided herein is not intended to be, nor should it be construed as an offer to sell or a solicitation of any offer to buy any securities, or a solicitation to provide investment advisory services.