What Happened This Week in the Digital Assets Markets?

What Happened This Week in the Digital Assets Markets?

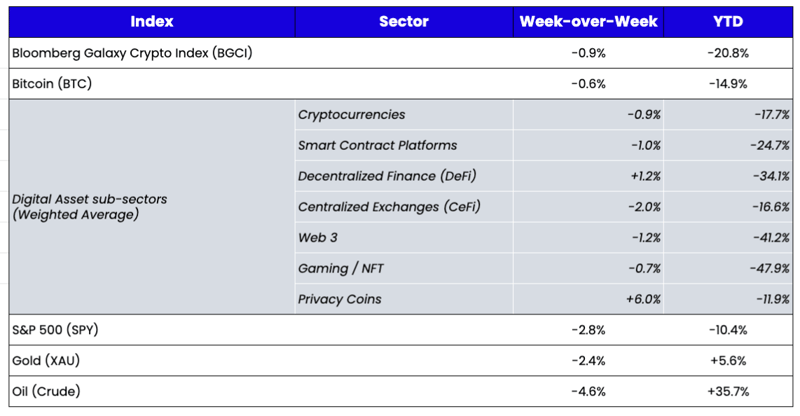

Week-over-Week Price Changes (as of Sunday, 4/25/22)

Source: TradingView, CNBC, Bloomberg, Messari

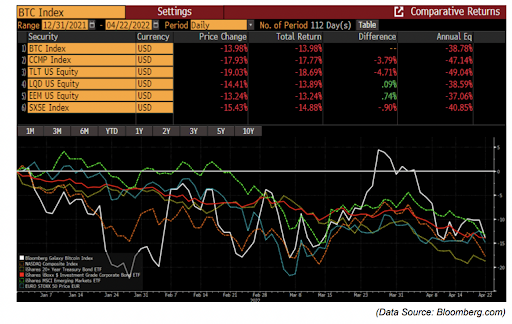

High Up-Capture and Low Down-Capture

Digital assets slightly outperformed traditional markets last week—a trend that will eventually matter when/if investors put money back to work. While the negative returns across digital assets, tech stocks, emerging market stocks, government, and corporate bonds all look quite similar in today’s macro/Fed-driven market, digital assets had amazingly high up-capture during good times the past three years, yet are showing very low down-capture during recent bad times. In other words, when a new asset class outperforms on the way up and on the way down, those characteristics will open eyes and eventually drive significant asset flows. Essentially, digital assets are providing the return that long/short equity and debt hedge funds have promised (and largely failed to deliver) for decades.

My Bank Forced Me Into DeFi

DeFi growth has been somewhat stagnant since November 2021. Activity has slowed amidst a dull, declining market, and the price of DeFi tokens has been straight down since peaking in February 2021. In addition, there has been a constant flow of hacks that have kept the media salivating over DeFi’s demise.

Though there are valid reasons to worry about DeFi, most concerns stem from those who have never engaged with it. If skeptics actually tried to use a DeFi application, they might be pleasantly surprised at how amazing it is. Last week, I was forced to turn to DeFi because traditional banking went silent on me during the course of an ordinary financial transaction. Here’s a detailed description of what happened to me (this account is from my personal experience and is not a reflection on, nor an official statement from, Arca):

- On April 6th, I requested an ACH withdrawal from my bank account via Coinbase to purchase ETH. Coinbase allows you to immediately spend the U.S. dollars even if your bank transaction hasn’t cleared (presumably because banks are good for the money even if it takes time for bank settlement to occur), so I bought the ETH. It’s a nice service by Coinbase, but it doesn’t work if banks unilaterally make opaque and inefficient decisions about your money (more on this later).

- On April 14th, Coinbase notified me that the payment never went through. My bank sent no notification that this was denied; I only found out because Coinbase told me. When I logged in to my bank account, I could see that my bank never initiated the payment.

- On April 15th, I re-initiated the payment. Once again, there was no notification from my bank that anything was wrong. On April 20th, I was informed once more by Coinbase that the payment never went through. Now I had 24 hours to make a payment, or else they would start liquidating the ETH that I just bought since I hadn’t actually paid for it (the ETH was down about 8% since purchase, so selling it for no reason wasn’t ideal).

- I called my bank immediately. After multiple disconnected calls, 5 interdepartmental transfers, and about 4 hours on the phone, I finally learned there was a freeze on my account. No payments were to be issued until the fraud department finished its work, which would take at least 48 hours. Don’t forget—this process started at least 9 days prior. For 9 days, I had no access to my own money, and no communication to notify me of the freeze.

So at this point, I was in a bind. I needed to make a payment immediately, but my hands were tied. My only hope was to use some of my investments as collateral to get a quick loan so that I could make a U.S. dollar payment. So here’s what I did:

- I sent ETH from a personal cold storage wallet to my MetaMask wallet, which took about 3 minutes to arrive.

- I deposited this ETH into Aave (a borrow/lend DeFi application with $11 billion of net deposits) at a 2x collateral ratio (I deposited 2x the amount I needed to borrow to ensure that I would not have any liquidations). That took about 2 minutes.

- Then, I borrowed USDC (U.S. dollar stablecoin) at a 3.6% annual rate in the exact amount I needed to make payment to Coinbase. This USDC showed up immediately in my MetaMask wallet since it was already connected to my Aave dashboard.

- I then bought 30 days of insurance to cover the principal I put at risk at Aave via Nexus Mutual at a 2.6% annual rate. That took about 5 minutes.

- Finally, I sent USDC directly to Coinbase, which covered the amount I used to purchase the ETH. That took about 3 minutes to clear from my wallet to Coinbase.

Ultimately, I spent about 15 minutes getting a large loan at a low rate and sending that money across multiple venues to complete a verifiable financial transaction. I am not engaging in money laundering, and it should not be overly complex for a bank to figure that out.

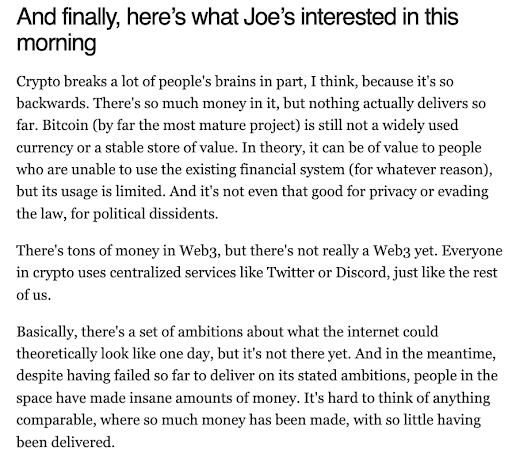

Now, I’ll admit this isn’t a perfect solution. It requires knowledge of the protocols and overcollateralization. But it is at the very least incredibly functional and helpful, especially when compared to the constraints of banks. Yet just this morning, Bloomberg journalist Joe Weisenthal wrote that crypto “does nothing,” only to pander to both sides of the extreme (crypto lovers and haters will give him a lot of attention for this), but he’s wrong. The use cases are evident, but most people don’t try them because they are scary, complicated, or unknown.

Source: Bloomberg email subscription from Joe Weisenthal “Five Things You Need to Know to Start Your Day”

I’ve been on record many times stating that February 2022 will be looked back upon as a major inflection point regarding how citizens across the world view their banks, brokerage accounts, and governments. Specifically, I wrote:

“Over the past six weeks, our society has discovered that money and stocks are not an asset—they are liabilities owed to you (typically by a broker or a bank). Whether or not you can ensure these entities pay you back in full is now in question due to recent activities in Canada, Russia, and the London Metals Exchange. This uncertainty has become a wide-reaching advertisement for ownership of bearer assets like digital assets.”

No one believes this is true until it happens to them. But it seems inevitable that it will, in fact, eventually happen to you. Curious why my assets were frozen?

A few months ago, I bought a house. To purchase this house, Citibank BEGGED me to get a mortgage through them, even though I held no assets with Citibank—I only have a Citibank-issued Costco credit card, which I pay off monthly from another bank account. Citi quickly and easily rushed to approve my loan and offered a 50 basis point reduction in my mortgage rate if I was willing to transfer a portion of my assets into a Citi checking or brokerage account. Not one issue arose during this process. Transferring money into Citi was made very easy. Paying a ton of fees and interest on a mortgage was made very easy. Not one person at Citi seemed to have any issues with me sending money or payments into Citi.

Once my new checking account was open, I only made a handful of transactions. I immediately paid my 2021 federal and state taxes via my new Citi checking account. No one seemed to have a problem with this since Citi is a national bank. Additionally, I made 2 monthly transactions to pay off my Citi-issued credit card bill. Again, no issues there.

But the subsequent transactions I attempted led Citibank to determine that my money was not my money—it was theirs. From their perspective, I was a potential criminal and they would decide whether or not I would regain access to my money.

Among those subsequent transactions was an investment I made as an LP into my own hedge fund—one of Arca’s many hedge fund strategies for which we have many U.S. investors. Arca’s funds are, of course, managed by Arca—a U.S.-based, SEC-registered investment adviser and U.S. tax-paying company. Yet because Arca is tagged as a “crypto company,” it took 3 phone calls from Citi’s fraud department before this wire transaction into my own hedge fund was finally approved. A week later, I initiated the transaction into Coinbase—a publicly-traded U.S. company from which Citibank earns banking and trading fees. Apparently, that was enough for Citibank’s hypocrisy to assume there was enough evidence to conclude that criminal activity was occurring.

Still more hilarious, no one at Citi communicated that any of this was happening (which is apparently legal), even though I had numerous failed transactions and at least a 9-day period when my account was locked and in “fraud review.” I even tried to send money back to Bank of America (the account from which I initially sent the money to Citibank to get my mortgage approved), but that transaction was also denied. Citi apparently has no problem taking money from Bank of America, but won't let it go back to Bank of America. What a savvy, veteran Wall Street move. Welcome to the Hotel California, where you can check out any time you like, but you may never leave.

At the end of the day, I’m still reliant on the U.S. banking system. Eventually, I still need to get my money out of my bank to repay my DeFi loan. I still need to utilize banking services to pay vendors, bills, and other services—for now. But let’s not sit on our high horse and pretend that DeFi doesn’t solve some real world problems while ignoring the multitude of issues that banks and brokerages continue to cause. A paradigm shift in the existing financial system is long overdue. I believe that transformation will happen through the real-world accessibility to manage life functions that DeFi enables.

In the meantime, I’ll wait for Citi’s fraud department to decide my fate, even though it seems that the only suspicious activity committed at this point was by Citi itself for holding my money indefinitely and not telling me about it. While I wait, I’m sure Citi will have no problem debiting my account to auto-pay themselves for my mortgage and Citi credit card bills. No conflict of interest at Citi, right?

Competition is a Good Thing

This probably deserves a longer writeup, but in the last few weeks, the two biggest stories were:

- Coinbase launched its NFT platform to compete with OpenSea

- Tron and Near protocols are launching algorithmic stablecoins to compete with Terra Luna’s UST

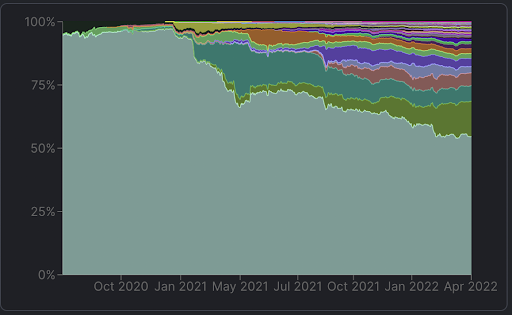

Both have been touted as the death of the incumbents, as OpenSea and Luna have dominant market shares in their respective categories (NFT trading and algorithmic stablecoins). But this has been happening since the advent of blockchain. Competition comes in, and immediately the market starts to focus on the inevitable winner-take-all outcome. The “Ethereum killers” didn’t kill Ethereum—they took a chunk out of Ethereum’s monopolistic market share (ETH share of total Layer 1 TVL in light green below), but Ethereum also grew tremendously as the overall pie of blockchain transactions grew (ETH TVL grew 10x).

|

|

In the same vein, Coinbase may eat into OpenSea’s NFT dominance, and Near/Tron may eat into Luna/UST’s stablecoin dominance. Ultimately, the interest in competition proves that there is something worth competing over. Smart contract platforms, NFTs, and stablecoins are easily three of the most successful use cases of blockchain technology to date. The competition to build the best versions increases overall adoption. A rising tide lifts all boats.

So while the market tries to decide who will win, thematically, it’s almost a sure thing that NFTs and algorithmic stablecoins will succeed, with multiple winners and a huge, growing pie.

For more background on both topics, I enjoyed Galaxy Digital’s take this week:

Coinbase Debuts NFT Market Place

After months of anticipation, Coinbase released a beta version of its NFT marketplace on Wednesday. While only a select group of users can transact NFTs on the platform today, any visitor can still browse individual NFTs, NFT collections, and user profiles. The mere release of this platform, even in its limited functional state, is a milestone in and of itself, given the 4+ million people who signed up for its waitlist (compared to 1.5 million all-time users of OpenSea, according to Dune Analytics). Coinbase built this OpenSea challenger with an eye toward integrating its existing retail-oriented product suite as much as possible. Not surprisingly, Coinbase Wallet features as the de-facto gateway to this web3 application (though Coinbase NFT is also compatible with other wallets like MetaMask). The platform will only support Ethereum-based NFTs initially, but they have plans of eventually being cross-chain. Fees on the platform are 0% for the time being, and they’re expected to rise to the low single digits seen in other marketplaces (such as OpenSea’s 2.5% and LooksRare’s 2%).

Coinbase wants to stand out from other NFT marketplaces by emphasizing its social features. On the Coinbase NFT platform, users can like, follow, and comment on NFTs and other user profiles. This experience positions Coinbase NFT both as an NFT-oriented version of social media and as an NFT marketplace. Coinbase hopes that this added level of user engagement and interactivity will attract and retain users to its platform. Time will tell if the synergies between Coinbase NFT and Coinbase’s existing retail-heavy products will be insurmountable for current NFT juggernauts like OpenSea to compete against.

GALAXY TAKE: Coinbase is in a very strong position to capture market share from OpenSea and other competitors in the red-hot NFT marketplace landscape. For starters, Coinbase can offer its users a very simplified user journey starting with onboarding fiat all the way to acquiring and NFT. Coinbase can also reduce the number of hoops its users need to jump through to obtain liquidity for their NFTs. Coinbase NFT's approach also simplifies tax compliance for users who may otherwise have to manually reconcile taxable events for their NFT trades should they occur across multiple platforms.

More importantly, Coinbase will enjoy a strong relative position due to its data. There are two angles to this. First, Coinbase NFT will employ a discover page (much like what is seen on other platforms). However, because Coinbase has an existing user base of 89 million individuals, it can leverage this treasure trove of data to recommend more relevant NFTs to its users in their personalized feed. This killer feature of accurate recommender systems anchored by massive datasets for ML algorithms to train on has led to the rapid rise of social media apps like TikTok. Because Coinbase has the best data of all current NFT marketplaces, they have the technical ability to recommend the most relevant content to its users compared to other players in this space.

Additionally, Coinbase NFT’s social features enable brand-new user-generated data sources to help the platform cultivate a custom experience for each of its users. This is especially crucial in a world increasingly cluttered by new NFT projects that emerge daily. Users will appreciate the ability of a platform to filter the signal from the noise. With that being said, integrating social features is a double-edged sword because content moderation is extremely tough, and it is not a core competency of Coinbase’s existing business. To the extent that hate speech, vulgar language, and unpleasant user-user exchanges happen on its platform, Coinbase may struggle to filter out this bad content and may do more harm than good from a UI/UX point-of-view. Time will tell if Coinbase can pull this off, but to the extent that it does, the company will be well-positioned to slice off a chunk of NFT trading market share in this highly competitive space.

TRON to Launch its Own Platform Stablecoin USDD

TRON founder Justin Sun announced plans to launch a decentralized algorithmic native stablecoin on Tron called USDD (Decentralized USD). USDD will employ a market module similar to Terra's UST to maintain its peg to the dollar: USDD will be minted by burning a portion of Tron's native platform token TRX. As demand for USDD increases, burning more TRX will have a diluting effect so that the price of USDD doesn't rise above $1. Similarly, when demand for USDD decreases, USDD can be redeemed for TRX at a 1:1 dollar ratio, reducing USDD supply and putting upward pressure on price whenever USDD is below $1.

TRON DAO is being created to provide custody of reserves backing USDD of up to $10bn in liquid assets (assets not yet specified) to be raised from "initiators of the blockchain industry" for use as an early-stage reserve and to enforce convertibility between USDD-TRX. The TRON DAO Reserve will also set its "basic risk-free interest rate" to 30% per annum. USDD is scheduled to launch on TRON May 5th, and will also be available on Ethereum and BNB Chain through the BTTC cross-chain protocol.

Following the announcement, TRX traded up 17%. Terra's Do Kwon responded to the announcement positively, saying, "Decentralized economies deserve decentralized money - every blockchain will run on [decentralized] stables soon."

GALAXY TAKE: The platform stablecoin wars are starting to heat up. With a design very similar to Terra's UST—including the algorithmic market module, the establishment of a reserve, and a very generous interest rate—TRON becomes the latest blockchain with plans to launch its own native stablecoin. NEAR Protocol is also expected to launch its own native stablecoin, USN, though has not yet made any formal announcement.

TRON currently has the largest balance of Tether across blockchains with a balance of nearly $42bn in TRC20 USDT - above the $40bn of USDT held on Ethereum. Justin Sun is now looking to diversify TRON's reliance on a centralized stablecoin through the launch of USDD, perhaps realizing the importance of having decentralized money, especially with Tether's proven ability to freeze USDT held in specific wallet addresses. Or potentially a greater contributing factor, Sun may be looking to mimic the successful model of Terra's UST in driving user adoption. The fixed 30% rate offered on USDD comes in higher than the 19.5% offered on UST through Anchor, and Sun's wallet was found to have been locking up CVX in Convex, suggesting he may be looking to influence rewards on Curve towards USDD (similar to Terra's 4pool strategy). It's an expensive marketing strategy for a blockchain to drive user adoption, which contrasts with the typical playbook employed by L1s last year of launching large liquidity mining incentive programs.

More competition between platforms for stablecoin dominance is great for users, as it implies higher rewards on stables. Any new chains will have to come in at more generous rates relative to the 19.5% Anchor Rate to incentivize new deposits and make up for the perceived risk premium on top of UST. Also, if TRON DAO or other chains employ a similar reserve strategy to the Luna Foundational Guard, it would suggest increased buying of assets like BTC. There's a strong moral case for decentralized money over the long term. Still, we hope to see more innovation behind any new platform algorithmic stablecoins rather than just copy-and-pasting onto every alternative Layer 1. These stablecoins’ designs have yet to be fully battle-tested, and the risks of de-pegging need to be better understood.

What We’re Reading This Week