Source: TradingView, CNBC, Bloomberg, Messari

J-Pow Opens the Door to Rate Cuts

The market caught fire just a few minutes into Fed Chairman Powell’s annual Jackson Hole speech. Whether he was intentionally dovish or not seems up for debate, but the market was decisive in its interpretation that Powell was giving the green light towards rate cuts. The odds of a Fed rate cut in September had fallen from 96% a week ago to around 70% prior to the speech, following a spike in inflation metrics (particularly wholesale prices), but then shot right back up to 87% post Jackson Hole.

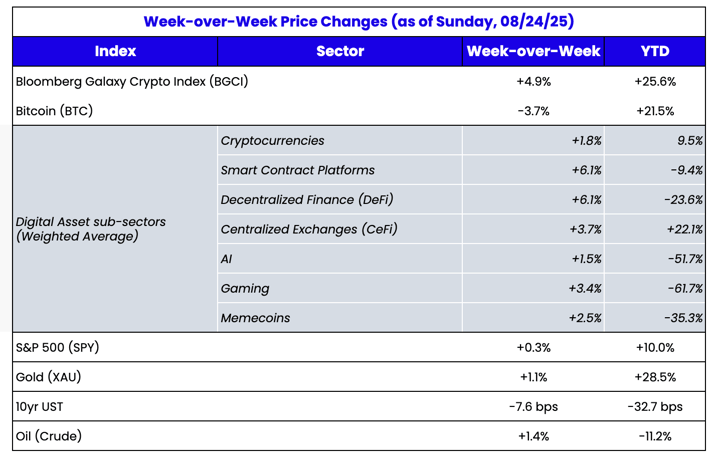

Bitcoin (BTC) actually ended the week lower, and stocks were only modestly higher week-over-week, but that’s only because they had tanked leading up to the speech. The rally on Friday erased all mid-week losses, and in digital assets, ETH and SOL led the way with gains of almost 10% each. ETH-based DeFi also exploded higher, with many tokens rising even more than 10%. Crypto equities jumped too, most notably ETH and SOL-based DATs, though even Circle (CRCL) gained +2.5% on Friday despite being the most negatively impacted by falling front-end rates (~100% of their revenue comes from interest income).

Source: TradingView 5-day chart of BTC, ETH and SOL

Needless to say, those who were shorting the market ahead of J-Pow’s speech were reeling on Friday. Friday generated one of the largest futures short liquidation days of the year in digital assets.

Why were so many people short heading into Jackson Hole? These charts have been making the rounds for the past few weeks, showing that equity valuations (as measured by P/E and P/S) are near the highest on record, and these levels have historically led to corrections. This has led many investors in both stocks and crypto to start “calling the top”.

Source: Bloomberg

Source: Creative Planning

Now, a big correction certainly could happen, but there are also quite a few new factors that weren’t relevant during past periods of market tops. Most notably:

- Democratized access to stocks via Robinhood and other “DIY brokerages” plus a completely unaffordable housing market leading to the death of the “American Dream” means anchoring to historical valuations is a fool’s errand. There is simply too much money chasing stocks. While that doesn’t make stocks less expensive, it does perhaps warrant higher multiples for longer.

- Yes, the market breadth in the S&P 500 is extremely narrow, with the bulk of returns driven by a few tech stocks (Mag 7), and that is a real concentration risk. But profit margins among tech stocks are structurally far higher than the rest of the market, and this margin divergence explains why market leadership is concentrated in a handful of large tech companies. Narrow breadth is not necessarily a sign of an imminent crash, but rather reflects where the earnings power actually resides. In the dot-com bubble, valuations outran reality. Today, earnings are doing the outrunning. It’s hard to call this market a bubble when fundamentals are this strong.

Source: X / Twitter showing Mag 7 earnings growth is much faster than stock price growth

Others are saying that rate cuts shouldn’t happen since stocks, home prices, Bitcoin, Gold, money supply, and global debt are at all-time highs, and inflation is still persistent. That may be true, but it’s clear that the Fed is going to cut rates anyway based on slowing employment, and not the market. So the only question is “are rate cuts actually good for markets”?

Back at the end of 2024, we talked about how historically rate cuts can actually be bad for markets because the Fed was acting too late, and the rate cuts were to fend off a recession/depression. This was the case in 2001 and 2008. But there are also plenty of other cases when rate cuts were done outside of a recession, and these have historically been very bullish for markets (such as 1995, 1998, 2019, and 2024). Ultimately, it comes down to whether or not rate cuts are happening in a recession. If the economy is not headed towards a recession, there is

plenty of data showing that rate cuts are very good for markets.

Source: Goldman Sachs

Which leads us back to digital assets. Just about every data point has been bullish for crypto prices this year, including:

- Regulatory tailwinds

- Stablecoin growth and regulation

- DeFi growth

- Wallet growth

- Real efforts to tokenize stocks, bonds, and real estate and combine trading of securities and tokens into one venue

- Digital asset treasury companies (DATs) soaking up supply

- Record ETF inflows for BTC and ETH ETFs

- Real crypto companies like Hyperliquid and Polymarket becoming mainstream

Those looking for reasons for crypto prices to go down tend to just make the argument that, well, historically prices have gone down after going up. Therefore, we must be nearing a top. There just isn’t a solid argument for this other than if stocks crash and take everything down with it.

But valuations alone don’t make markets crash. There has to be a trigger, whether that is from underlying rates, or debt defaults, or unemployment. Without a trigger, we’re still staring at a very healthy market that is about to get even cheaper when the discount rate is lowered.

And according to a recent Morgan Stanley survey, the percentage of people they surveyed who do not own any crypto has actually increased in 2025 from 69% in 2025 to 82% in 2025, while a recent BofA survey states that 75% of their clients do not hold any crypto.

Source: BofA

That’s a big pile of cash that may or may not enter the crypto market eventually. While prices can always go down, it still seems like the market has a lot of wind behind its back in terms of growth.