Welcome to the first edition of Signal to Noise where I attempt to break down the headline news of the week and put it into two piles: Signal; denoting it may affect and incite action in the crypto market & ecosystem, and Noise; denoting material which interferes with said action, but yet seem to take up our attention & mental space.

A quick note: The content provided in Signal to Noise is for informational purposes only, you should not construe any such information or other material as legal, tax, investment, financial, or other advice. Nothing contained in this blog constitutes a solicitation, recommendation, endorsement, or offer by Arca to buy or sell any securities or other financial instruments in this or in in any other jurisdiction.

Over the last two years a tremendous amount of news and information about the crypto ecosystem have been generated and captured in newsletters, podcasts and more. The crypto ecosystem now has burgeoning news and research operations with companies likeThe Block,Messari,Coindesk and more. With more operations in place there are a significant amount of headlines and more to “weed” out.

So let’s dig in and see what’s Signal and Noise!

Signal

In this section you can anticipate a focus on news and research focused on Institutional Investors investing & focusing on crypto, products/platforms shipping and launching, Corporations getting involved in the ecosystem, job moves into crypto and much more.

Institutional investors have long relied on financial infrastructure to manage the tens of trillions of global assets under management — the top 4 custodians alone have a market cap > $550bn. Yet much of the existing infrastructure will not immediately port to crypto given cyber and physical security risks, lack of insurance, regulatory uncertainty, new tech stacks, and complexities introduced by protocol nuances such as staking.

Meanwhile, crypto has captured institutional investors’ attention, withlow correlationto other assets and tremendous return potential. While that uptake has been slow, digital assets appear to be a logical additive component when constructing a diversified modern portfolio. As such, we see potential in the full stack of financial infrastructure necessary to meet institutional needs — custody, prime brokerage, liquidity, derivatives, research, margin / lending, and so on. We seeAnchorage,Skew,Compoundand others as the first wave of many businesses in this space.

Other aspects of the market they discuss are STO’s, NFT’s and Gaming and more. As a reminder Kleiner Perkins was formed in 1972 and were early investors in Amazon, AOL, Compaq, Electronic Arts, Google, Intuit, Macromedia, Netscape and Sun Microsystems. When they opine it’s probably worth a listen.

2. A Billionaire entering the crypto market: “Alan Howard’s Elwood Targets Big Investors for Digital Assets”. For those who don’t know Alan Howard or his firm Brevan Howard the company was co-founded in 2002; was described as one of the largest “macro hedge funds” in the world with $40 billion in AUM. As Mark Yusko tweets: #ProbablyAFad

Howard, a co-founder of Brevan Howard Asset Management, made sizablepersonal investmentsin cryptocurrencies in 2017.

The company said the new regulated products will cover the full spectrum of crypto-assets, Chief Executive Officer Bin Ren said in a phone interview. Elwood and Invesco Ltd. have alreadylaunchedan exchange-traded fund tied to companies that are developing blockchain technology, the ledger tool first created to facilitate Bitcoin transactions.

A new report by BlockData says blockchain money transfers are 388x faster and 127x cheaper than legacy financial systems — shedding new light on how blockchain-based financial solutions are poised to disrupt the remittance system status quo.

The report names Philippines-focused GCash, Nigeria-based SureRemit, and Singapore-based Instarem as notable blockchain-based remittance firms.

Per the report and according to the International Data Corporation (IDC), global spending on blockchain technology is expected to reach around $2.9 billion in 2019 as industries everywhere investigate ways to use blockchain to increase trust and address challenges around complexity, transparency, and security.

According to Cisco, 83% of executives believe trust is the cornerstone of the digital economy, and it’s expected that the blockchain market will reach $9.7 billion by 2021. Cisco also stated that 10% of the global GDP is likely to be stored on blockchains by 2027.

Cosmos, a highly anticipated blockchain itself designed to improve the interoperability between any number of other blockchains, has officially released a live software.

With the mining of its first block at 23:00 UTC, the project has launched Cosmos Hub, the first in a series ofproof-of-stake (PoS)blockchains that will be created in the Cosmos ecosystem.

Noise

In this section you can anticipate a focus on news and research that does not discuss building, does not discuss investors coming into the ecosystem via investment or careers, rather focuses on price, predictions of price and more.

While Tom does talk about adoption and news headlines like JPM Coin the prediction of price on Bitcoin and other cryptocurrencies hasn’t shown to be effective, and in all actuality, has in my opinion led to weakened sentiment.

From the technical point of view, Lee suggested keeping an eye on DMA200 (currently at $4,876). Bitcoin will cross it by August if the current momentum is maintained, according to the expert.

Point of order — I like Tom and respect him since he’s been in traditional finance for a long time; before launching Fundstrat he served as J.P. Morgan’s Chief Equity Strategist from 2007 to 2014.However, Back in May 2018, Tom was predicting a Bitcoin rally to $25,000 by the end of the year.I’ve advocated for a while that we need to get away from price predictions because we just don’t have the historical, empirical data yet. Yes Bitcoin has been around for 10 years, but of those 10 how many years has it been trading at an “Institutional” level…hint, not 10 years.

Coin Center also published the letter and highlighted the key component which lead to the headline:

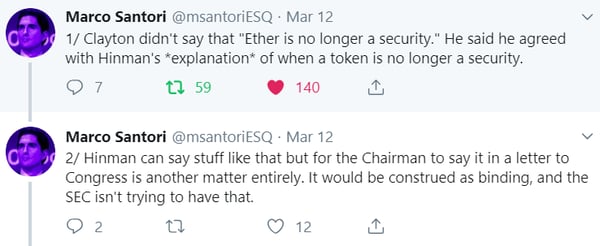

Your letter also asks whether I agree with certain statements concerning digital tokens in Director Hinman’s June 2018 speech. I agree that the analysis of whether a digital asset is offered or sold as a security is not static and does not strictly inhere to the instrument. A digital asset may be offered and sold initially as a security because it meets the definition of an investment contract, but that designation may change over time if the digital asset later is offered and sold in such a way that it will no longer meet that definition. I agree with Director Hinman’s explanation of how a digital asset transaction may no longer represent an investment contract if, for example, purchasers would no longer reasonably expect a person or group to carry out the essential managerial or entrepreneurial efforts. Under those circumstances, the digital asset may not represent an investment contract under the Howey framework.

3. The drama of Mt. Gox:Former Mt. Gox CEO Mark Karpeles Gets Suspended Jail Term. Have the issues with Mt. Gox affected sentiment among Institutional Investors? Sure…have we moved on? Absolutely. I put this in the let’s itch that scratch a little bit even-though it doesn’t nothing good for you, bucket.

Mark Karpeles, a central figure in the early days of Bitcoin who presided over the dramatic 2014 collapse of the world’s biggest cryptocurrency exchange, was found guilty of tampering with financial records but will likely avoid jail time after receiving a suspended sentence.

And there you have the first version of Signal to Noise! Comments, questions, additions and possible subtractions to Signal to Noise? Let me know atdavidn@ar.ca

To learn more or talk to us about investing in digital assets and cryptocurrency

Subscribe For the Latest Blockchain News & Analysis

Disclaimer: This commentary is provided as general information only and is in no way intended as investment advice, investment research, legal advice, tax advice, a research report, or a recommendation. Any decision to invest or take any other action with respect to any investments discussed in this commentary may involve risks not discussed, and therefore, such decisions should not be based solely on the information contained in this document. Please consult your own financial/legal/tax professional.

Statements in this communication may include forward-looking information and/or may be based on various assumptions. The forward-looking statements and other views or opinions expressed are those of the author, and are made as of the date of this publication. Actual future results or occurrences may differ significantly from those anticipated and there is no guarantee that any particular outcome will come to pass. The statements made herein are subject to change at any time. Arca disclaims any obligation to update or revise any statements or views expressed herein. Past performance is not a guarantee of future results and there can be no assurance that any future results will be realized. Some or all of the information provided herein may be or be based on statements of opinion. In addition, certain information provided herein may be based on third-party sources, which is believed to be accurate, but has not been independently verified. Arca and/or certain of its affiliates and/or clients may now, or in the future, hold a financial interest in investments that are the same as or substantially similar to the investments discussed in this commentary. No claims are made as to the profitability of such financial interests, now, in the past or in the future and Arca and/or its clients may sell such financial interests at any time. The information provided herein is not intended to be, nor should it be construed as an offer to sell or a solicitation of any offer to buy any securities, or a solicitation to provide investment advisory services.