What happened this week in the Crypto markets?

Lulled to sleep until the bottom dropped out

Virtually no asset classes were safe in October, which is why November’s hot start to the crypto markets was such a breath of fresh air to investors earlier this month. For the first 2 weeks of November, it seemed crypto-assets were not only uncorrelated to equities and other asset classes but were starting to recover from a year-long selloff. Even at the outset of last week, when equities once again suffered big losses on Monday, high yield spreads widened as outflows intensified, and oil followed suit with a 7% decline on Tuesday… prices of digital assets barely budged leading to collective high fives amongst crypto enthusiasts.

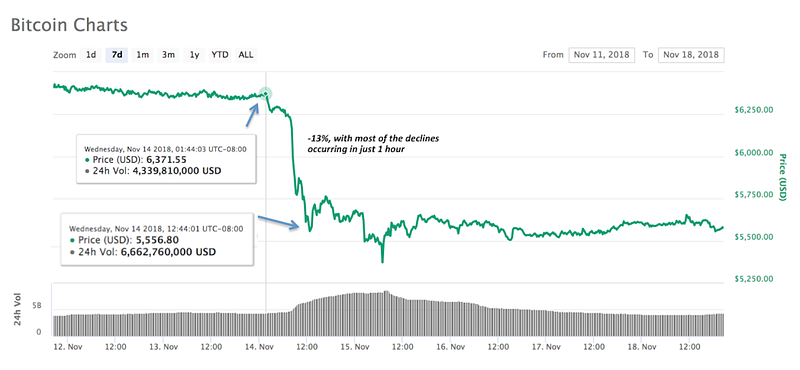

And then came Wednesday. The crypto market experienced yet another flash crash. In under a few hours, Bitcoin fell 13% and many other large-cap tokens lost 15% or more. Those that were long had virtually no escape, as the market went from point A to point B in an instant, with few trades in between. Perhaps even more bizarre than the decline itself, the market almost immediately settled into this new trading range following the crash, 13% below where we started the week (though this theory is being tested today as the crypto market has fallen another 10–15% as we write this). In any other asset class, when a large decline like this occurs, investors are faced with a decision:

- Buy on weakness since nothing has fundamentally changed other than price (usually leading to a recovery in prices)

- Adjust their valuation models lower to factor in whatever caused the selloff, lowering the market’s expectations of future value, leading to further losses

- Reduce risk until the situation becomes more clear

Any of these reactions tend to exacerbate the selloff or stop it dead in its tracks. But in crypto, it seems these selloffs are so random and frequent in nature that they just immediately reset the collective markets’ psyche, and all market participants simply agree to accept and transact at these new prices. Fundamentally nothing has changed other than price, but the price is typically the only thing that ever changes. And since valuation techniques are so new, there just isn’t enough data or universal support to definitively say “prices are now cheap”.

Graph of BTC price over past 7 days, focused on the Wednesday , Nov 14th selloff

Source: Coinmarketcap

This is the norm

Fortunately (or unfortunately), crypto market participants are becoming quite used to these types of “Flash crashes”. Using BTC as a market proxy, this was the 12th time this year that BTC has fallen by more than 10% in a single 24-hour period (though most of these had occurred earlier in the year — in fact, only 4 such events have occured in the past 6 months). Of course, there have also been 7 days this year where BTC has risen by 10% or more in a single day, many of which came only a few weeks after one of the steep declines.

Graph of BTC prices over past 6 months — with indications of 10%+ moves lower

So is crypto volatile or not?

If you had simply followed the media narrative the past few months, you may have been lulled to sleep by the lack of volatility in the crypto market (a notion that we at Arca have been outspokenly criticizing due to too narrow of a focus). As a result, if you only look at Bitcoin instead of the broader market, this spike in volatility may have caught you off guard ( BVOL , the rolling 30-day BTC annualized volatility metric, fell to 14% on 11/13 and rose dramatically to the 49% range following Wednesday’s selloff).

But it’s important to remember that these outsized moves are quite common, and will likely continue to be common until this asset class matures further. Those that can stomach the volatility have the chance to take advantage of opportunities not currently present in other asset classes. Those that choose to wait until the waters are more clear will undoubtedly feel safer with their decisions, but may miss out on some of what makes crypto special. As Outlier Ventures stated this week, “Volatility is a two-edged sword. On one end it has contributed to the growth of the ecosystem over the years by wild movements on token prices offering free PR for the industry. On the other, it has kept possible early adopters away due to the fear of seeing their savings being wiped away.“

Can the crypto asset class mature?

Yes. In fact, despite these large outsized moves, the maturation process has already started. As noted above, the steep price declines are already abading. In the last 6 months there have been half as many 10%+ declines as the first 5 months of 2018.

And looking deeper, there are other signs of maturation and institutionalization that will bring in more participants, make markets more efficient, and lower volatility even further. This includes:

- Improved Research — Crypto exchanges have gotten into the research game with models similar to sell-side research (like Circle Research and Binance Research), while stand-alone independent research firms with Wall Street pedigrees and institutional-caliber focus (like 51percent and Digital Asset Research ) give investors a trusted third party opinion.

- Institutional Investor valuation frameworks — The number of asset managers in crypto has steadily grown, but the caliber and AUM have not. Fortunately, some institutional investors are creating frameworks that will weed out the amateurs, and help those most capable flourish. Fund of Funds like Vision Hill have begun to create real due diligence and benchmarking frameworks, family office investors like David Nage have helped other family offices evaluate opportunities, and fintech investors like Michael Nov have explored avenues with which new players ( like M&A ) can enter and influence this space.

- Good, on the fly adjustments — The beauty of a new industry is that no one is dead-set in their ways yet. Even industry giants like Coinbase are still more speedboat than aircraft carrier in terms of their ability to maneuver changes quickly. For example, following their recent listing of a new token (ZRX), which led to trading chaos and exploitation of retail investors, they created and followed a new script just weeks later before listing another new token (BAT) in order to ensure a more stable order book.

While all of this may not give investors comfort today, these signs are pointing in the right direction. This is how an industry matures, and by the time it does, the opportunity may be gone.

Notable Movers and Shakers

The crypto market experienced some extraordinary moves last week, almost entirely negative (and by the looks of it may not be done moving lower). While we purposefully avoided the beaten-to-death topic of Bitcoin Cash (BCH) and its hostile fork in our commentary above, it may have been the driving force behind the broad-market selloff. Only a few tokens remained defensive last week. These tokens either moved higher due to real catalysts, or are tokens that are not mining-based systems, and therefore (hopefully) remained outside the major reaches of the Bitcoin Cash debacle.*

- NEM moved higher after its relisting on CoinCheck, gaining 12% early in the week before the entire market moved lower. NEM finished the week down only -3%.

- Outperforming the broader market, XRP and LINK managed to remain basically unchanged week-over-week amidst a sea of red. Elsewhere, MANA fell just -6% w-o-w as momentum seems to be gaining and transactions are increasing for this interesting blockchain-based virtual world.

- On the flip side, many of the most well-known and largest digital assets underperformed Bitcoin last week. This includes BCH (-25%), NEO (-24%), ADA (-21%) and LTC (-19%). Similarly, larger platforms like Ethereum (ETH) and Eos (EOS) continued their declines, falling 17% each.

*All numbers are for the period 11/11–11/18.

What We’re Reading this Week

Speaking at the FinTech Festival in Singapore this week, Christine Lagarde, head of the International Monetary Fund, advocates for central bank digital currency. Lagarde argues that it could potentially provide for greater financial inclusion, security and consumer protection and privacy in payments. She balances her talk by also exploring the potential shortfalls of a central bank issuing digital currencies.

On Friday, the SEC announced that they have charged and settled with two ICOs, Airfox and Paragon Coin. Both conducted ICOs in 2017 and were charged with having conducted those offerings illegally as they did not register with the SEC or file for an exemption from registration. Thursday an article from the Wall Street Journal suggested that Erik Voorhes is being investigated by the SEC for his involvement in Salt Lending’s ICO back in 2017. Voorhes was banned from conducting a bitcoin offering back in 2014 for a period of 5 years. This latest investigation is whether he violated that ban. Finally late on Friday, the SEC issued a statement discussing each of the enforcement actions and outlining guidelines for digital asset issuance and trading.

Although Nvidia predicted this outcome at the close of the third quarter, the chip maker took a hammering last week, its shares dropping 17% after posting third quarter sales that missed expectations. The chip maker has done incredibly well over the last year as the crypto frenzy has driven up sales of CPUs and GPUs produced by Nvidia, the graphics cards used in crypto mining.

Oil companies BP, Shell, and Equinor, together with a few large banks, have united to create Vakt — an energy commodity trading platform based on the blockchain. They plan to utilize smart contract technology to reduce paperwork and friction when trading these commodities.

On November 15, Canaan’s IPO filing with the Hong Kong Stock Exchange officially lapsed. Canaan is one of three mining companies that have filed for an IPO (Ebang and Bitmain). As Canaan has not yet publicly announced the reason for the lapse, many have started to speculate that the company is facing many financial woes that are preventing a public offering.

Augur’s prediction market saw its largest ever market of $1m for the US Midterm Elections exceeding $2m in total volume. This marks an important milestone in the decentralized app’s history as it seeks to overtake centralized competitors like PredictIt and overcome hurdles around its settlement process.

ICYMI: Ripple Lab’s was served a lawsuit earlier this year alleging they made an unregistered securities offering with the sale of XRP. The lawsuit is currently being tried in the state of California but this week their attorney’s filed to have the lawsuit moved a federal court. If won, XRP would be the first cryptocurrency ruled as not a security which could have far reaching implications for the entire crypto market.

Vision Hill, a crypto fund-of-funds, published its Q3 hedge funds returns report. Notably, crypto hedge funds outperformed the Bletchley20 and the Galaxy Index by 2480 bps and ~200 bps, while underperforming Bitcoin by 1260 bps.

Arca in the Press & on the Street

- The Arca team, lead by co-founder and Chief Legal Officer Phil Liu, met with the SEC (voluntarily) last week to discuss our plans to manage a US Treasury backed stabletoken, as filed last week

And That’s Our Two Satoshis!

Thanks for reading everyone! Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA — Portfolio Manager

Katie Talati — Director of Research

Hassan Bassiri , CFA — Junior PM / Analyst

To learn more or talk to us about investing in digital assets and cryptocurrency

.jpg)