And That’s Our Two Satoshis!

Thanks for reading everyone!

Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA - Chief Investment Officer

Katie Talati - Director of Research

Hassan Bassiri, CFA - Portfolio Manager

Sasha Fleyshman - Portfolio Manager

Alex Woodard - Research Analyst

Nick Hotz, CFA - Research Analyst

Bodhi Pinker- Research Analyst

Wes Hansen - Director of Trading & Operations

Mike Geraci - Trader

Kyle Doane - Trader

David Nage - Principal, Venture Investing

Michael Dershewitz - Principal, Venture Investing

Michal Benedykcinski - Research Analyst

Andrew Masotti - Trading Operations

Topher Macpherson - Trading Operations

To learn more or talk to us about investing in digital assets and cryptocurrency

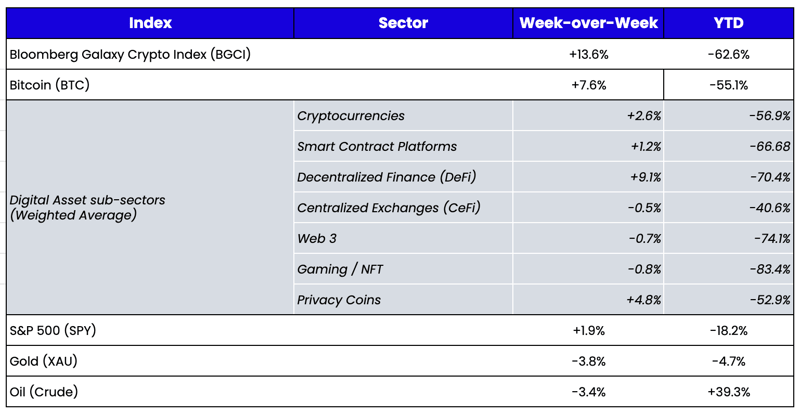

What Happened This Week in the Digital Assets Markets?

What Happened This Week in the Digital Assets Markets?