What happened this week in the Digital Assets markets?

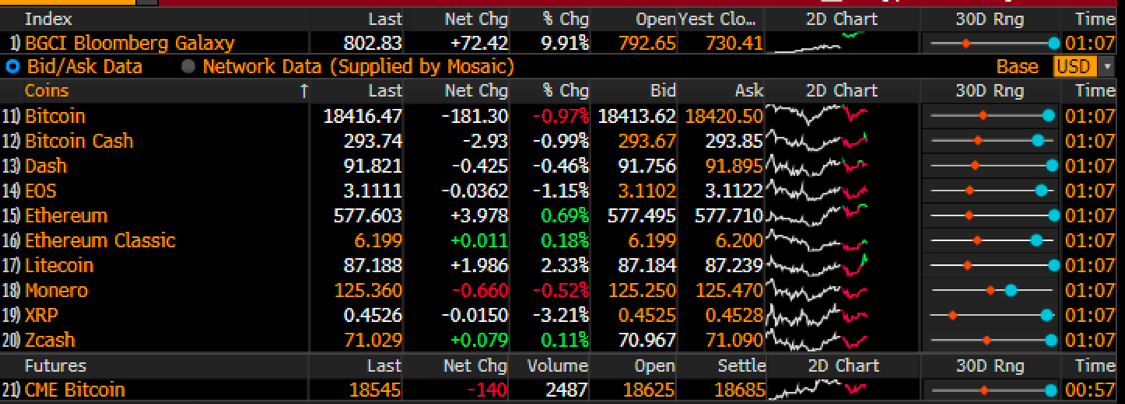

What happened this week in the Digital Assets markets?Week-over-Week Price Changes (as of Sunday, 11/22/20)

|

|

WoW

|

YTD

|

|

Bitcoin

|

+14.8%

|

+153%

|

|

Bloomberg Galaxy Crypto Index

|

+24%

|

+182%

|

|

S&P 500

|

-0.8%

|

+10%

|

|

Gold (XAU)

|

-0.8%

|

+24%

|

|

Oil (Brent)

|

+5.7%

|

-30%

|

Source: TradingView, CNBC, Bloomberg

The Market is Ripping, and No One Will Stop Talking About It

If you’re reading this, chances are you already know that digital assets were on fire again last week, which continued in force throughout the weekend. Unlike the past few months, where each move higher in certain sub-sectors of digital assets stemmed from some rational qualitative source, this past week seemed more like blind panic buying, and the front-running of possible continued panic buying. Regardless of merit, this is what it looks like when small asset classes begin to go mainstream - the sheer lack of supply is on full display.

- Bitcoin was higher (+15%)

- Ethereum was higher (+29%)

- DeFi was higher (+16%)

- Small-caps were higher (various)

- Forgotten tokens from 2017’s graveyard were higher (XRP +58%, XLM +28%, EOS +20%)

We’re at the stage of the rally where all of us who are heavily involved in digital assets are getting bombarded with phone calls and texts, and those that crave attention can’t stop making wild price predictions on CNBC and Bloomberg. There appears to be two types of investors right now:

- Those that are heavily invested are celebrating, perhaps exorbitantly, as they feel long-awaited validation.

- Those who are not invested continue to publicly deny this market’s existence, and are finding new ways to justify their lack of involvement, some going as far as calling it fraudulent.

If this sounds familiar, it’s exactly what just happened following our Presidential election, and it’s not exactly healthy. This religious-like belief in one’s preconceived notions makes it difficult to accept new information, which is why it is so important to see folks like Ray Dalio of Bridgewater and Rick Rieder of Blackrock, amongst others, begin to slowly change their tune on Bitcoin. It’s also why those of us who invest beyond “cryptocurrencies” into the world of digital assets issued by real value-producing companies and projects are so excited -- because we’re about 2 years away from the rest of the world waking up to these assets as well.

However, we still have a long way to go. Every Bitcoin or Ethereum breakthrough comes with endless speculation about nonsense that should have died years ago, but remains stubbornly in the public eye. The thing about religious-like opinions is that they don’t easily die, even when it seems obvious to others that it should.

For example, here’s a look at the CRYP page on Bloomberg. While it’s nice to see Bloomberg embracing this portion of the financial markets so traditional financial investors can begin their educational journey, outside of Bitcoin and Ethereum (and reluctantly Zcash), not one of these other tokens would ever be seriously considered by research-minded digital asset investors. Bitcoin is digital money, Ethereum is like the Apple app store, in that almost every blockchain application is built on top of it, but the rest are longshot “show me” stories from the 2017 VC investing class. I’d love to see an investment memo explaining investments in any of the others -- my guess is they don’t exist since these tokens exist purely because algos/quants/retail traders keep them alive. I for one have been investing in this space professionally for 3+ years now and I have no idea what Dash does, or is supposed to become. Yet the casual investor will likely stumble upon Dash before hundreds of other digital assets that do have a real purpose and value.

Our opinions aside (which like Rieder and Dalio above, we reserve the right to change our mind), as an industry we still have not gotten to a point where the best and most relevant information is accessible to all investors. Market fragmentation and misinformation create a lot of alpha for a small group of investors, but also severely hinders the speed of growth and adoption.

As an industry, we can do better.

Even a 10-year old understands why all companies will eventually have a token

Arca’s head of Investor Relations, Peter Hans, had an interesting conversation with his 10-year old daughter this weekend:

Peter: “The first stock I ever bought was Southwest Airlines (LUV) in 1993.”

Lucy: “When you buy stock in Southwest Airlines you, do you get a free ticket?”

Peter: “No, but that is a really good idea.”

Lucy: “ I feel like you should at least get a 10% discount on tickets or something.”

That innocent conversation explains years of divergence between the 1% and the 99%. According to Gallup, “ just a modest majority of Americans, some 55%, own stocks”. Despite our entire economy being driven by consumers, very few actually benefit financially from their own consumption.

This conversation does, however, perfectly explain what has been happening in digital assets over the past two years, and why several companies who have issued tokens to their customers have grown faster than any other companies in history. Some companies are issuing digital assets specifically to wedge that gap between those who benefit financially (shareholders) and those who benefit via utility (customers) - a dynamic that makes even more sense if viewed through the differences between Amazon shareholders and Amazon Prime members. We refer to these hybrid tokens as “pass-thru” tokens, as they represent a hybrid security that is part loyalty / reward program to be used within a closed ecosystem, and part quasi-equity ownership via financial value that is passed through directly to tokenholders. This type of arrangement leads to customer evangelism and rapid growth, as early customers are incentivized financially to help their favorite companies grow.

It should come as no surprise then that some of the best performing tokens and fastest growing companies over the past several years are those with tokens issued by actual companies, not decentralized protocols. These companies have given financial rewards to their customers via pass-thru tokens. A few examples can be seen below:

- Binance’s BNB token: +1500% (from $2 to $30)

- Hxro’s HXRO token: +1000% (from $0.02 to $0.20)

- Celsius’ CEL token: +6200% (from $0.04 to $2.50)

- Helium’s HNT token: +800% (from $0.20 to $1.60)

Further, in the wake of economic destruction of small businesses around the world due to the pandemic, it’s both embarrassing and extremely disheartening that more companies haven’t embraced this financial innovation yet. There is a way out of this endless loop:

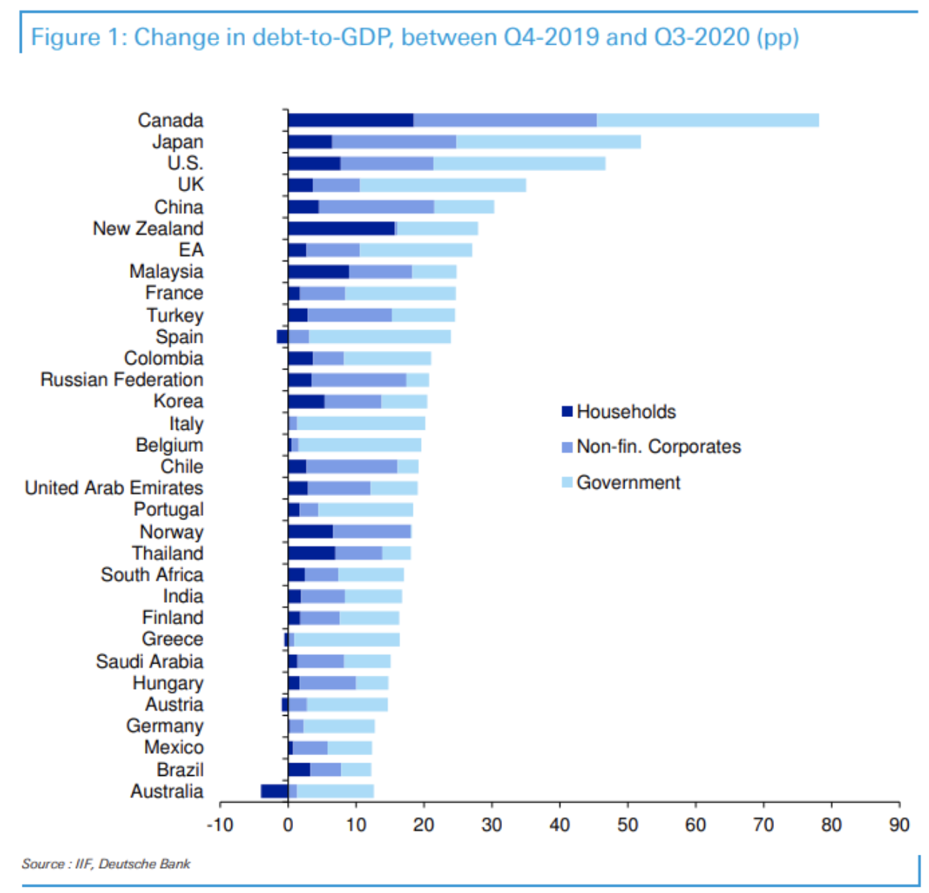

Between a lack of investment bankers, and a lack of education, most companies don’t even know this type of capital raising and growth hacking instrument even exists. Instead, we continue to layer on debt that will never be repaid. According to Deutsche Bank:

“The cost of the pandemic will only be truly known in years to come but we can get some good early indications by looking at debt increases around the world. Yesterday the IIF suggested that global debt will hit $277 trillion by the end of 2020, up around $20 trillion over the year (just shy of the annual size of the US economy). Excluding financial debt (where there is double counting risk), global debt/GDP will go up by 35 percentage points in 2020. It’s hard to believe there’s been a bigger global increase in history.”

Source: Deutsche Bank

Source: Deutsche Bank

This is just outright irresponsible. We are sitting on a new form of capital formation that consumers actually want, which fuels growth, and does not create a liability, yet the regulators are dragging their feet while the majority of companies don’t even know this is an option. Meanwhile, investment banks are trying to figure out how to cover Bitcoin from a research perspective, a service absolutely no one needs. We’ve received four calls in the past month from investment banks asking us to help them map out the “publicly tradable universe”, but instead of embracing tokens issued by small companies and doing their jobs as investment bankers to create more investable products, they are scrambling to write research on “Bitcoin tracking stocks” like Galaxy Digital, Hut 8, Microstrategy and of course the upcoming Coinbase IPO. The same bankers and broker-dealers that blockchain aims to disrupt would rather write research no one needs in an effort to get a piece of the trading fees they are missing out on rather than try to avoid disruption by getting ahead of the inevitable shift in capital formation and investing.

As an industry, we can do better.

What’s Driving Token Prices?

By Sasha Fleyshman, Trader

The Bitcoin Blitzkrieg over the last seven weeks took a moment to allow the rest of the market to catch up, with Bitcoin dominance falling 1% (albeit during a positive week for all digital assets). The market itself has been driven by rampant spot bidding and a rapidly increasing funding rate (+50bps to +70bps daily across the sector, which means those owning long perpetual futures contracts are paying to stay long), as well as a supposed Grayscale/PayPal bid that is soaking up supply faster than it comes to market. With the holidays around the corner, we are left remembering the past moves around Thanksgiving (+175% in 2017, -50% in 2018, -25% in 2019). This week, we focus on the drivers of this market - Bitcoin and Ethereum:

- Bitcoin hash rate is recovering nicely three weeks after the second largest difficulty drop was recorded, adjusting down 16% (largest was 18% in 2011). Difficulty is a target that helps maintain homeostasis to keep the Bitcoin blocks at 10 minute intervals; it rises when there is more hash rate in the network, and falls when there is less. As such, the expected difficulty adjustment in five days is projected at +8.5%, which is 5% off the previous highest rate. Network difficulty bouncing back is a positive sign, as it is positively correlated to the security of the network. In a market dominated by volatile price movements and aggressive predictions, a quick look under the metaphorical Bitcoin “hood” shows that the engine is running just fine.

- Ethereum is in the process of transitioning from the Proof-of-Work (PoW) consensus mechanism to the Proof-of-Stake (PoS) consensus mechanism. The way PoW works (Bitcoin is PoW) is that a significant but feasible amount of effort is required from validators of information to deter malicious activities such as spam or double-spend attacks (those that provide this effort for Bitcoin get rewarded with newly minted supply, i.e. miners). Moving to PoS removes this from the system, instead using active participants (validators) to propose, verify, and vouch for the validity of blocks (by doing so, they are rewarded with newly minted supply). The difference between these two is that with PoW your costs are in equipment, electricity, and upkeep - in PoS your main cost is that you need to post assets as collateral to ensure alignment in behavior between the validator and the network. Currently, 58% of the required ETH has been staked to trigger the launch of the mainnet, with a soft launch date of December 1st (unlikely at this point due to time constraints).

And That’s Our Two Satoshis!

Thanks for reading everyone!

Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA - Chief Investment Officer

Katie Talati - Head of Research

Hassan Bassiri, CFA - PM / Analyst

Sasha Fleyshman - Trader

Wes Hansen - Head of Trading & Operations

Alex Woodward- Analyst

To learn more or talk to us about investing in digital assets and cryptocurrency