What happened this week in the Crypto markets?

The Crypto Market Is Showing Healthy Signs Again

There has been much more balance in the digital assets market over the past few weeks, aside from September 24th when the whole market fell 20% in a single hour. Each day, some tokens trade up; and some trade down. Even though the overall direction has mostly been lower in past weeks, intra-token correlations have continued to break down, which is a healthy signal. And when it’s rare to see every digital asset move higher or lower together, investors begin to re-enter the market one token at a time.

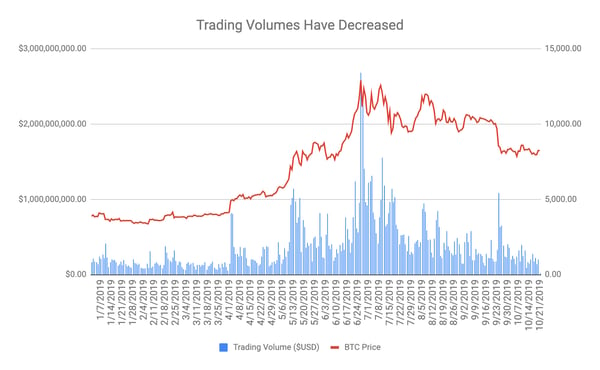

Last week, the overall crypto market was largely unchanged, as measured by both Bitcoin as a proxy as well as numerous Crypto Indices. Bitcoin traded in a narrow range, and the rest of the market followed suit according to their individual betas. But the direction and magnitude of the overall market is less important than the lack of correlation. There was just one day this past week (Wednesday) where the whole market sold off together, and this broad-based selling was driven more by market makers and those that are short pushing the market lower, rather than driven by long unwinds or real-money selling pressure. Again, this is a healthy sign.

Short sellers leaning on the market is typical behavior across all asset classes when volumes are low -- and crypto market volumes remain depressed versus the peaks reached this summer. When volumes are low, shorts are incentivized to keep pushing prices lower until they hit resistance. In the high yield bond market for example, when volumes are low and market makers have little interest in using their balance sheet to stabilize prices, those who are short will continue to bring prices lower and lower until a Blackrock, Oaktree or PIMCO is rumored to step in as buyers -- at which time, shorts will scramble to cover at any price and other long holders will begin to defend prices as well. This generally leads to a gap higher in price as there just isn’t any inventory to sell at these artificially lower levels.

In crypto, we just haven't run into the "Blackrock or PIMCO" type buyer yet (or perhaps these high quality buyers don’t yet exist in crypto). But if/when buyers do start to come back in (and Sunday’s strong price action indicates this may be happening as we speak), the move higher could be just as violent as September’s move lower.

Source: CoinMarket Cap & Arca Proprietary

Crypto Conferences are Ghost TownsLast year, we attended a number of crypto conferences around the country and here in Los Angeles. They were packed with new service providers, issuing companies, asset managers, investors and speculators. Most panels and presentations were standing room only if security would even let more people in. This year, many Arca members have spoken at conferences here in the U.S., and around the world.The crowds are not what they once were. Tumbleweed has replaced many of the sponsor booths. Gone are the ICO projects pitching their “next big thing”; gone are many of the retail investors who thought crypto would make them rich; gone are the loosely financed service providers hoping to sell services to unsuspecting retail clients. Generic interest in crypto is waning. And that may be a good thing. Interest in crypto is largely a lagging indicator based on price; not a leading indicator. As such, it is somewhat refreshing to see the halls of these events empty. Job openings for crypto are at all time highs, and you don’t need a conference to hire, put your head down, and build great products. Similarly, you don’t need retail investors running around every conference looking for the next investing tip, crowding out the institutional investors. This year, we spoke to more allocators of capital than last year -- and that’s not surprising given their due diligence takes much longer, their interest is independent of market cycles, and their capital is much more sticky once they choose to allocate. That said, we did witness one panel where a developer wore baggy pants and sandals, and took his sandal off to scratch his foot during his speech. Needless to say, crypto isn’t for everyone, and we still have a long way to go to institutionalize this space as actions like this turn off even the most liberal investors. But slowly, these crypto rah-rah conferences are being replaced by real financial conferences, like the upcoming Oppenheimer Conference on FinTech, Blockchain & AI: Disruptive Innovation. Lower prices and less retail interest is generally a formula for success for institutional investors looking to enter the space. Bank EarningsJP Morgan, Bank of America and most US banks released record 3Q earnings this week. Of course, the stable business lines like lending are down considerably due to non-existent Net Interest Margin, and the earnings beats were largely driven by more volatile revenue line items like trading. While crypto is often praised for “banking the unbanked”, the opposite may be more likely, as crypto slowly "unbanks the banked". While these earnings reports were impressive, the backbone of banks earnings are driven by lending and interest rates, and a whole slew of products are coming after this business, including decentralized finance projects that utilize digital assets like Ethereum.

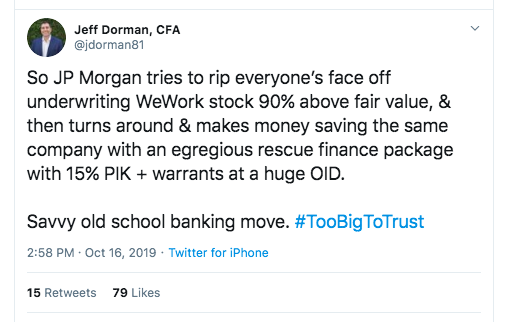

Further, the traditional investment banking businesses may be in trouble as competition grows on this side too. Aside from PR and revenue disasters like the botched WeWork IPO, we’re seeing more direct listings (e.g.. Spotify and Slack) as well as more direct to consumer financings (crypto offerings being just one of these initiatives). In fact, new crypto-focused investment banks like Galaxy Digital are popping up specifically to underwrite and distribute new digital asset offerings (like asset-backed tokens). Galaxy may become the “Jefferies” or “Imperial” of Digital Assets. Jefferies and Imperial can’t compete with the balance sheets of JP Morgan or Goldman Sachs, so they focus on off-the-run, smaller, more winnable deals and esoteric trade opportunities. Similarly, Galaxy can’t launch an IEO of any questionable project and see strong retail demand like Binance and (soon to be) Coinbase, but if they work harder to find good deals from real companies, investors will benefit from these niche offerings.

If this model proves successful, the traditional investment banks will inevitably want a piece of this business, but by then, it may be too late.

For now, these banks will have to make money the old fashioned way:

The Positive Side of Criminal Digital Assets Use CasesDetractors of digital assets like to point to the underground use cases of Bitcoin and other digital assets, primarily as a means of payment for illicit activity. What you don’t hear enough is how terrible digital assets are to use for illegal activities given how trackable these transactions are. Unlike the US Dollar, which is involved in trillions of dollars worth of untraced money laundering, drug trafficking and other illicit activities, Bitcoin is actually quite traceable. Recently, crypto startup Chainalysis, which has raised over $50 million in venture funding, helped the DOJ shutdown one of the largest child pornography websites. IRS Criminal Investigations Chief Don Fort mentioned the importance of the sophisticated tracing of Bitcoin transactions in order to identify the administrator of the website. While the media may focus on the fact that this site was using Bitcoin in the first place, we think it is far more important to see the site shut-down because of Bitcoin. Bad actors are going to act badly, regardless of what tools they have. The WeWork debacle is a microcosm for crypto. One bad deal with ridiculous pricing driven by an investor (SoftBank) that was bigger than everyone else has now cast a shadow over the entire unicorn Silicon Valley tech sector. But just like WeWork shouldn’t invalidate private equity or consumer tech, bad crypto deals and use cases shouldn’t invalidate the whole industry.

Notable Movers and Shakers

Bitcoin (and as a result the rest of the market) salvaged a pretty grueling week of price action with a 3.5% upward move on Sunday, finishing the week relatively neutral (-0.5%). Bitcoin dominance remained flat week-over-week, signaling that the majority of the market moved in lockstep with volumes low across the board. Outliers were modest this week, but are nonetheless worth mentioning:

- Binance Coin (BNB) completed its 9th quarterly burn last Wednesday, eliminating 2,061,888 BNB (~$36.7M) from the market. This is a significant (54%) increase from their 8th quarterly burn (808,888 BNB, ~$23.8M), with revenue streams diversified away from just spot trading, and aided by their recently released products: futures, margin trading, and staking/lending. The team will continue to burn BNB from their allocation until the overall token balance reaches 100,000,000 (currently 185,474,825 BNB outstanding). The token itself didn’t react to the move (+1.5%), but it is worth monitoring as exchange volumes increase in the future.

- Ripple (XRP) released their Q3 quarterly report Friday, revealing that they sold $66.24M worth of XRP last quarter (down from $251.51M in Q2). Ripple has stated that the sale of XRP is programmatic and the funds received from the sale go towards developing the infrastructure and building partnerships to further the XRP network. With their Swell conference coming up in three weeks, compounded with the released report, interest has once again shifted toward the digital asset space’s third largest project, with XRP finishing the week up 6%.

What We’re Reading this Week

What Grayscale’s Q3 Report Says About Bitcoin FlowsAccording to Grayscale’s Q3 2019 report, over a quarter of a billion dollars flowed into their products with the majority of new assets coming from hedge funds and institutional investors. Despite the massive amount of capital flowing in, the majority of capital went to the Bitcoin Trust product with very little flowing into Grayscale’s other crypto products. Also of interest, most investors purchasing into the bitcoin trust used cryptocurrencies, not cash, to invest, indicating that these investors are not in fact new to the space but are recycling their profits back into the space. Grayscale is increasingly expanding its institutional products and last week was approved by FINRA for the first publicly-traded digital currency index fund.The Telegram SagaAbout ten days ago, the SEC issued an emergency order to halt the issuance of Telegram’s GRAM tokens, which were expected to hit the market on October 31 when its network launched. Telegram, a popular messaging app, raised a $1.7b ICO in early 2018 from large VC and institutional investors, promising a network launch by end of October. If the network launch date was not met, Telegram would return ICO proceeds to investors. The SEC’s emergency order claimed that GRAMs were in fact unregistered securities and must be registered in accordance with the Securities Act of 1933. Late last week rumors began to circulate that Telegram was approaching all investors and requesting a 6 month extension on its network launch. Alternatively, investors will only receive 77% of their initial investment back. Crypto Exchange Poloniex Spins Out From CircleLast week, crypto exchange Poloniex announced it would be spinning out from Circle with the backing of a “major investment group”. Circle purchased Poloniex in 2018 for $400m, one of the largest crypto acquisitions at that time. Poloniex will rebrand itself to “Polo Digital Asset” and will no longer serve US customers. The move is not surprising given the increasing regulatory pressure and the increasing competitiveness among crypto exchanges. The terms of the spinoff are unclear, however, the exchange announced it was planning to spend $100m on platform development. Ripple and Coinbase Invest in Mexican Crypto ExchangeMexican crypto exchange Bitso received an undisclosed round of funding led by Ripple with participation from Coinbase, Jump Trading and other notable investors. Bitso began operations in 2014 and currently serves over 750,000 customers. The funding will help Bitso as it expands to other parts of Latin America, primarily Argentina and Brazil. Latin America has become a hotbed for startup innovation in recent years, particularly in the FinTech space as up to 70% of its population is unbanked. In addition, countries such as Argentina and Venezuela have suffered from massive currency devaluations and instability in recent years, making them optimal targets for digital assets.Sacramento Kings to Release Crypto CollectiblesLast week, Sacramento Kings NBA basketball team announced it would be releasing a limited edition line of crypto collectibles. The line is being developed with the help of CryptoKaiju and will include 100 limited-edition Kaiju collectible toys released throughout the 2019-20 basketball season. The collectibles will be represented by a “non-fungible token” (a token that is unique and nonidentical) and 15 of the tokens will also include special experiences such as court side seats or VIP tours. This is not the Kings first foray into crypto: the company recently announced the release of a predictive token-based gaming app and has been accepting Bitcoin as a payment method since 2014.

And That’s Our Two Satoshis!

Thanks for reading everyone!

Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA - Chief Investment Officer

Katie Talati - Head of Research

Hassan Bassiri, CFA - PM / Analyst

Sasha Fleyshman - Trader

Wes Hansen - Head of Trading & Operations

To learn more or talk to us about investing in digital assets and cryptocurrency

.jpg)