What happened this week in the Crypto markets?

Crypto Markets are Trading Heavy

As equity multiples continue their march towards new all-time highs, crypto multiples contract and continue to trade as heavy as a bag of hammers. Bitcoin’s slow decline is a continuation of themes that have developed since this summer -- volumes are low, no new money is coming into the ecosystem, there is a lack of new digital assets to excite investors, and stocks/bonds/gold are all up double-digits YTD, giving the non-crypto world less reason to focus on this emerging asset class. Bitcoin and other digital assets fell 7% last week, but the downward price action has less to do with negative events and more to do with a lack of positive catalysts. As such, traders are bored, and money is being re-allocated out of BTC into “alt-coins” -- which are bobbing up and down in a zero-sum game, creating no overall value.

That said, we are now inside of 6 months from the “Halving” -- when Bitcoin’s daily mining production will be cut in half. Meanwhile, the Fed continues to do what it does best (print money and lower rates), and citizens in the rest of the world continue to challenge the status quo as it pertains to money, politics and oppression.

Said another way, the positive bull case for Bitcoin remains in tact -- but trying to time it is challenging.

Why Do Crypto Investors Focus So Much on Equities / Recession?

Digital Assets take many shapes and forms, and there are many factors affecting price movements. But Bitcoin is still King when it comes to overall sentiment and inflows, and lately, that sentiment has shifted negative while the exact opposite is happening in Equities.

Why does this matter if Bitcoin has proven to be uncorrelated to equities?

The answer may have to do with Bitcoin’s duality. Many believe Bitcoin is a risk-asset, and as Central Banks around the world push investors and savers into riskier assets, Bitcoin will be the ultimate beneficiary of the stretch for yield. Others believe Bitcoin can be a safe haven, and will protect (and enhance) investors’ purchasing power should a recession occur and/or we see continued destruction of fiat currency valuations. Perhaps both are true. Regardless, despite a near zero correlation, Bitcoin’s success does seem tangentially related to what happens to equity markets.

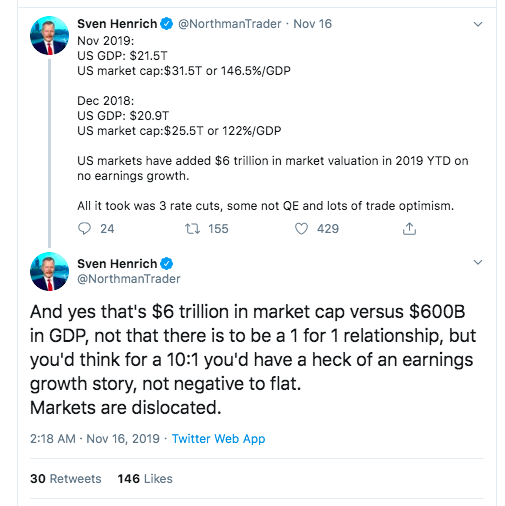

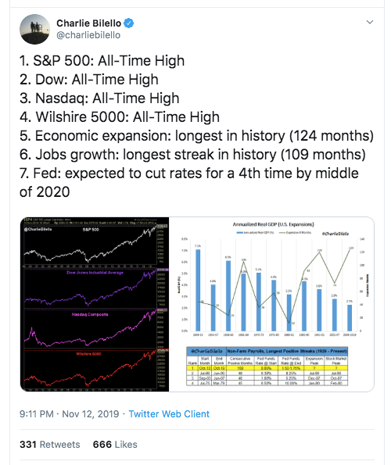

Since Bitcoin was created in 2009, stocks have endured the longest bull market in history aided by debt and low rates. As a result, we have plenty of data to support how Bitcoin will perform in a risk-on, low rate environment (Answer: Bitcoin has had the greatest 10-year run of any asset, ever). However, the jury is still out on what happens during a recession and/or a prolonged slump in equities.

First, let’s set the backdrop for US Equities. Morgan Stanley recently skated around the issues...

Unwavering confidence in a trade deal, Fed easing and the so-called “Trump put” have allowed investors to shrug off weakness in global trade, capital spending, manufacturing, corporate earnings, business confidence and recession signals such as the inverted yield curve. Bulls note strength in services and the US consumer, but now these pillars don’t look so sturdy either. Deterioration in manufacturing seems to be spreading to services, consumer confidence is flagging and labor market vulnerability is emerging. The odds of recession are unequivocally rising. A recession need not be severe or punishing for stocks, but expectations need to reset and risk premiums expand. Escaping the cyclical bear market requires one last capitulation on earnings and valuations. Stay patient and defensive.

… while Cantor Fitzgerald was much more pointed:

The wonderful thing about sports is that there’s a score and nobody can craft a narrative that the winner is a loser. The score is the score. Liverpool’s win over Man City this weekend is indisputable. In markets, however, narratives are everything. There is no one, decisive metric – no single score. The WSJ discussed the rapid expansion in term premium noting that “the yield curve, in fact, completely uninverted this week for the first time since November 2018, meaning shorter-dated benchmark Treasurys [sic] all yielded less than longer-dated ones.” The Journal’s author further suggested that “the reversal gives comfort to investors, because an inverted yield curve has proved to be one of financial markets’ best predictors of recessions.” O contraire! This un-inversion is precisely what one might expect preceding a recession. We must ask why the curve normalized and how that relates to recessions. To the first question, the answer is that most of the curve’s steepening has come from the Fed cutting three times! Historically, this kind of late cycle cut after a deep inversion (as the curve just experienced) is indeed followed by recession. We wrote on July 11th that “a look at history should be creating considerably more dissonance for market participants than it is right now. Late cycle cuts, no matter how masterful any Fed maestro might be, tend to be followed by recession within several months. Risk assets tend not to perform well during such periods.” So, our conclusion would be that the rapid expansion in term premium is precisely what should give market participants even more concern – not less.

There are two main takeaways from these snippets:

- Multiple expansion seems to be the only way stocks can continue to go higher

- Narrative trump reality

Given this backdrop, it’s not surprising that crypto investors are creating the narrative now about what will happen to Bitcoin in a recession. After 10 years of infinite growth in crypto prices paralleled by infinite growth in stock prices, we’re inevitably going to have to test the waters the other way at some point... and maybe quite soon. Crypto investors are doing their best to get ahead of this narrative before it happens.

And so, the narrative builds:

- We’re heading towards a recession

- Bitcoin will do well in a recession

- Stocks are overvalued and Bitcoin is undervalued

The last part of the narrative is the most heavily debated. We know the equity rally has been debt-fueled and due to multiple expansion, but what many don’t know is whether or not crypto markets are declining due to multiple contraction or fundamental decline, because the valuation techniques needed to support multiple expansion/contraction haven’t yet been agreed upon. But this too is changing, as working groups have been created to help create uniform crypto valuations. And any way you slice it with these “work in progress” metrics, it’s becoming quite clear that fundamentals are improving while price is falling.

Thus, equities are getting more expensive at the same time that crypto is getting cheaper.

It may take longer than expected for this narrative to fully play out, and investors across all asset classes are trained to expect the inevitable to never actually materialize. Further, only a small fraction of the investing public is part of this digital asset narrative right now -- for everyone else, this is either brand new or being ignored.

Equity owners with trillions of dollars at stake are hoping this isn’t true. Meanwhile, only a few hundred billion dollars are at stake in crypto hoping this is true. While it’s conceivable that everyone is wrong -- think about the wealth effects if one side is more right than the other.

Notable Movers and Shakers

The oft-volatile waters that price out Bitcoin have become more tranquil of late, with less day to day volatility as Bitcoin finished the week down 6%. While tranquil waters might be a sigh of relief to those weathering the storm, others turned to alternative digital assets for outsized volatility and price movement this week:

- VeChain (VET) had its fourth positive week in a row (+ 33%), with many speculating that the nationwide vaccine tracking system that China is planning to launch in March of 2020 will be powered by VET - a rumor based on a blog post VeChain released in 2018 detailing its Drug and Vaccine Traceability Solution. On Thursday, VeChain announced a Tea Tracability Platform that is being officially endorsed by the Chinese government - another feather in the cap for the self touted ‘enterprise-focused blockchain ecosystem’ in their efforts to permeate the supply chain management sector of the Chinese economy.

- Basic Attention Token (BAT) announced on Wednesday that Brave, the web browser built to natively support and work with the BAT token in the ad-exchange ecosystem, has officially launched Brave 1.0. The 8.7 million monthly active users on their beta now have access to the full set of features offered in this release: Brave Rewards (payments), Brave Ads (monetized attention), and Brave Shields (ad/tracker blocking). Investors reacted positively to this significant release, as BAT finished the week up 13%.

What We’re Reading this Week

Digital assets have become mainstream as evidenced by the two pages (out of 46) dedicated to them in the Federal Reserve’s semi-annual report on financial stability. The report unfortunately had a cautionary tone, warning that the proliferation of stablecoins could cause global instability. The concern surrounds the possibility of a bank run on issuers of stablecoins stemming from liquidity, operations or credit. While the report makes some points to be concerned about we view this as a net positive for the industry.

According to reports from publication The Logic last week, Canada’s largest bank, Royal Bank of Canada, is exploring a cryptocurrency trading platform. RBC recently filed four patents in the US and Canada that indicate how the bank might integrate cryptocurrencies. The findings along with 27 other previously filed patents related to blockchain indicate RBC is well on its way to offering its customers cryptocurrency accounts.

In a press release last week, HSBC announced it was exploring Distributed Ledger Technology (DLT), with participation from Temasek and the Singapore Exchange. The purpose is to determine if DLT can be used to issue and service fixed income securities. Their ultimate goal is to digitize the entire Asian bond market by reducing friction and lowering costs. These groups join a number of other financial institutions exploring DLT for such use cases.

According to a story from the Wall Street Journal, two ICO issuers - Airfox and Paragon - missed their deadlines last month to repay investors after the SEC ordered them to refund investor capital or register their tokens as securities. A third company is purportedly five months late to provide investors information to judge if a refund should be sought. These companies were given a reduced fine by the SEC after promising to abide by fundraising regulations set out by the SEC. It is unknown at this point if Airfox and Paragon have enough assets to repay investors and if they will therefore be able to comply with the SEC settlements.

And That’s Our Two Satoshis!

Thanks for reading everyone!

Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA - Chief Investment Officer

Katie Talati - Head of Research

Hassan Bassiri, CFA - PM / Analyst

Sasha Fleyshman - Trader

Wes Hansen - Head of Trading & Operations

To learn more or talk to us about investing in digital assets and cryptocurrency

.jpg)