What happened this week in the Crypto markets?

What Goes Up, Must Come Down — Crypto Unable To Sustain Gains

The overall crypto market gained anywhere from 1–5% last week, depending on which Index you prefer to look at. However, the casual observer may not notice what is occurring, as watching Bitcoin alone is not painting an accurate picture of overall market depth, volatility or even fundamentals (yes, there are fundamentals in crypto). In fact, BTC was largely unchanged last week (again), even as over half of the Top 100 tokens by market cap gained or lost over 5% (36 tokens fell more than 5%; while 16 gained more than 5% week-over-week).

Diving deeper, the broader crypto market began rallying on Tuesday with gains as much as 5–10% across the board, but much of these early gains were eventually offset by a slow grind lower throughout the back-half of the week. We mentioned last week how a lack of market participants beyond just tradersis holding the crypto market back. Well, another factor holding the market back is a lack of “real” catalysts (something with which Arca spends a lot of time analyzing and investing around) — and there is a stark difference between how the market treats “weak” catalysts versus “strong” catalysts. While somewhat arbitrarily defined:

- Weak catalysts (such as technical analysis, listing on popular exchanges, or hard forks) are generally met with fast run-ups and equally fast sell-offs. This leads to a zero-sum game with unfortunate new buyers often lacking a chair when the music stops. Recent examples can be seen with BCH’s upcoming fork, and Coinbase’s recent listings of BAT and ZRX. In all three instances, prices ran up 50–100%, but eventually retraced most if not all of the gains. These catalysts really don’t mean anything with regard to the future value of the token, and active management (i.e. sell into strength) is needed to lock in gains.

- By contrast, strong catalysts (such as partnership announcements, transaction increases, hacks, etc) generally lead to more sustainable price moves. For example, XRP jumped well over 100% in September after announcing partnership growth and stronger sales. While XRP also gave back some of the gains, the token still remains almost 80% higher than pre-announcement as this positive catalyst actually leads to real growth potential.

Thus far, weaker catalysts have outpaced stronger catalysts, which is why most crypto rallies eventually stall. Both types of catalysts can be profitable of course, but it’s important to distinguish between trades and investments.

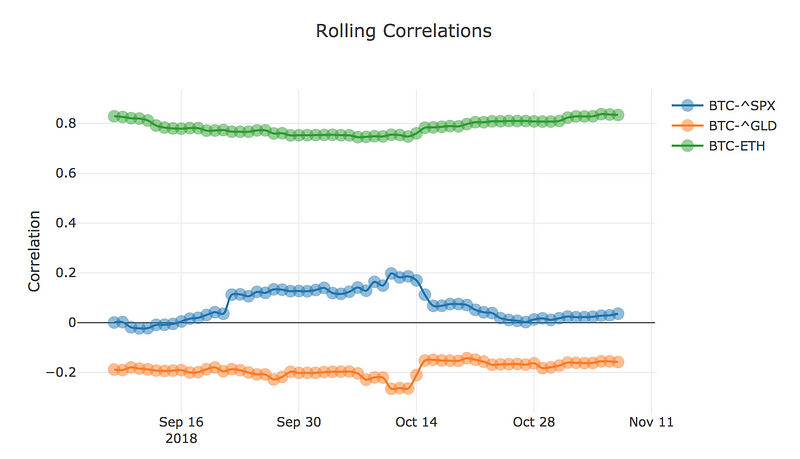

Correlations Are Still Low

Alongside crypto’s mild rally last week, it’s worth noting that US equities also gained 2–3% last week, while Asian equities were flat to -3%. But overall correlation does not seem to be picking up meaningfully between crypto and other asset classes.

BTC exhibits high correlation with ETH & other tokens, but low correlation to other asset classes

Sentiment Should Be Improving

Once again, a positive news backdrop underpinned BTC’s stagnation and a mild rally by the rest of the crypto market, with more new entrants and involvement from large institutions. Amongst these:

- The market continues to gear up for the launch of Bakkt, with speculation that this may trigger a bull run. What this means for Bitcoin (and thus, other digital assets that remain highly correlated to Bitcoin), remains to be seen, but it is being viewed as a positive data point.

- In addition, although there have been many recent crackdowns by the SEC, clear guidance from the SEC on how to handle crypto and ICOs will be a long term net positive for the industry, as it removes a large overhang on the market.

- The MACD index from Galaxy had its first positive divergence, leading many to speculate that crypto is headed for another bull run before 2018 comes to a close.

- Finally, while October 2018 bucked this trend, there is a case to be made for the seasonality of the crypto market, which generally sees its largest gains in the fourth quarter.

Bitcoin (BTC) Monthly Returns since 2013

Change is Hard to Recognize Amongst Incumbents

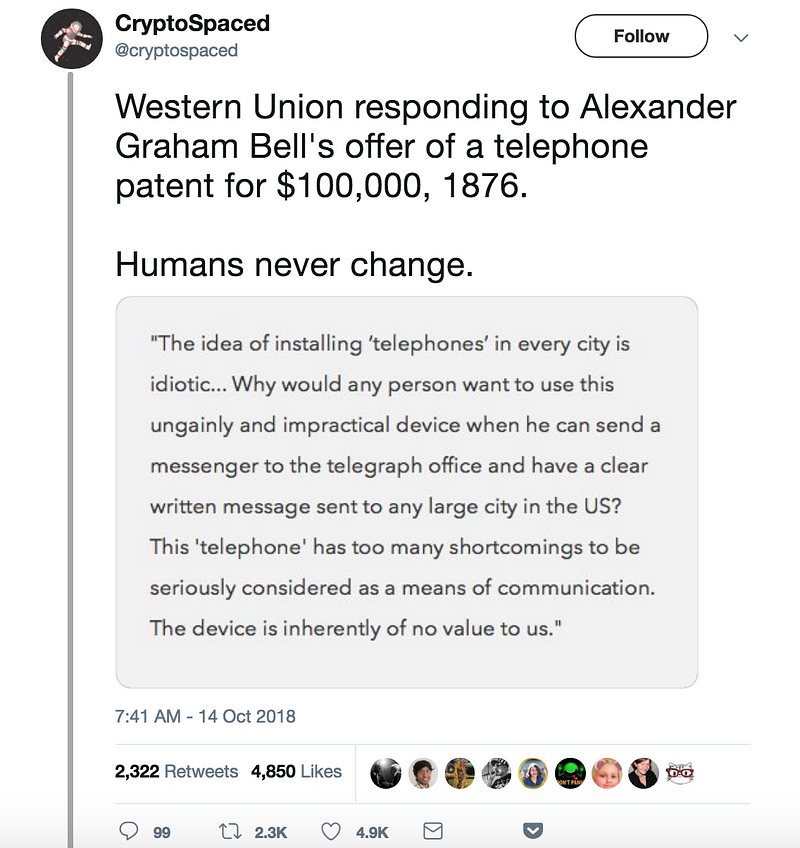

And finally, we were encouraged by news this week that a consortium of fifteen banks has begun working with The Depository Trust & Clearing Corporation (DTCC) to use a blockchain-based system for trading credit derivatives. While this may not ultimately be that impactful, it sure beats the alternative narratives of JP Morgan, Berkshire Hathaway and Nouriel Roubini, all of whom continue to act like Bitcoin and other digital assets offer no threat to existing business models. Perhaps they should re-read how Western Union viewed the telephone:

Notable Movers and Shakers

We continue to see similar patterns as the previous week, with tokens like BAT, XLM, and BCH moving on idiosyncratic news and events, while the rest of the market moves more on overall sentiment.

- Basic Attention Token (BAT) had an up-and-down week, rising as much as 27% mid-week before retracing 33% and finishing down 16% week-over-week. If you recall, earlier this month BAT was listed on Coinbase’s Prime and Pro platforms which drove the price up 17%. BAT CEO, Brandon Eich, added fuel to the mid-week BAT momentum with an ambiguous announcement in a podcast, which alluded to BAT partnering with a site “that has 80 million ad-blocking users a month”. When Coinbase announced support for BAT trading on its mobile app, the token saw a quick 12% jump, only to be followed by a 21% decline. The token has now normalized in price at about $0.25 which is where it was trading prior to the Coinbase listing announcement but still up roughly 20% since rumors began swirling. Worth noting, Coinbase’s last token listing (ZRX) had similar issues — rising ahead of listing and quickly retracing once retail investors entered the market. Coinbase tried to rectify this problem with the BAT listing, but will once again have to go back to the drawing board.

- Bitcoin Cash (BCH) was another volatile token, rising as much as 16% mid-week only to lose steam and end the week down 5% as the realities of the hard fork set in. Many market participants like to buy tokens ahead of a fork, thinking they will be receiving a “free dividend” in the form of the newly created tokens, but it’s often a game of cat and mouse, as those who get left holding the bag typically see rapid price deductions once the fork is complete. In the meantime, crypto exchange Poloniex is offering pre-fork trading of the two new forked assets, and early numbers indicate that Bitcoin SV (BCHSV) will not fare well compared to BitcoinABC (BCHABC).

- WAX Token (WAX) gained 48% last week after the network’s transaction count spiked on Bioactivity. However, since then reports have come out that indicate some of the transactions may be attributed to spam.

- Decentraland (MANA) spiked 21% after news that a virtual piece of land sold for $215,000. Decentraland is an ethereum based virtual reality representation of the globe, where users can buy and sell parcels of land.

- Other notable mentions: GoChain (GO) rose 23% on it’s announced a partnership with LINKCHAIN, and RChain (RHOC) rose 22%, riding the effects of its node release two weeks ago.

What We’re Reading this Week

The SEC has had a busy week, first with the promise of “plain English guidance on ICOs” followed by enforcement action against EtherDelta’s founder on Thursday. Zachary Coburn, who has not confirmed or denied the allegations, has agreed to pay almost $400,000 in disgorgement and fines to the SEC for his part in founding the exchange. According to a report from last week, we can expect many more of these enforcement actions from the SEC before the end of the year.

According to a recent study produced by Nature Sustainability, mining Bitcoin consumes more energy than mining copper, gold and silver. Specifically, it is more than three times the cost to mine gold on a per dollar basis. Although not explicitly highlighted, reports such as as these remind us of the importance of developing alternatives to Proof-of-Work (PoW) mining systems that are not as energy consumptive.

We don’t like to touch on politics in these newsletters, but it’s worth noting that two pro-crypto candidates were elected following the US midterm elections on Tuesday. Regardless of your politics, we cannot stress enough the importance of having elected officials who understand cryptocurrencies and are therefore able to guide appropriate legislative decisions. Relatedly, this week’s midterms also brought up the topic of voting using blockchains. As a tamper-proof and cryptographically secure system, blockchains can potentially bring the voting process online, something that many have delayed over fears of hacking.

If 2017 was the year of ICOs and dApps, 2018 has been the year of reality as many market participants come to understand what is and isn’t suitable for blockchains. In this article, Mastodon, Peepeth, Memo (Twitter clones), and PeerTube (YouTube clone) are critiqued for their implementation of blockchain-based systems which are not necessary and in some cases prohibitively expensive.

According to a study from the University of Queensland, lack of options for investors to short cryptoassets is depressing downward price pressure. The study confirms a long-held theory in finance, the resale hypothesis, which states that “an asset tends to favor the most optimistic participants in a market (those with long bets) when two conditions persist: lots of disagreement about price and impediments to shorting the asset.” Through their testing, researchers discovered that the resale hypothesis applies to both mainstream tokens and altcoins.

Apparently, Pichai’s 11-year-old son has been mining Ethereum on the home PC, which Pichai built himself. He revealed that his son understands far more about the cryptocurrency industry than he himself does. “I realized he understood Ethereum better than how paper money works,” Pichai said.

Arca in the Press & on the Streets

- Arca CEO, Rayne Steinberg, and Arca Portfolio Manager, Jeff Dorman, spent last week in NYC meeting with investors. Perhaps the most important takeaway was how receptive investors are becoming to crypto given it’s near zero correlation to any other asset class, a fact not lost on those trying to find investments that can offset the recent (and upcoming) volatility in global equity and bond markets

- The Arca team, led by co-founder and Chief Legal Officer Phil Liu, will be in Washington DC tomorrow meeting with the SEC to discuss our plans to manage a US Treasury backed stabletoken, as filed last week.

And That’s Our Two Satoshis!

Thanks for reading everyone! Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA — Portfolio Manager

Katie Talati — Director of Research

Hassan Bassiri , CFA — Junior PM / Analyst

To learn more or talk to us about investing in digital assets and cryptocurrency

.jpg)