Source: TradingView, CNBC, Bloomberg, Messari

The Market is Still Losing Its Mind… Part 2

Last week, we attempted to summate the U.S. president’s inauguration and subsequent TRUMP coin launch, using what we believed to be a rational and objective voice amidst a market frenzy that was hanging off both sides of an emotional teeter-totter. It was one of the most well-read pieces we’ve ever written (over 7 years). Hopefully, we calmed a few nerves.

But one week later, it feels as if the market is leaning even further towards the extremes yet again. The calls for both all-time highs and a massive crash are getting louder and louder. So here we are again, trying to make sense of it all.

First, let’s take a look at credit. Typically, credit spreads act as a leading indicator for any sort of financial crisis, and currently there is no indication of a credit crisis. High-yield credit spreads are still at the all-time tights. While this can, of course, change, this is like calling for a tsunami while looking over a glass-like morning lake. We’d be looking for some sort of hiccup in credit before making any broad sweeping conclusions about a sustained sell-off.

Second, while meme coins are getting destroyed, and the AI agent sub-sector has given back a lot of recent gains, the majority of what professional crypto investors would call the “real market” is holding up just fine. Looking just at a select list of leaders in each sector (cryptocurrency, smart contract protocols, DEX’s and Lend/borrow platforms), the weekly returns are as follows:

BTC -1%

ETH -1%

SOL +1%

HYPE +7%

AAVE -1%

Not exactly a sign of an apocalypse. Meanwhile, stocks were up last week, while the VIX, US Treasury yields, and the DXY were all down. Many crypto-native market participants are calling for armageddon simply because a handful of overvalued (or zero value) tokens are -10% or more, while a handful of equity investors are calling for a crash because stock valuations are elevated and the hottest sector on earth (AI) has proven to be competitive (Hint: Competition is a good thing).

Third, the President of the United States followed through on almost all of his campaign promises in the first week of his Presidency with his Executive Orders. As Galaxy Digital wrote in their weekly blog to clients:

“The order explicitly makes it the policy of the United States that: self-custody, mining, validating, and transactional freedom should be protected; banks should not prevent lawful individuals or companies from fair access; the government must establish clear and progressive regulatory frameworks; and that the government should study whether and how to create a national digital assets stockpile. Coordinating all this will be difficult and the new Presidential Working Group on Digital Asset Markets will have its hands full.”

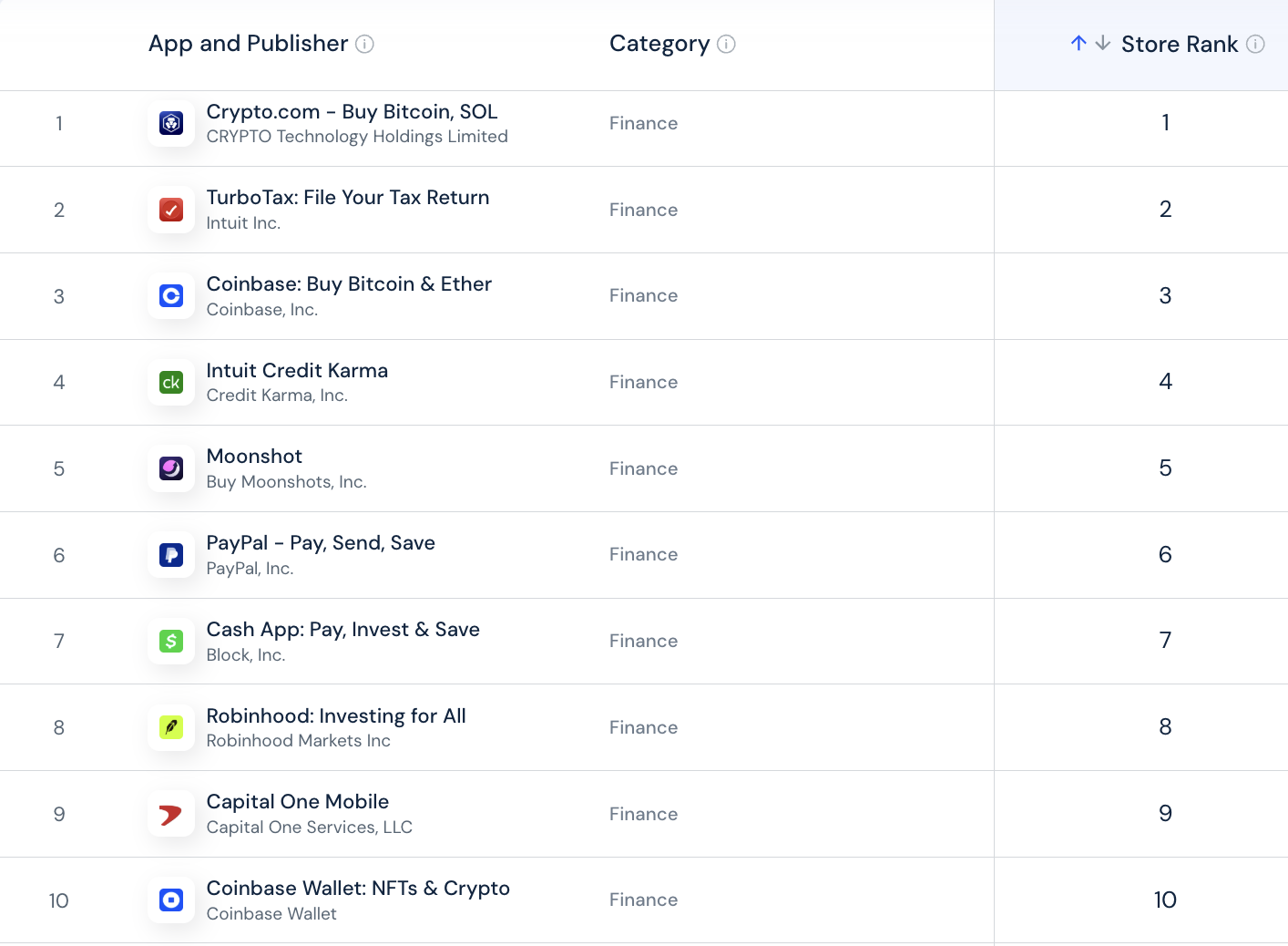

It may take time for price to catch up to the enormously positive pro-crypto advancements in the U.S. But it is interesting to see crypto-native investors calling for the “end of the cycle”, while our conversations with non-crypto-native investors suggest the exact opposite. Meanwhile, 7 of the 10 finance apps are currently crypto-native, or offering crypto-products.

It’s not entirely clear why the market is so on edge right now. However, one thesis is that easy money is over. There are simply too many tokens for the entire market to trade up together, and as such, the dispersion of returns going forward is likely to be massive. Over the past few years, many crypto traders made a lot of money with no real skill or thesis, and the writing is on the wall that this strategy won’t work going forward. So, even as the industry propels forward, many are feeling like they will be left behind.

The Potential Impact of the EO

Written by David Nage, Portfolio Manager at Arca

While we typically discuss the liquid markets, it’s helpful to view the market through the lens of venture investing occasionally. Specifically, how the U.S. presidential election impacted Q4 fundraising and how the executive orders will likely have a strong impact on 2025.

Crypto venture funding in 2024 reached ~$11.5-12 billion, marking a 7.48% increase from 2023's $10.7 billion, though remaining significantly below the peaks of 2021-2022 ($29 - 33.3 billion).

Despite the modest overall increase compared to prior bull markets, 2024's focus on infrastructure, early-stage deals, and technological development, particularly evident in Q4's strong performance, suggests a maturing market prioritizing fundamental development even as the mainstream is focused on “meme mania”. Infrastructure dominated the funding landscape with $5.5 billion deployed across 610+ deals, followed by Web3 ($3.3B) with significant DePIN activity ($1B+), NFTs/Gaming ($2.5B), and a resurgent DeFi sector seeing 530+ deals (+85% YoY). Early-stage investments led the way with a record 1,180+ pre-seed deals, while seed funding approached 2021's peak at $3.4B and Series A rounds totaled $2.8B across 175+ deals.

![]()

.png?width=663&height=323&name=unnamed%20(5).png)

Valuation Recovery: Despite a tough market for raising funds, median valuations for crypto-specific deals in 2024 showed signs of recovery. By Q3 2024, median pre-money valuations for crypto deals were at $23.8 million, slightly down from $25 million in Q2 but still indicating a stabilization or slight increase from the lows seen in 2023.

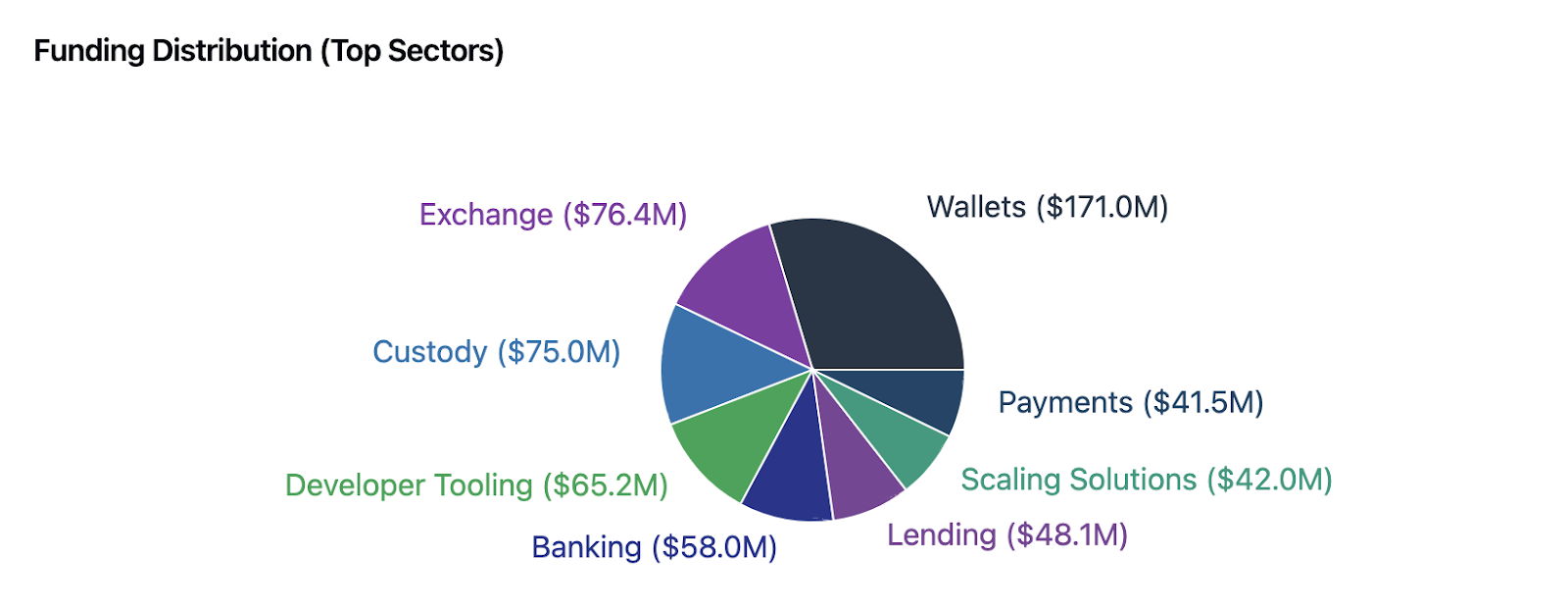

In Q1 2025 we have already seen $798M deployed across 133 rounds. Here’s a breakdown of them by sector:

Source: Messari Fundraising Data

If we forecast out for Q1 2025, taking the 133 deals done thus far in January and keeping them steady at that rate, we get to 399, which would be significantly lower than the 603 deals in Q1 2024, representing a 34% decrease in deal count. The $798 million invested so far in 2025 compares to $2.49 billion in total for Q1 2024, effectively 31% of Q1 2024 totals. Off of ETF approvals, new administrative change and some perceived regulatory wins in 2024 one might have expected a return to 2020-2021 levels that saw over $30B allocated per year. But we aren’t there…yet.

As Galaxy notes: “On an annualized basis, 2024 was the weakest year for crypto VC fundraising since 2020, with 79 new funds raising $5.1bn, well below the frenzy of 2021-2022.” Simply put, the dry powder isn’t there right now. So why has there been so much difficulty raising new funds in this market?

Two reasons:

- The top five largest token unlocks of 2024 released more than $5.4 billion into circulation, heavily impacting market dynamics. At least $150 billion in combined token unlocks are expected from 2024 to 2025, with approximately $82 billion absorbed in 2024 alone

- New token issuance died in Q2 2022 after FTX/Luna/BlockFi and has, up until the last few quarters, been dead on arrival. Then the dam broke after Q1 2024 with the belief the market was changing in light of the Bitcoin ETF and some perceived legal wins (SEC v Ripple, SEC v Coinbase), leading to an oversupply with not nearly enough dollar demand, leading to poor token performance.

- The reason why new token issuance was dead on arrival was due to lack of regulatory clarity and an administration here in the United States that was ruling by enforcement versus proactively working with the industry.

That all changed this week.

Strengthening American Leadership in Digital Financial Technology

President Donald Trump signed an executive order (EO) on January 23, 2025, titled "Strengthening American Leadership in Digital Financial Technology." A few key points from this EO:

- Establishment of a Working Group: The EO establishes the "Presidential Working Group on Digital Asset Markets," chaired by David Sacks, the White House AI and crypto czar. This group includes high-level officials from various departments like the Treasury and the SEC.

- Regulatory Framework: The group is tasked with developing a federal regulatory framework for digital assets, focusing on market structure, oversight, consumer protection, and risk management. They must identify current regulations affecting crypto within 30 days, recommend changes or rescissions within 60 days, and submit a comprehensive report within 180 days.

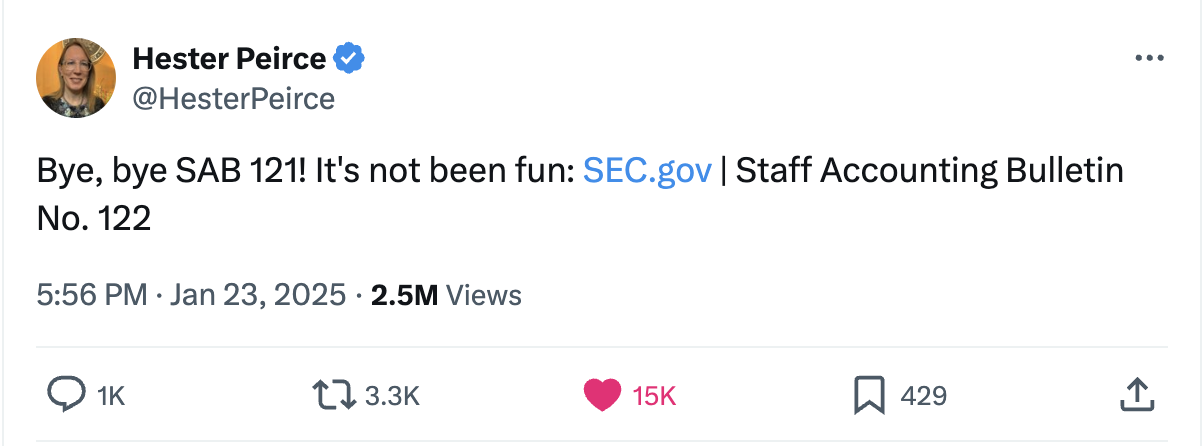

In addition to the EO, the market also received news of the repeal of SAB 121.

The repeal of SAB 121 and its replacement with SAB 122 could have several implications for H1 2025:

- Banking Integration: The removal of SAB 121's constraints could significantly boost the potential of banking integration with digital assets. With SAB 122 potentially offering a more favorable accounting treatment, more banks might be willing to offer custody services for digital assets.

- This was highlighted by the CEO of Bank of America this week in Davos: “If the rules come in and make it a real thing that you can actually do business with, you’ll find that the banking system will come in hard on the transactional side of it.”

- Institutional Access: Banks being more open to custody services could lead to significant capital inflow as institutions gain more confidence in the regulatory environment surrounding digital assets.

Banking Infrastructure and Market Development

The potential implementation of digital asset custody services by U.S. banks represents a watershed moment for the industry, though the barriers to entry remain significant. There are costs associated with that, include:

- Cold/hot wallet architecture

- Multi-signature controls

- Private key management systems

- Hardware security modules (HSMs)

- Air-gapped signing systems

- Geographic distribution

- Backup procedures

- Insurance coverage

With that in mind, these requirements and associated costs suggest that only banks with substantial resources and committed digital asset strategies will be early movers.

Leading banks will likely leverage existing state frameworks, particularly in Wyoming, Texas, and Nebraska, where regulatory clarity and supportive legislation exist. Wyoming's Special Purpose Depository Institution (SPDI) framework offers the most immediate path forward, potentially serving as a template for other states. If all goes to plan with the working group, the industry could see 15-20 banks establishing custody operations within H1 2025, primarily concentrated in these pioneer states.

The capital requirements and operational complexity suggest that a tiered adoption approach will emerge. Tier 1 global banks will likely establish comprehensive custody and trading services, while regional banks may initially partner with technology providers such as BitGo, Anchorage Digital or Coinbase Custody to offer more limited services. This stratification could create interesting market dynamics, with some regional banks potentially gaining competitive advantages through faster implementation of targeted services.

Insurance and Market Structure Development

These are key areas to watch. The insurance market perhaps represents the most critical bottleneck in the ecosystem's development. Lloyd's of London has been a provider of insurance coverage for the digital assets sector, however, there has been a significant offering gap in the market.

New entrants like AIG and Chubb could significantly expand market capacity, however, if we are going from 0-60 in the United States, and we see a surge of banks entering into offering custody and trading solutions, this level of insurance demand could drive up premiums initially as insurers adjust to the new risk landscape. Once the market stabilizes, competition might lower these costs. This underscores the importance of developing robust custodial infrastructure, including security measures, to mitigate risks and make insurance more viable.

The development of institutional-grade trading infrastructure requires significant investment. The high barrier to entry suggests that established players could dominate the initial market structure. Goldman Sachs has been actively involved in the crypto space. They restarted their cryptocurrency trading desk in March 2021 to deal in bitcoin futures and non-deliverable forwards for clients. Morgan Stanley has been ahead of its peers when it comes to crypto. It was the first major U.S. bank to offer Bitcoin funds to its clients in 2021, and last year, it took the lead in offering Bitcoin exchange-traded funds. There may be 5-7 major trading venues emerging within the first 90-120 after the EO was executed this week, primarily through the expansion of existing cryptocurrency exchanges and traditional financial institutions.

The transition to T+0 (same-day) settlement along with Delivery versus Payment (DVP) and Receive versus Payment (RVP) capabilities in the context of digital asset trading introduces significant technical and operational challenges for banks and trading venues. One of the primary challenges is in system upgrades. Existing trading and settlement systems are typically designed for T+2 or T+1 settlement cycles. Moving to T+0 requires substantial upgrades or even a complete overhaul of these systems to handle real-time transactions. This includes ensuring that all parts of the system (trading, clearing, settlement) can operate in sync.

Conclusion: A Market at an Inflection Point

The convergence of regulatory clarity through the new executive order, the repeal of SAB 121, and established state frameworks create an unprecedented opportunity for institutional adoption of digital assets in H1 2025. While venture funding is trending towards a potential decline in Q1 2025, this may represent the calm before a transformative storm in market infrastructure.

The path forward isn't without challenges. Banks face significant technical and operational hurdles in implementing custody solutions, with multi-million dollar initial setup costs. Insurance capacity remains a critical bottleneck, with current coverage falling well short of projected institutional demand. The requirement for T+0 settlement and robust DVP/RVP capabilities will require substantial system overhauls across the industry.

However, the frameworks emerging from pioneers like Wyoming, Texas, and Nebraska provide tested models for rapid deployment. Combined with the Working Group's expedited mandate and Bank of America's signal of institutional readiness, we could see a dramatic acceleration in banking adoption through H2 2025. This infrastructure build-out, backed by regulatory certainty and institutional demand, may create the foundation for the next phase of digital asset market maturity.

The key question isn't whether traditional finance will enter digital assets but rather how quickly the industry can scale its infrastructure to meet incoming institutional demand.