What happened this week in the Crypto markets?

Sell Everything

It was a good week for the bears and naysayers, to say the least. Bitcoin fell over 20%, and all major digital assets followed suit, leading to one of the worst weeks in the history of digital assets. This was the fourth consecutive negative week, and the first time this has occurred since July/August 2016 when Bitcoin sold off 16% over a 4-week stretch. A year earlier, another bout of 4 consecutive negative weeks occurred in July/August 2015, with Bitcoin losing 22% over that stretch.

We’ve been here before, and will likely be here again. While many professionals have dedicated their lives to this new industry, and remain as bullish as ever, most of us are not naive. As investments, we understand that digital assets currently trade like penny stocks. That’s scary, that’s frustrating, and that will likely deter many investors. The difference is that there is a path towards maturation, price stability, and usage growth. Many see this path and are willing to wait; others are jumping ship or not interested in getting on the ship. There is no wrong answer other than ignorance.

Worth noting, following the 16% selloff in 2016, Bitcoin finished the following month up +7, and went on to gain 70% over the next 4 months. Similarly, following the 22% selloff in 2015, Bitcoin gained 89% over the next 4 months.

How Do We Get There With Digital Assets?

Have you ever tried going a full day without using Apple, Google, Amazon, or Facebook? It’s nearly impossible (Facebook is fairly easy, but Amazon, Google and Apple are very difficult to avoid). Collectively, these four companies make up 14% of the S&P 500.

Now, remember that 10 years ago you could have easily gone a month without using any of these companies.

Technology, consumer behavior, and adoption curves happen fast, but are difficult to see in the moment. It took a long time for many “value investors” to believe that printing companies were dying, but looking back, it’s obvious. To believe that these four tech companies will have a stranglehold on all internet value creation forever is almost guaranteed to be wrong. Regardless of whether or not digital assets help to replace this value creation remains to be seen, but to dismiss the possibility is foolish. One of the main value drivers of digital assets is the notion of Web 3.0 - the idea that the users of the internet are the ones creating value via the data that tech companies collect, and therefore, the users should capture value instead of the intermediaries (FAANGs). This is a simple, and intuitive concept - and digital assets are the key to its success. But until it actually happens, it seems far-fetched.

Innovation requires patience that many in the digital asset space don’t have. These are the day traders and speculators. But ten years from now, owning digital assets may seem as obvious as shorting printing companies to buy tech companies. Google’s first home page looked like this, and newspapers were still showing up on everyone’s front door -- it was hard to place that bet. But those that can see past the present day are generally rewarded handsomely.

“The Summer of Bitcoin Macro Love is Over”

This summer, near the peak of the digital asset rally, we explored 4 reasons why Digital Assets were rallying, and could continue to rally further:

- The inflows into crypto are real

- Global Markets are in a death spiral (negative rates, negative yielding debt)

- China matters a lot more than the US (Yuan devaluation)

- Awareness is growing

Six months later, it’s worth revisiting the unwinding of some of these themes, and the effects it may have had pushing digital asset prices lower.

Regarding inflows, it’s been mixed. Inflows of talent and financial incumbents has continued at a rapid pace, but inflows of capital have slowed dramatically. This makes sense -- the fast money has fled with prices, but the sticky institutional money has not yet arrived. Institutional capital is generally not swayed by market cycles, but is still in the midst of 18-36 month due diligence processes.

Regarding awareness, I think it’s safe to say that has continued. From Trump, to the G-7, to central banks, to corporations across the globe -- digital assets are top of mind. We see this every day with the 60-90% open rates for our emailed written content.

China and the global markets is where the macro narrative has really shifted since summer. Many of the global macro narratives that we (and others) believed were resulting in allocations to crypto have dissipated ever so slightly. While the long-term trend is still very bullish for digital assets, it’s very possible that digital assets are similar to leveraged equities -- where even the slightest change has an outsized (levered) impact. Our friends at Digital Asset Research addressed #2 and #3 above perfectly in their weekly recap (sign up here), so we invited them to guest post (slightly paraphrased below).

During Bitcoin’s late spring to early summer run from $4,000 to nearly $14,000, we observed a number of narratives in the media attempting to explain the move. Most of these explanations fell into the same bucket – the macroeconomic backdrop was ripe for a non-sovereign backed form of censorship-resistant gold. More specifically, the narratives were bucketed into a couple of categories we want to check in on now that Bitcoin is falling through the $7,000 barrier:

- Exploding balances of negative-yielding debt

- Negative real rates

- Gold correlations

- Chinese Yuan devaluation

Exploding Balances of Negative-Yielding Debt

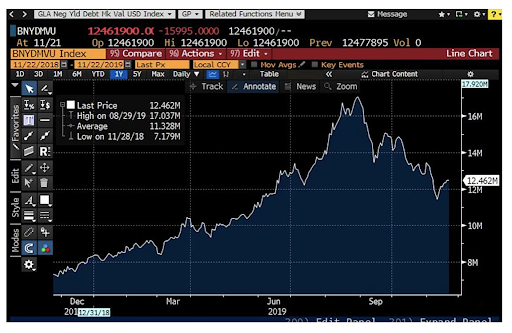

The summer was peak media hype surrounding negative nominal yielding debt balances around the world. This is an abrogation of the typical borrow/lender relationship we’re accustomed to. When nominal yields are negative, the borrower pays back a lesser amount than the loan today. These balances hit $17.9T at the end of August, mostly comprised of sovereign debt issued in Japan and Western Europe.

Today that balance stands at $12.5T, a 30% drop in almost 4 months.

Negative Real Rates

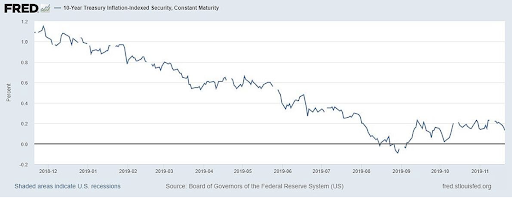

We argued here that it wasn’t nominal yields that investors should focus on but real yields. Real yields are the returns excluding the impact of inflation and should be the hurdle that investors should focus on. Said slightly differently, real yields (returns) are the increases in purchasing one could expect by risking (investing) their money. 10 Year TIPS yields, a good proxy for risk-free real yields, briefly went negative at the end of the summer, coinciding with the peak in negative nominal yielding debt mentioned previously. A good way to think about negative risk-free real yields is that investors must invest their money in increasingly riskier assets, outside of the haven of US Treasuries, in order to maintain the purchasing power of their dollars.

Those trends have reversed, making riskless (or low-risk assets) investments more attractive to maintain or increase purchasing power.

Gold Correlations

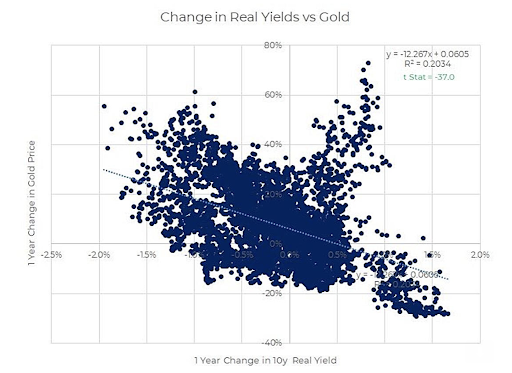

We’ve thoroughly debunked Bitcoin price correlations with the price of gold numerous times – 90-day rolling correlations with gold and Bitcoin peak at about 0.30, which is to say they aren’t highly correlated. But gold prices are significantly explained by changes in real yields, which were dropping all the way until September according to the previous graph.

The reason is that when real rates turn negative, investors should have an increasing appetite to switch their safely invested dollars for non-yielding (or non-productive) assets, like gold, collectibles, art, and Bitcoin. Said differently, when TIPS yields fall below 0%, cash is a non-productive asset as well.

Gold is off about 6% since its early Sept high, not as much as Bitcoin, but still noteworthy in our opinion, especially since it coincides so well with the reversal in real yields.

Chinese Yuan Devaluation

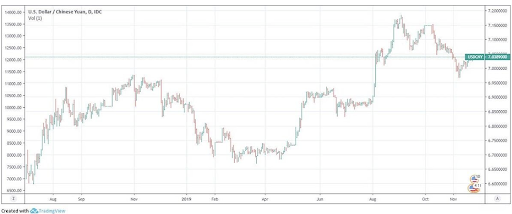

One of the biggest stories from the summer was the Chinese Yuan peg, which broke 7 in the summer amidst the US/China trade dispute and ensuing tariff war. Beginning in May, the Yuan has fallen in value vs the dollar (the Yuan does not freely float), perhaps in China’s attempt to stimulate exports in the face of increased prices caused by US tariffs.

This lead to the narrative that Chinese citizens were buying Bitcoin in order to avoid devaluation. While an interesting story, we found little statistical evidence to support the narrative.

The Yuan has now rallied since the beginning of September, but we hear little of the reverse happening: Chinese citizens selling Bitcoin for Yuan.

What We’re Reading this Week

According to reports last Friday, the People’s Bank of China (PBOC) has reportedly begun to crack down on cryptocurrency trading in Shanghai. The statement was a word of caution to current traders and blockchain businesses to not confuse President Xi’s support of blockchain technology for support of virtual currencies which include “multiple risks”. This report follows news that the Shanghai offices of crypto exchange Binance were raided mid-week (although such reports have also been refuted). Many believe Friday’s market sell-off (which accelerated through the weekend) was a direct result of the PBOC’s stance.

Millennials are set to inherit the largest amount of wealth ($68 trillion) and be the wealthiest generation since the Baby Boomers with disposable income for Millennials expected to hit $7 trillion in the next ten years. However, with the environment the Millennial generation has grown up in (collapse of large financial institutions like Merrill Lynch and scandals like Wells Fargo), this up and coming generation of wealth may not be allocating their capital to traditional equity markets. According to a recent study “forty-three percent of millennial respondents said they trusted cryptocurrency exchanges more than U.S. stock exchanges.” The current sentiment does not imply that the future of investing will all be in digital assets, but sentiment is shifting and legacy financial institutions need to adjust or fade away.

Fidelity’s digital asset arm last week was granted a trust charter from the New York Department of Financial Services (NYDFS) allowing them to engage in virtual currency business with New York residents. This marks an important milestone for Fidelity as its digital asset division can now offer custody and trading of Bitcoin to investors based in New York. We view this as an important step to getting new money in to the digital asset ecosystem.

The R&D division of Visa published a paper last week that outlines a blockchain-based system for collecting user financial data. The system, dubbed LucidiTEE, will tackle how financial data for customers is transmitted and can be used beyond that to train machine learning algorithms on consumer behavior. The system would displace current data aggregators like Plaid and Envestnet and keep data in-house reducing risk of data misuse or leaks.

German airline, Hahn Air, flew customers last week that were holding “blockchain-powered” tickets. The tickets were issued in partnership with Winding Tree, an open-source travel distribution platform. The tickets and flight were part of a test flight to analyze if the process can be incorporated and commercialized for the airline. The platform allows Hahn air to list and manage inventory and manage reservation requests while also accepting major payment forms including cryptocurrency.

And That’s Our Two Satoshis!

Thanks for reading everyone!

Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA - Chief Investment Officer

Katie Talati - Head of Research

Hassan Bassiri, CFA - PM / Analyst

Sasha Fleyshman - Trader

Wes Hansen - Head of Trading & Operations

To learn more or talk to us about investing in digital assets and cryptocurrency

.jpg)