What happened this week in the Digital Assets markets?

What happened this week in the Digital Assets markets?Week-over-Week Price Changes (as of Sunday, 8/02/20)

|

|

WoW

|

YTD

|

|

Bitcoin

|

+11.6%

|

+53%

|

|

Bloomberg Galaxy Crypto Index

|

+15.0%

|

+84%

|

|

S&P 500

|

+1.7%

|

+1%

|

|

Gold (XAU)

|

+3.3%

|

+29%

|

|

Oil (Brent)

|

-2.2%

|

-34%

|

Source: TradingView, CNBC, Bloomberg

Ok, That was Surprising

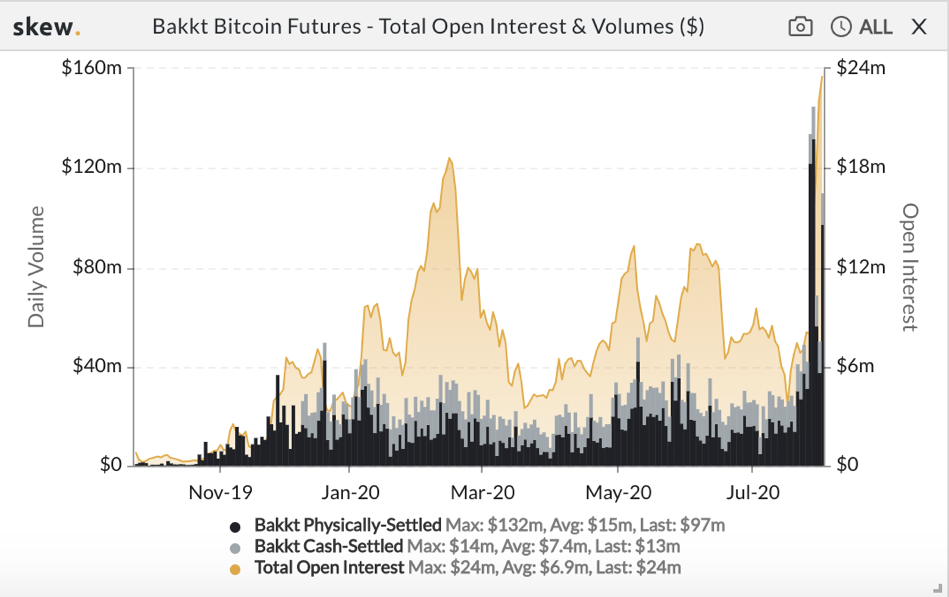

Last week, we discussed a market move that generated no surprises. The same cannot be said of this past week. Bitcoin broke above the symbolic $10,000 level and decided not to stop until a swift rejection of $12,000 over the weekend. Quite a move from the slumbering King of digital assets. During this past week, we saw record volumes across all spot and derivatives platforms. Of particular note, on the institutional side, the once promising but struggling upstart, Bakkt, saw 11,509 contracts traded (85% higher than previous record). Clearly this was not a fluke rally.

Bitcoin started the year as the primary digital asset story, following a March crash to forget, the Bitcoin halving, and validation from investing legend Paul Tudor Jones. But lately, BTC has been forgotten as other forms of digital assets besides “money” have garnered most of this year’s investment gains. As gold, silver, equities, and long-bonds reach record high levels, and the US Dollar slumps, the King of “cryptocurrencies” may be back in the spotlight for the foreseeable future.

Source: Skew

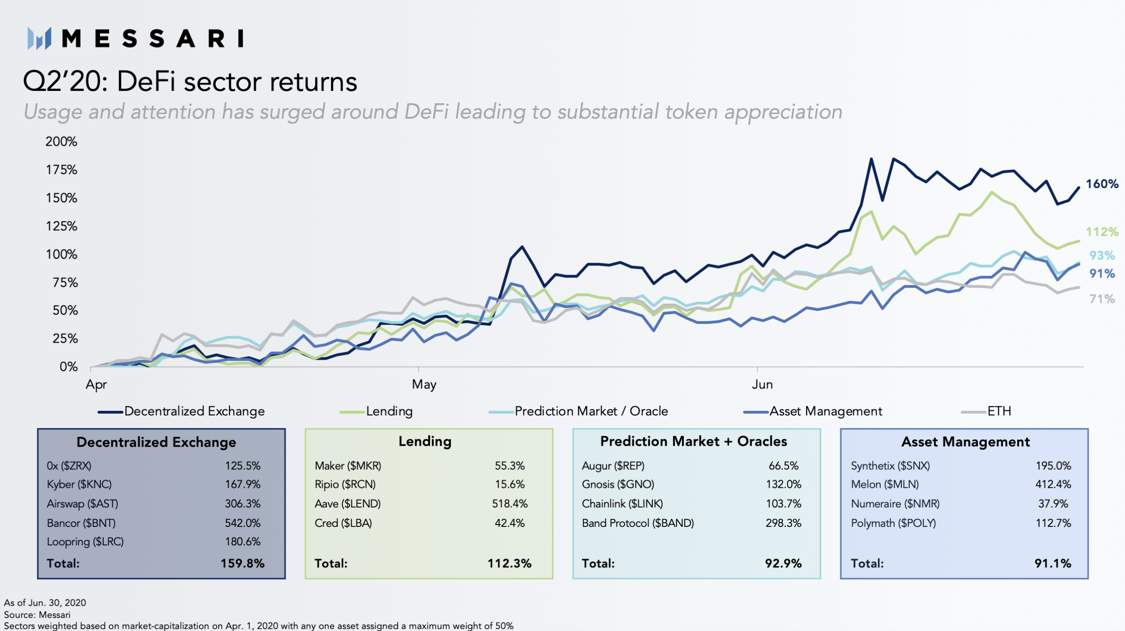

Source: SkewDeFi’s Breakout and Why it Matters: Real Value Accretion and Governance

Written by Arca VP of Portfolio Management: Hassan Bassiri, CFA

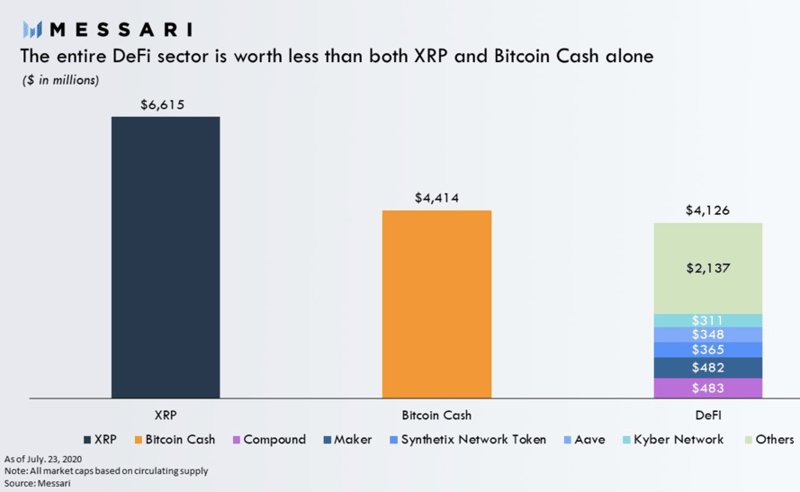

Decentralized Finance (DeFi) has come into its own in 2020 with a total market value of ~$4.1 billion, which still pales in comparison to Layer 1 valuations ($45 billion), and barely registers on the radar relative to the size of traditional centralized financial products (insurance, asset management, and lending platforms). Nonetheless, the 600% YTD growth rate of value locked in DeFi products and subsequent token outperformance can be attributed to two primary factors:

- Real (non-inflationary) yield in the form of exogenous cash flows

- Community Involvement / Governance

The mechanics behind how DeFi applications work can be complex, but the basic premise is quite simple. These platforms turn non-productive assets and investments held on users’ own personal balance sheets into productive assets that can be lent or staked to earn a yield. By rewarding you for using their platform, these platforms bootstrap customer growth faster than normal startups, and once a community of customers develops, they ultimately hand the keys over to their growing communities to make key decisions. Simple in concept, complex in operation. Let’s explore each of these primary factors further using a few examples.

Source: Messari

1. Exogenous Flows Create Value for Token Holder

There have been many iterations of token models and monetary policy. Some are inflationary, some are deflationary, and others are flexible. Compared to a pure inflationary model (which is actually just a tax on non-stakers), DeFi protocols are generating real yield for their users (“DeFi Farmers” or “liquidity miners”) via exogenous “cash flows” coming from other protocols.

For example, Aave is a lending/borrow protocol similar to Compound. When Aave v2 launches, users that stake AAVE tokens in a Balancer pool will effectively become the “equity backstop” for the system in the event of a liquidation shortfall (similar to how MKR holders backstop the stabletoken, DAI). In exchange for assuming this risk, aave stakers will receive:

i) 90% of platform fees (paid in ETH/USDC)

ii) Balancer (BAL) tokens

iii) Balancer pool trading fees (paid in ETH)

iv) AAVE inflationary rewards

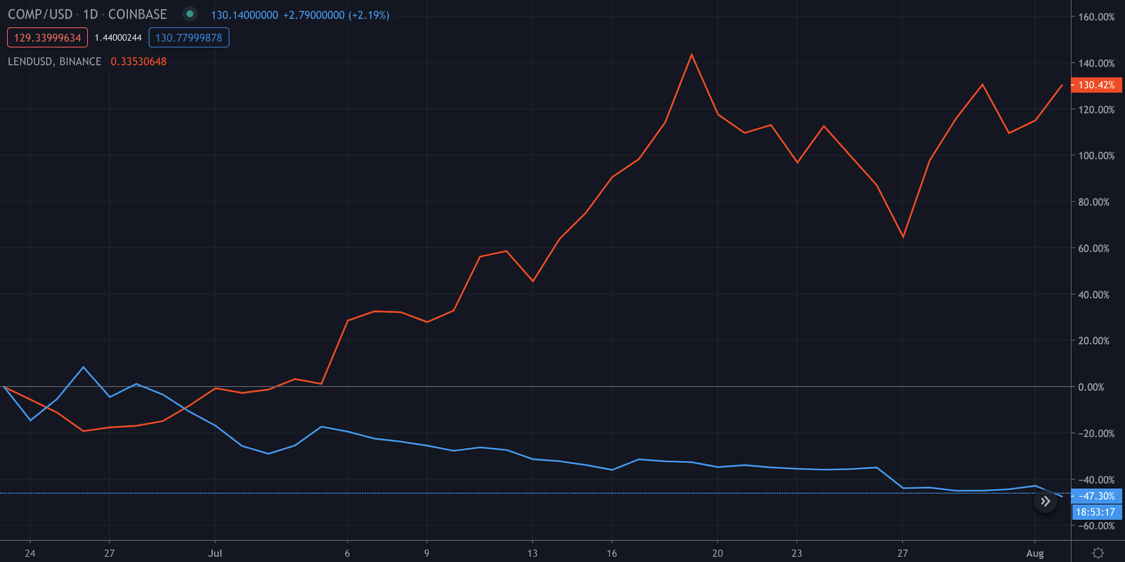

With the exception of iv, all of these represent real yield to AAVE stakers. In AAVE’s model, participants can realize a return selling USDC/BAL/ETH without adding constant selling pressure to the underlying AAVE token, but they also have the option to reinvest/stake those returns in the Aave platform to effectively own a bigger part of the network (thereby entitling them to more future flows). Re-investing exogenous flows not only creates buying pressure for the native token, it acts as a velocity sink (i.e. less circulating tokens), and as more and more tokens are staked, the total value locked (TVL) of the network increases, making the protocol more secure and more visible to other DeFi users and investors). In our view, exogenous cash flows are the key to long-term value accretion for token holders because they actually reduce the selling pressure on the native token and help bootstrap positive, reflexive behavior. This is quite different from the Compound model, where liquidity miners recycle assets to mine COMP and then immediately sell COMP to offset their interest expense.

In other words, when using Aave, you generate yield by holding AAVE tokens, whereas when you use Compound, you generate yield by selling COMP. It’s no surprise then that Aave’s native token (LEND, which is becoming AAVE) has gone straight up, while Compound’s token (COMP) has gone straight down. Token accretion models matter.

Source: TradingView

Further, when comparing Aave’s token accretion model to that of most Centralized Exchanges (BNB, FTT, LEO, HT, etc.), it’s easy to understand why investors are flocking towards DeFi. When an exchange conducts a buyback and burn of its native token, it’s symbolic, but there is no real value accretion for holders because no actual cash is received. A token holder can still be rewarded, but only if the token accretes value due to scarcity, without really having any control / voice on the decisions made by the exchange. Again, token accretion models matter.

2. Community Governance ~ Equity Voting Rights

We’ve established that cash flows matter, but arguably the biggest driver of DeFi’s recent success is in its Community / Governance. There is an old adage in the digital asset space that “community is everything” -- with the success of Synthetix (SNX) and ChainLink (LINK) serving as prime examples. The latest emerging trend in DeFi is putting control of the platform into the hands of the community - e.g., SNX is winding down its Foundation and turning control over to 3 DAOs and Aave’s proposal to migrate to a governance token will allow the community to decide how inflationary rewards are split between stakers and liquidity miners, which assets get listed on the protocol, collateralization ratios, interest rates, and more.

Giving users the right to vote as though they were equity holders not only decentralizes the network, but also forces engagement because it ties the future value of protocol to decisions the community makes today. It’s pretty apparent that governance matters to DeFi users, but what are those voting rights worth?

Enter YFI - The DeFi Aggregator

We can put the value of governance in perspective by studying Yearn.Finance (“YFI”), an automated Decentralized Finance (DeFi) yield aggregator built on Ethereum. Yearn works by automatically depositing stablecoins into the highest yielding lending/borrowing protocols (AAVE, Compound, Curve, and DyDx). As DeFi has exploded, finding the most beneficial rates across all platforms has become a much harder and more time intensive task - even for the most experienced user. Yearn aims to reduce the barriers to entry, increasing the capital pool by attracting new users and making other DeFi protocols more valuable. In other words, it’s as if you had a computer that automatically took your idle cash and deposited it into the highest yielding savings account across all global banks, all day, every day, without you needing an account with any of the individual banks.

Created by Andre Cronje on 7/17/20, the YFI token has no VC backing, no pre-mine, no ICO and no founders reward. The original 30,000 tokens created had to be “earned” via liquidity mining and Andre has explicitly stated that the token has “no value” at all. Nonetheless, YFI is currently trading at ~$4,000/token and has a $120 million market cap. Why? Our past write-ups have touched on this, but it’s worth repeating… successful projects typically have three key similarities, and YFI is no exception:

- Product market fit (PMF)

- Well-designed “tokenomics”

- Community / governance

1. PMF - YFI as the DeFi Aggregator

Given that DeFi has proven product market fit in the digital assets space, YFI as an aggregator of these protocols should also have value. Ben Thompson’s Aggregation Theory requires that three things be true for an aggregator to capture value (with a hat tip to Messari):

- Direct relationship with users? Yes, users can go to Yearn to lend their assets

- Zero-marginal cost for serving users? Yes, it’s free to optimize another user’s deposit

- Demand-driven multi-sided networks with decreasing acquisition costs? Yes, in our opinion

The last requirement is such that when users come to the YFI platform it becomes more attractive for suppliers (other DeFi protocols) to join too because it makes each protocol more valuable and draws in more users, which in turn reduces customer acquisition costs for the platform (in this case, YFI). There is an established symbiotic relationship between other DeFi protocols and YFI where both can accrete value to users. A real-world example would be Expedia or Travelocity and its airline/hotel counterparts -- while each airline/hotel may prefer to draw customers directly to their own websites (and have tried), the aggregators make the user-experience easier, and after achieving critical mass, the hotels/airlines no longer have a choice but to participate.

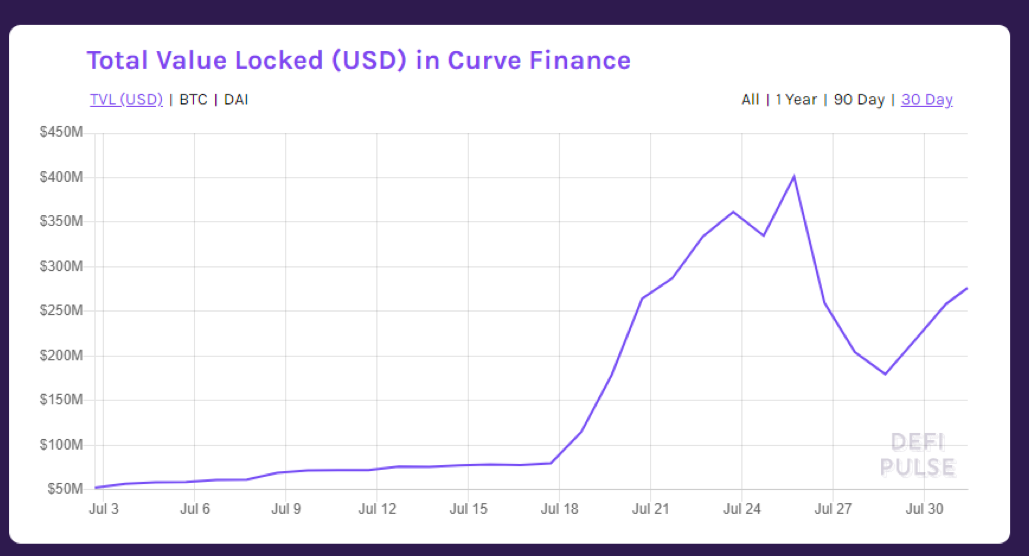

Before YFI, Curve Finance (CRV) had $100 million in Total Value Locked (TVL). When YFI farming began, CRV TVL jumped to $400 million within a week and even after liquidity mining incentives ended, CRV continues its upward trajectory.

Source: DeFi Pulse

YFI is also not just a yield aggregator for stablecoins. The second iteration of the network (YFI v2) will have a more user friendly dashboard and will introduce a whole new set of yield tools previously only accessible to the most experienced DeFi coders, such as: ytrade (finding arbitrage opportunities), yliquidate (the ability to bid for liquidated assets), yleverage (taking advantage of funding rates), ypool and smart contract credit delegation lending. Token holders may be able to control how capital is allocated to various strategies and how creators are compensated for publishing those strategies.

2. Well Designed Tokenomics

Originally, there were only 30,000 YFI tokens which could be “earned” via liquidity mining and by participating in the governance process. The first pools distributed 10,000 each via the CRV and BAL pools of 98%/2% DAI/YFI and 98%/2% yCRV /YFI.

Scarcity value (30k initial supply), imbalanced pool ratios (when a user contributes DAI to a 98%/2% YFI Balancer pool they’re essentially market buying YFI) and staking YFI to earn more YFI within a 10 day distribution period all combined to drive up the token price. Whether YFI will retain/enhance its value will be up to its community, which will vote on future supply and inflation. Voters have to balance the need for future inflation to incentivize the Founder (who owns very little of his own token) and attract liquidity providers versus over-inflation / dilution.

3. Community / Governance

YFI is truly decentralized in the sense that any change to the ecosystem goes through on-chain voting and proposals. YFI is only two weeks old (compared to AAVE and SNX which have been established in this space for over two years), and there are already 31 YIPs (YFI Improvement Proposals), an extremely active Discord, and a Telegram group with over 1700 active users.

However, the decentralization process happened so quickly that there will be, and have been, bumps in the road. YFI has already been forked numerous times (YFII,YFIII, etc.), Quorum had to be reduced to 20% in order for proposals to pass, and only YFI holders can vote rather than Balancer pool token (BPT) holders as a BPT represents 2% YFI. More importantly, to date the only concrete decision that the community has agreed upon is that there will be future inflation; however, the emission schedule and its allocation (between LPs, founders, etc.) has not been finalized.

It’s fair to say YFI is in the early stages of a governance experiment. Price action will be extremely volatile, fluctuating daily as the market attempts to find equilibrium with the odds of each proposal passing. While no one knows what the future holds, it’s evident that the YFI community is willing to risk a lot of capital to voice their opinion on the protocol’s future because they see a massive total addressable market (TAM) both for DeFi and for YFI as the primary DeFi aggregator.

Whether YFI token holders are able to come together and pass proposals in the best interest of the protocol (and whether the market agrees) remains to be seen, but it will be fascinating to watch it all unfold. Regardless, YFI perfectly exemplifies why DeFi matters, and how value accrues in the form of governance and tokenomics.

“Since crypto operates in this regulatory gray area, even US-based projects (albeit somewhat decentralized) have been able to pursue this equity-like giveaway in the form of tokens. These early projects are pioneering a growth hack that will lay the groundwork for many similar models in the future. While the yield-farming craze may seem like the next get-rich-quick scheme on the surface, it represents a novel means of incentivizing a large number of people to perform valuable services for an early-stage network addressing the critical chicken and egg problem of any financial marketplace.”

Notable Movers and Shakers

The headlines will most likely read that Bitcoin finished the week up 11.5%, posting its first double digit weekly gain since May. The headlines may also read that Ethereum posted its second consecutive 20%+ rally last week, outperforming Bitcoin by over 80%. What the headlines will likely leave out is that Bitcoin Dominance posted its 5th consecutive down week (-20bps), showing that the rest of the digital asset space is keeping pace with the King (or Queen!). There is an entire ocean of investable assets in this space, lest we forget, and there is news to be had:

- Crypto.com/Monaco (CRO/MCO) announced an MCO to CRO token swap ahead of their mainnet to phase out their two token model in favor of a one token model. The conversion rate was set at 1 MCO:27.6439 CRO, with a 20% bonus if converted before September 3rd (1:33.1726). At the time of the announcement, the spot ratio was skewed (1:24.72), which gave rise to arbitrage. The current ratio aligns with the bonus conversion round (1:31.68), with MCO gaining 31% to close the gap. Larry Cermak, Director of Research at The Block, astutely pointed out that this token swap comes at the expense of early investors/token holders, as the product offered became significantly (~4x) more expensive and their holdings were therefore diluted. Whether existing users will be grandfathered into the new program is still being hashed out; nonetheless, this points to the potential downside(s) of a two token model - utility and token economics serve better when accruing to a single token within the network.

- The Top 10 had a week of rare outperformance last week, as capital rotated from hot sectors (DeFi) into cold sectors (large caps). Of the Top 10, only Cardano (ADA, -10%) and Binance Coin (BNB, +7%) underperformed Bitcoin (+11.5%). With all the movement in mid-caps of late, some of the legacy projects that compose the majority of the total market cap of the industry were dormant - the shift in the market is worth monitoring as we push through what has been a hell of a year.

What We’re Reading this Week

Institutional Investor details the recent history of Wall Street’s acceptance of Bitcoin, from Paul Tudor Jones detailing his investment thesis in an investor letter to Renaissance Technologies potential investment in Bitcoin futures. However, despite the potential for institutional investor acceptance of the decentralized currency, the US government, particularly the SEC headed by Jay Clayton, has been unwilling to push the envelope for wider Bitcoin adoption. The interest and acceptance of Bitcoin from Wall Street has grown only in the last year and very much hinges on how the US government chooses to regulate it.

Last week, the Bank of Japan (BOJ) officially said it needed to further the development of a digital Yen and it is now a chief concern for the central bank. Previously, the Bank of Japan had discussed its experimentation with Central Bank Digital Currencies (CBDCs) but said there were no plans to launch one in the near future. The statements last week are a change of stance for the BOJ, likely in regard to China’s advancing digital yuan, DCEP, which is well into the testing and piloting phases. China’s CBDC poses potential national security threats and therefore the development and launch of a digital yen has been made a top legislative priority this year.

Huawei recently applied for a patent that covers blockchain storage methods and devices. This patent adds to a number of others that the Chinese tech giant has filed related to blockchain-settlement methods. Huawei also recently signed a “strategic cooperation agreement” with the People’s Bank of China (PBOC). Although the details of the agreement are not public, it is believed the agreement is related to the PBOC’s digital yuan project, DCEP. With the launch of DCEP coming soon, it will be imperative that technology providers can provide safe storage for these new digital assets.

Last week, Chinese authorities arrested 27 alleged masterminds behind the Plus Token crypto scam that netted the group $5.7B. The pyramid scheme was believed to have run 3,000 layers deep, deceiving over 2 million people in the process. The operation was led by 109 individuals, most of whom escaped China with only 6 arrests made in 2019. This case marks the first time Chinese authorities have cracked down on a crypto-related Ponzi scheme. It is unclear how many additional members of the scheme are yet to be arrested and if victims will be returned any of their funds.

And That’s Our Two Satoshis!

Thanks for reading everyone!

Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA - Chief Investment Officer

Katie Talati - Head of Research

Hassan Bassiri, CFA - PM / Analyst

Sasha Fleyshman - Trader

Wes Hansen - Head of Trading & Operations

Alex Woodward- Analyst

To learn more or talk to us about investing in digital assets and cryptocurrency