What happened this week in the Digital Assets markets?

What happened this week in the Digital Assets markets?Week-over-Week Price Changes (as of Sunday, 11/29/20)

|

|

WoW

|

YTD

|

|

Bitcoin

|

+0.9%

|

+152%

|

|

Bloomberg Galaxy Crypto Index

|

+7.8%

|

+204%

|

|

S&P 500

|

+2.3%

|

+12.6%

|

|

Gold (XAU)

|

-26%

|

+19.4%

|

|

Oil (Brent)

|

+7.0%

|

-25.7%

|

Source: TradingView, CNBC, Bloomberg

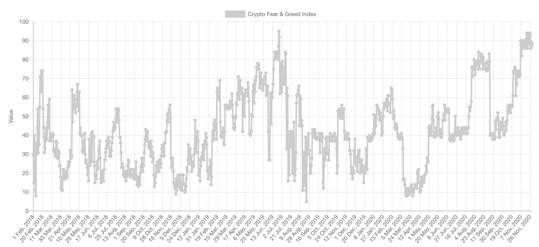

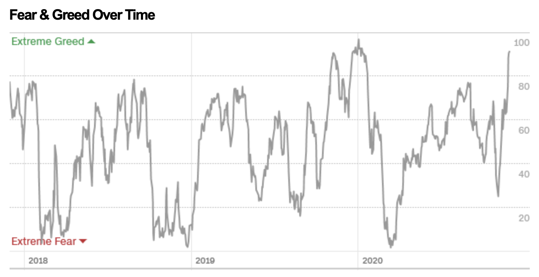

Market Participants Showing No Fear

Stocks up. Digital assets Up. Oil up. It doesn’t seem to matter what you’re invested in right now… chances are, it’s higher. And as we said last week, the bulls and bears are equally loud and insufferable right now, as the chorus of celebrators grows louder as does the uninformed anti-Bitcoin takes. But while the bears are talking loudly, they aren’t doing much investing. Everywhere you look, markets look extended, with very little fear.

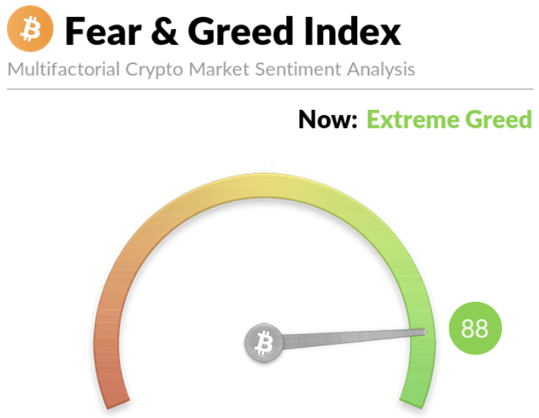

Both the equity and Bitcoin fear and greed indexes are flashing caution.

| Bitcoin Index |

Stock and Corporate Box Index |

|

|

|

|

|

|

|

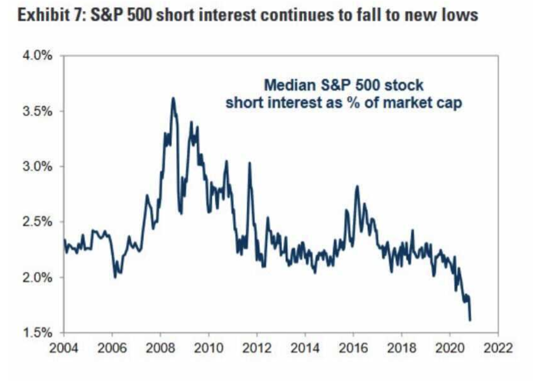

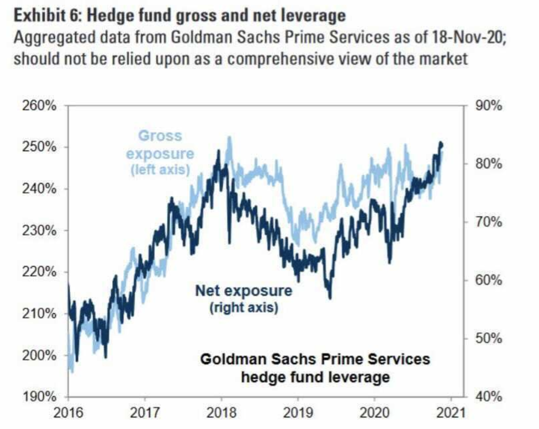

Equity short interest is at 15-year lows, and hedge fund leverage is at 5-year highs

Source: Goldman Sachs Report

At one point last week, Bitcoin and Ethereum skew was -28% (meaning call options were 28% more expensive than puts). We could go on and on. While the lack of fear itself should be causing more fear, the reality is, governments around the world are basically double-dog daring investors to hold cash. They are doing everything in their power to force investors into risky assets, and it’s working. They’re also constantly changing their narratives, which on its surface would be concerning, except it's nearly impossible to take any government officials' words at face value anyway after 10+ years of moral hazard.

When everyone is on one side of the boat, it usually ends badly. But at the same time, the government is doing a pretty effective balancing act on the other side.

The Institutions are Coming, the Institutions are Coming!

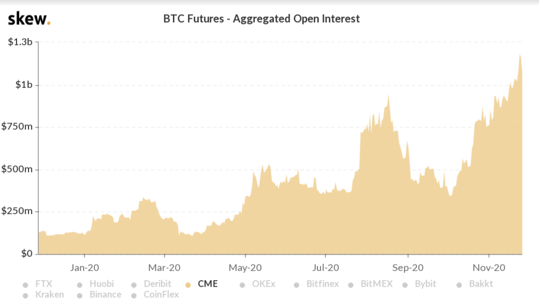

The biggest, most frequently stated hypothetical scenario in digital assets is now a reality. The institutions are in fact coming, many of whom are already here. Coinbase wrote this week, “Institutional adoption is flashing green”, citing two benchmarks for tracking this adoption:

“CME Bitcoin futures open interest made a new all-time high above $1bln in dollar notional. Assets under management of the Grayscale Bitcoin Trust crossed $10bln for the first time. “

Source: Coinbase blog via Skew

Coindesk went further, stating, “While we have been hearing for years now about the fabled institutional “wall of money” poised to rush in and push BTC prices to stratospheric levels, there are some signs that institutional interest is growing.”

Everywhere you look, there are new data points and discussions about new entrants. There’s only one problem.

Ummm… How Do you Trade Unregulated 24/7 Assets on Regulated, Limited Trading Venues?

Grayscale’s products and the CME futures products are dominating US institutional trading of Bitcoin. The problem is, they both run on outdated infrastructure that don’t support the 24/7 nature of trading Bitcoin. And this of course completely ignores the hundreds of other unique and growing digital assets that aren’t even available on the CME or at Grayscale, yet these other assets often provide insights into the behavior of Bitcoin and Ethereum. The institutions are coming all right, but they are currently playing stickball in the parking lot while the pros are under the lights of Yankee Stadium. This of course is not an endorsement of unregulated exchanges, nor a knock on the CME or Grayscale, but simply a reality of a disjointed market infrastructure. The institutions are getting a raw deal while trying to play by outdated, or unspecified, rules. I’ve personally spoken to two traditional bond and equity fund managers this week who have compliance and back office so far up their assets simply for trying to invest in Bitcoin futures using a “regulated” venue.

How damaging is this limitation? Last week’s holiday-shortened week sheds light on the inefficiencies, which is directly affecting P&L as much as it is settlement and structure. In the first half of the week, Bitcoin rocketed up to $19,374. As soon as US markets closed on the Wednesday night before Thanksgiving, the market turned, with Bitcoin falling over 12% in 16 hours and many other digital assets falling 20-30%. This same pattern reversed over the weekend, as Bitcoin and other digital assets exploded higher ahead of the US open Sunday night. All of this volatility happened with the CME and Grayscale’s products closed for trading. How would you like to watch your P&L move by 15-20% with no ability to do anything about it? This was a reality for all “traditional” institutional investors who are dabbling with products that don’t fully express the market reality.

The graph below shows the price of Bitcoin from Wednesday through Sunday. The yellow lines show when the CME closed on Wednesday, and the white lines the subsequent open. The CME was only open for a brief time period and missed both the move down and subsequent move higher.

Source: TradingView

Source: TradingView

A similar graph below shows an even smaller window of time where Grayscale’s GBTC product was tradable compared with the volatility that occurred outside of trading hours.

Source: TradingView

While bond and equity investors were enjoying time off for the holidays, as were the operators of their favorite trading venues, those of us actually entrenched in the digital assets ecosystem were up until 3am trading (present company included). The institutions are coming all right, but they are taking the local bus while the rest of us are on the express.

The digital assets market needs US institutional investors. We welcome them with open arms. Many of us (again, present company included) are also rooting for regulators to figure this out, and for regulated venues to continue to improve their offerings, thereby stealing market share. We want Bloomberg to offer a suite of services that actually represents this asset class (not the nonsense batch of tokens it currently lists on CRYP). We are keenly aware that the current system is not perfect. This is the early days of a very important and growing asset class. The infrastructure is being built. But until it is fully built, investors have to make tough choices. None of them are wrong, but the differences should be noted and understood.

In the 1800’s, JP Morgan and Alexander Hamilton used to literally corner the market. On an actual street corner. That didn’t invalidate the early days of equity and commodity trading… it simply left more to be desired. That is the current state of digital assets investing.

We can do better, but that doesn’t mean the old way is better.

What’s Driving Token Prices?

By Sasha Fleyshman, Trader

While Turkey Day was tepid historically for Bitcoin, there was still volatility to be had - a 17% drawdown peak to trough is nothing to sneeze at (with much of the space declining 20-30% in tandem). Bitcoin dominance fell 3% this week as high beta outperformed enough in the early week to offset the underperformance into the holiday. This week we focus on two projects that utilized token economics to generate positive interest in their token:

- Yearn Finance (YFI) had quite the week, joining forces with Pickle and Cream in the modern day Food Pyramid M&A. With yield farming being easily replicable and not protected by IP, it makes all the sense in the world for projects to join forces to grow the biggest community and development team (as well as TVL and product suite). MakerDAO raised the YFI vault debt ceiling from 7M DAI to 20M DAI, which bodes well for the velocity sink for tokens deposited into Maker’s protocol. The price action didn’t reflect these moves (unched), with the Thanksgiving selloff erasing the gains from earlier in the week.

- FTX Token (FTT) rolled out staking for their exchange token this week, which should come as no surprise given the success it had with Binance (BNB). Staking the token will offer holders several advantages, such as increased referral bonus rates, better maker rebates, increased voting power, and increased airdrop rewards. The token has been on a slow and steady increase since inception, with this week being no different - FTT finished up 5%.

And That’s Our Two Satoshis!

Thanks for reading everyone!

Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA - Chief Investment Officer

Katie Talati - Head of Research

Hassan Bassiri, CFA - PM / Analyst

Sasha Fleyshman - Trader

Wes Hansen - Head of Trading & Operations

Alex Woodward- Analyst

To learn more or talk to us about investing in digital assets and cryptocurrency