Source: TradingView, CNBC, Bloomberg, Messari

Ready To Move On Next Week Post-Election

Of course, this will be a busy week with the U.S. presidential election looming, many critical Senate and House seats up for grabs, and the second-to-last FOMC meeting of the year.

As a result, it’s perhaps not surprising that markets were volatile, and lower last week leading up to this “certain uncertainty”. Equities fell, Treasury yields rose, the VIX spiked, and crypto headed lower. As we’ve stated many times, especially 4 years ago during the last election, markets hate uncertainty more than bad outcomes. So, as the polls and prediction markets moved towards a tighter race, uncertainty increased, and global markets retreated.

On one hand, a repeat of 2020 wouldn’t be so bad for digital assets. After a tough September and a mixed October, markets rejoiced over the Biden victory, even though a Republican victory was largely viewed at the time as a better outcome for investors. Roughly ~50% of voters hated the outcome, but the markets universally loved that the election was over, and business could resume as usual in the U.S.

![]() Source: Bloomberg

Source: Bloomberg

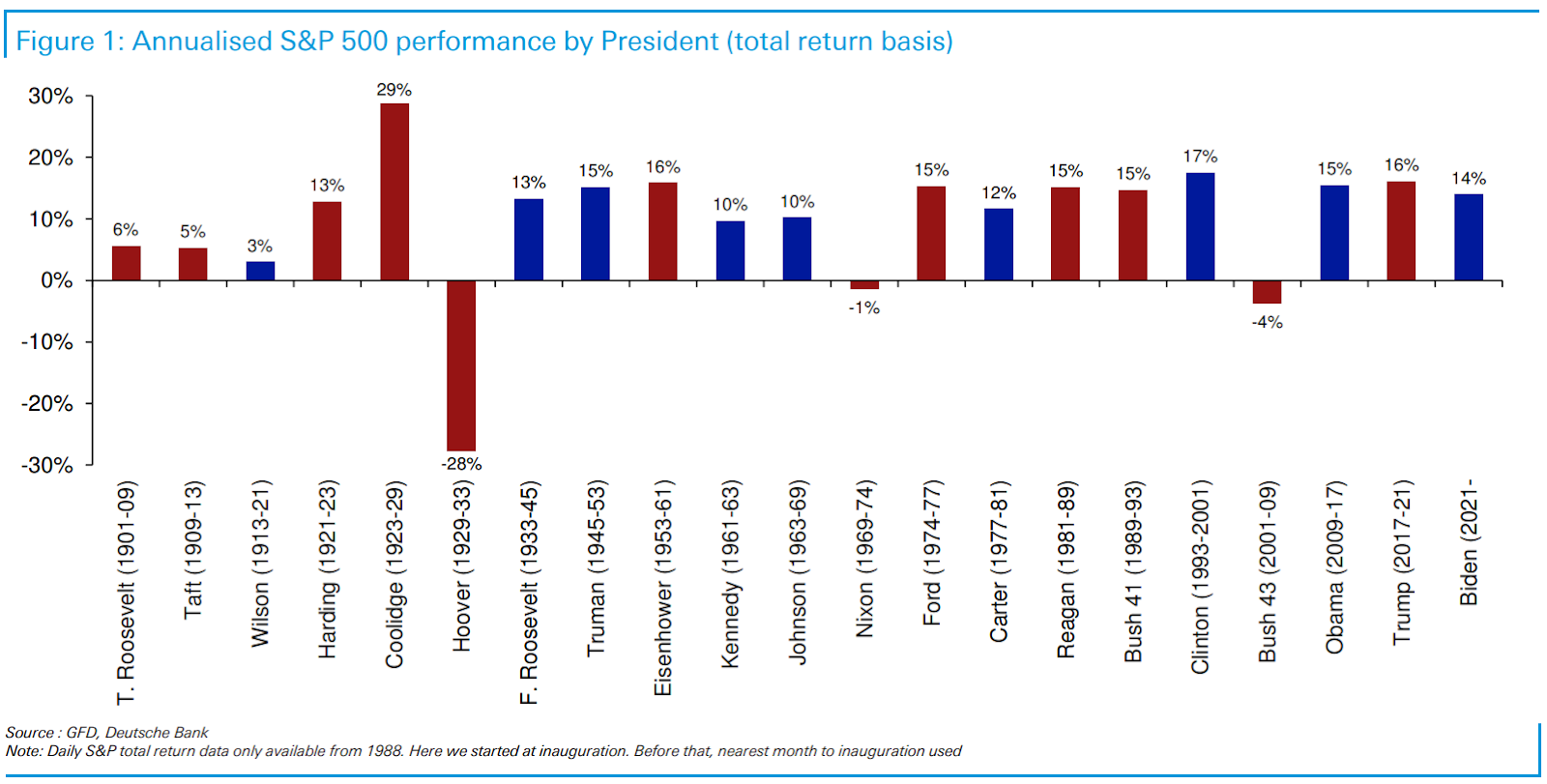

In fact, in the long term, U.S. presidential elections tend to have no bearing on investments. Annualized returns for U.S. equities have had little to no impact from presidential outcomes. The big outliers were driven by events that were arguably mostly outside of the control of the sitting President, namely the Great Depression, the 1973 oil shock, and the double whammy of the post-2000 bubble unwind and the early great financial crash shock of the George W. Bush administration.

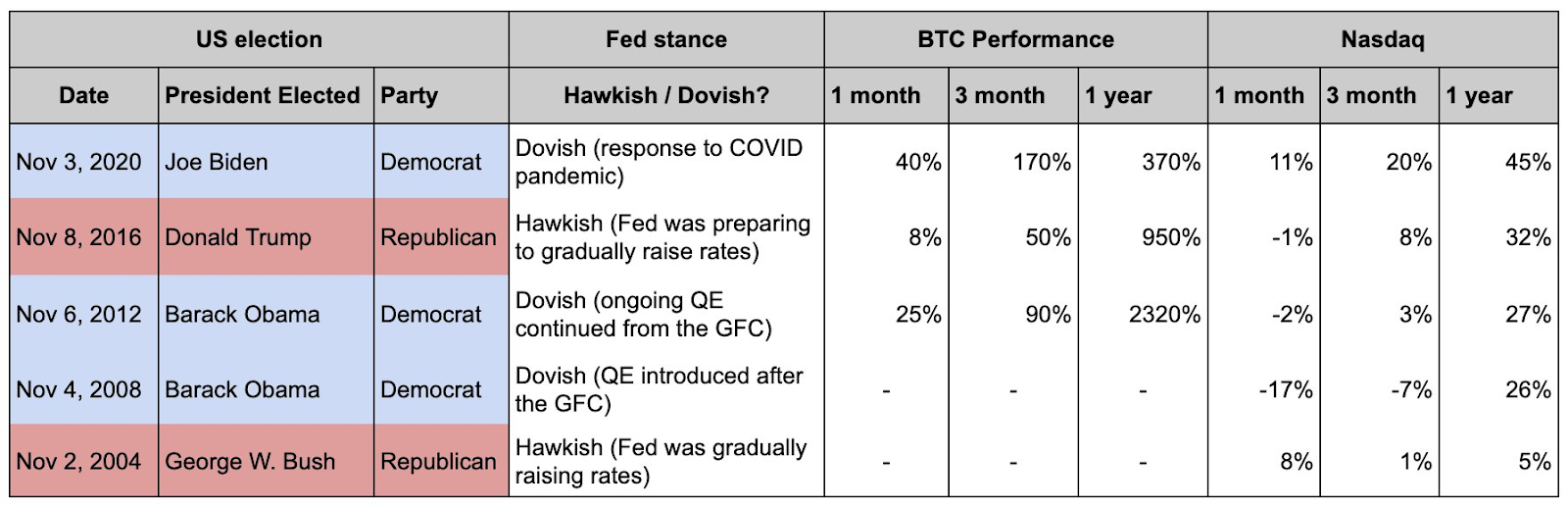

On a much smaller historical scale, buying Bitcoin and holding it post-election works pretty well regardless of the winning party too.

But 2024 has been such a strange year that anchoring to a 2020 or previous election cycle market playbook is a tough order. The S&P 500 is currently

trading higher than all Wall Street forecasts prior to the year. Bitcoin dominates the crypto market, but overall returns for the asset class have been stagnant at best. Gold has hit all-time highs despite little fanfare earlier this year. And U.S. Treasury yields have increased almost 75 basis points following the first rate cut. It’s just been a bizarre year for investing.

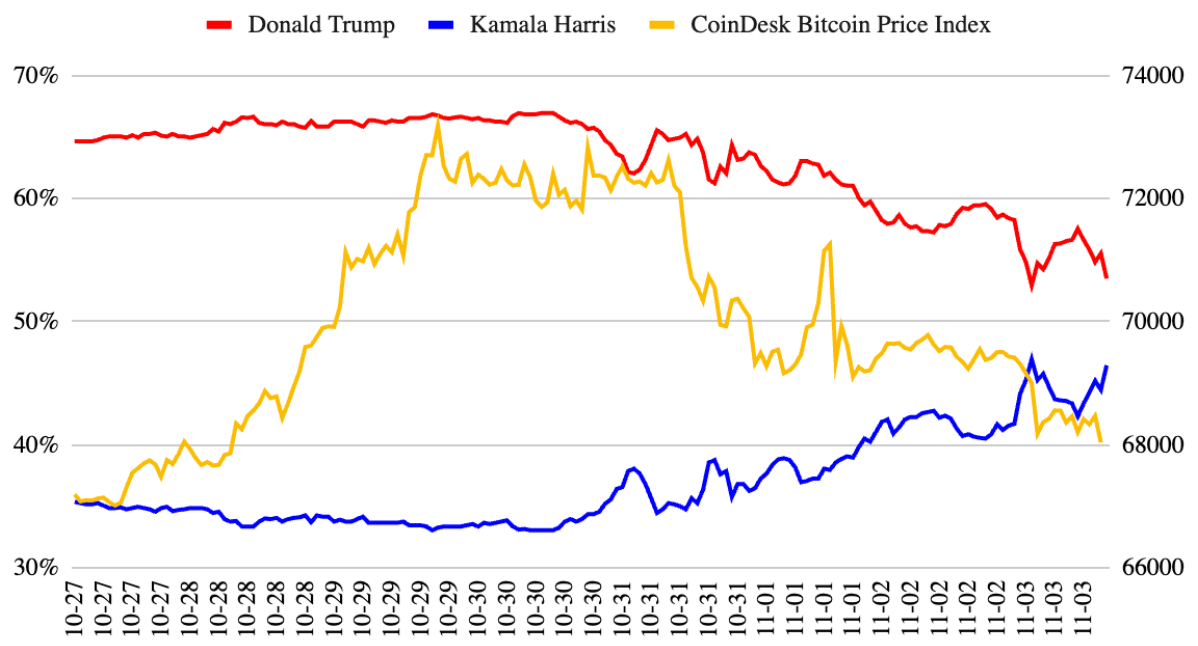

In crypto specifically, the U.S. presidential election has become such a partisan, binary outcome for crypto that Bitcoin has been moving in lock-step with the election odds in recent weeks (moving up when Trump has the lead, and moving down when Harris closes the gap). This is even more bizarre considering Bitcoin stands to gain the least of all digital assets since its regulatory status and ETF access are already in place, whereas L1 protocols, DeFi, stablecoins, and other areas of crypto stand to benefit the most from a Republican victory and a subsequent softer and more proactive regulatory environment. However, Bitcoin is viewed as a proxy for all things crypto, and thus, price action that makes little sense intuitively has become the norm.

Source: Coindesk

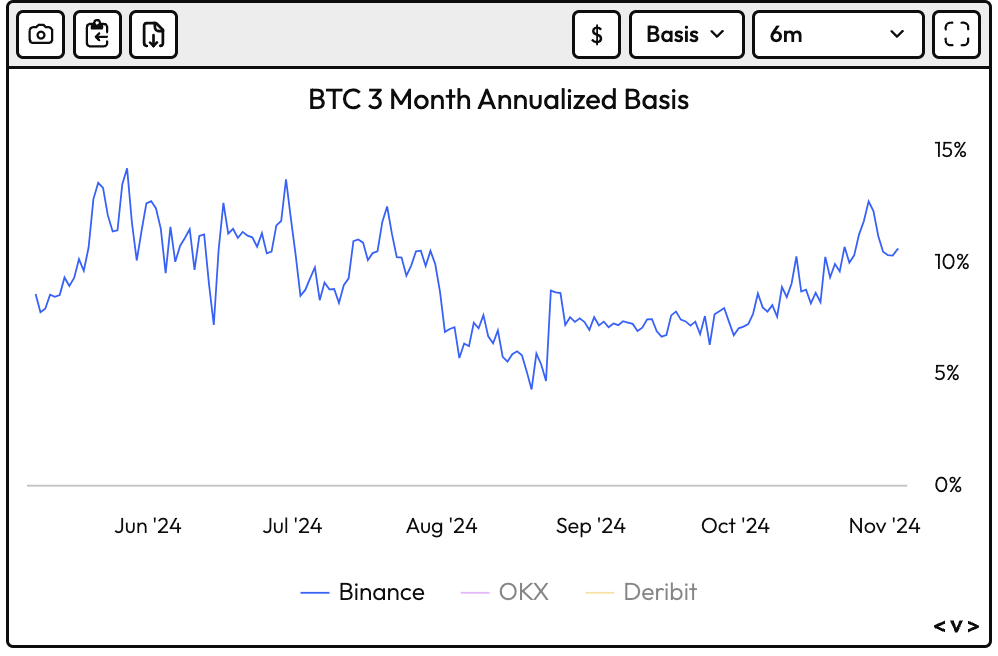

Moreover, as we finally near the election, flows into the spot bitcoin ETFs rose significantly, with U.S. spot bitcoin ETFs bringing in $5.3 billion of inflows in October. With that type of new money, you’d expect Bitcoin to be flying higher, but that, too, has been muddied by the basis trade. As

Jim Bianco at Bianco Research laid out, the inflows into the BTC ETFs might be misleading. He suggests that there hasn’t been new money entering crypto, but rather, a recycling of money that was once on-chain into the off-chain world of ETFs.

While I don’t agree with everything Bianco says, it is indisputable that the 3-month annualized basis (futures price/spot price) looks much more attractive to yield-hungry TradFi funds as it rose back above 10%. This likely contributed to most ETF buying, as hedge funds can sell futures on CME against these ETF longs.

Source: Velo.xyz

The new BTC and ETH ETFs have really sucked the life out of the rest of crypto. While I’m happy for financial advisors and RIAs who can now give their clients BTC or ETH exposure via ETFs, I’m grateful for all of the legal and financial minds who helped force the SEC’s hands to allow the launch of the crypto ETFs, but

let's not kid ourselves. These ETFs are a near-term setback for actual blockchain usage.

The BTC and ETH ETFs just jammed a real-time settlement system (blockchain) into an antiquated T+1 settlement product (the ETF). As an industry, we should strive towards bringing the world’s assets on-chain, not bringing on-chain assets to Wall Street’s outdated rails. Before the ETF hype started in June 2023 (upon the Blackrock application), most blockchain enthusiasts were focused on the benefits of blockchain being a superior technology:

- 24/7 settlement

- Realtime proof of reserves

- 99.999% uptime

- Open APIs

- Low transaction costs

- Public governance

- Global acceptance and usage

But all of this seems to have gone away, at least in the short term, due to the popularity of the ETFs. ETF buyers don’t care about any of this—they just want price action and volatility.

Ultimately, the digital assets market has been held hostage by regulation (or lack thereof), the presidential election, and a limited penetration of Wall Street. So, regardless of this week’s events, the fact that they will soon be over should be enough to renew interest in broader blockchain investing going forward.