What happened this week in the Crypto markets?

A Pragmatic, Subtle Shout Out to Bitcoin That Everyone Missed

There are 3 classes of investors when it relates to crypto:

The Extremists

- Those that believe everything in crypto is going higher

- Those that think everything in crypto is a scam and will never touch it

The Bitcoin Maximallists

- Those that think Bitcoin is the only digital asset that matters, and believe BTC will be at worst a $7 trillion store of value (i.e. Gold) and at best, the global reserve currency

The Pragmatists

- Those that believe Bitcoin has real value, but there are also a select few other digital assets that will create immense societal and investment value (and remain open-minded to new developments).

The Extremist camp essentially runs the media. These polarizing opinions shape narratives, which leads to even more polarizing extremes -- it’s a circular loop.

The Bitcoin Maximallists may end being right, or they may end up being very wrong. Either way, it’s effectively a religion so there is no point in trying to debate.

The Pragmatists, where Arca resides, are the ones that can probably influence the most minds simply because their minds are also malleable themselves. During a week when Trump and Powell dominated headlines (we’ll get to that), it may have been a pragmatic take from ex-Franklin Templeton legend, Mark Mobius, that ends up meaning the most. Mobius spoke on Bloomberg TV and said:

“I’m not a buyer [of Bitcoin] but I realize that it is something we have to account for. The reason why I am not a buyer is that I don’t know what the real value is and unless it is so widely held and accepted then that’s a different story. Let’s face it: all currencies are based on faith. If you have faith in the dollar or faith in the renminbi or faith in the euro, whatever it is, then you can use it.

But the problem with these cryptocurrencies is that it is not that widely used. But, at the end of the day, there are many people who do believe in it and if it continues and grows, then I would probably have to be a buyer and be involved in this.”

He’s right, and we applaud his open mindedness considering he is on record saying the exact opposite just 1 year ago. Bitcoin and other digital assets may not be for everyone, and they may not make sense today. But to ignore them at this point is pretty dangerous. Those that want to be early should be investing now. Those that want to wait will have plenty of chances, albeit most likely at higher prices, if they ever decide to enter.

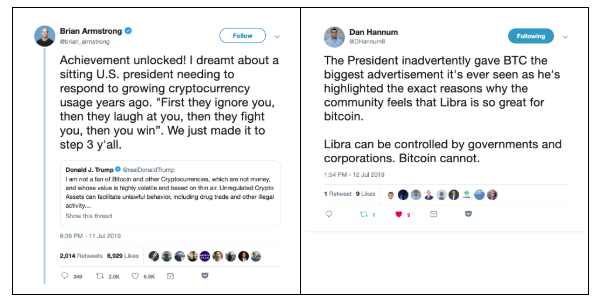

Trump & Powell Just Elevated Bitcoin to “It Matters” Status

Speaking of saying one thing and flipping your stance later, President Trump generated the biggest crypto story this past week. To over 60 million followers, Trump tweeted that he is “not a big fan of Bitcoin”, immediately introducing the word “Bitcoin” to millions of people who probably never thought twice about it before. This tweet followed Fed Chairman Powell’s comments in front of Congress earlier in the week, when he was asked whether Bitcoin could become globally adopted rendering other reserve assets worthless, to which Powell responded:

“I think things like that are possible but we really haven’t seen widespread adoption. Bitcoin is a good example, almost no one uses it for payments, they use it more as an alternative to gold, it’s a store of value, it’s a speculative store of value like gold.”

Once again we have a pragmatic response (Powell) overshadowed by an extreme response (Trump). And this entire debate was sparked of course by the even more extreme reactions to Facebook and their Libra project, where everything from investigation to outright ban is now being discussed.Our takeaway remains the same. Facebook matters more than anything else in crypto because it is forcing discussion earlier than many anticipated. If this project moves forward, it opens 2 billion people to this technology. If it fails, it fuels the fire for those that know this revolution can’t be stopped anyway.

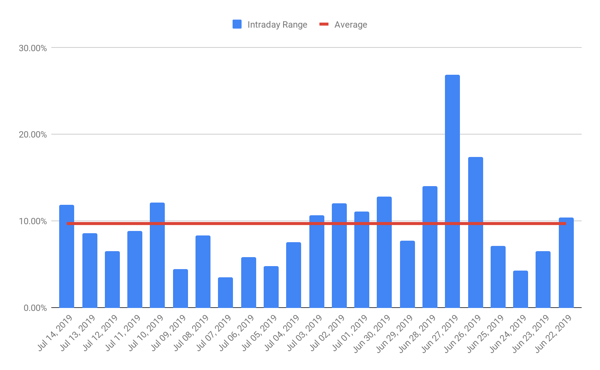

Volatility is Not Subsiding

Meanwhile, volatility remains incredibly high. To illustrate what kind of market environment we're in right now, Bitcoin has moved in an intra-day average range of 9.70% since June 22nd (peak-to-trough price over each 24-hour period). That's incredible volatility.

Further, because Implied volatility is so high (even higher than realized volatility), a July 26th expiry BTC in-the-money straddle (expiry less than 2 weeks from today) trades at $1600 vs BTC at $10,000 spot, meaning BTC would have to move up or down 16% in just 2 weeks just to breakeven. Again, that's incredible.

Bitcoin Recent Volatility as Measured by Intra-day Trading Ranges

Leverage, Leverage, Leverage

The only thing that can kill crypto is crypto itself. Thy sword is leverage. We began talking about the explosion of leverage and derivatives last week and the week before, but another week with 30% intra-week price moves warrants a further, deeper discussion.

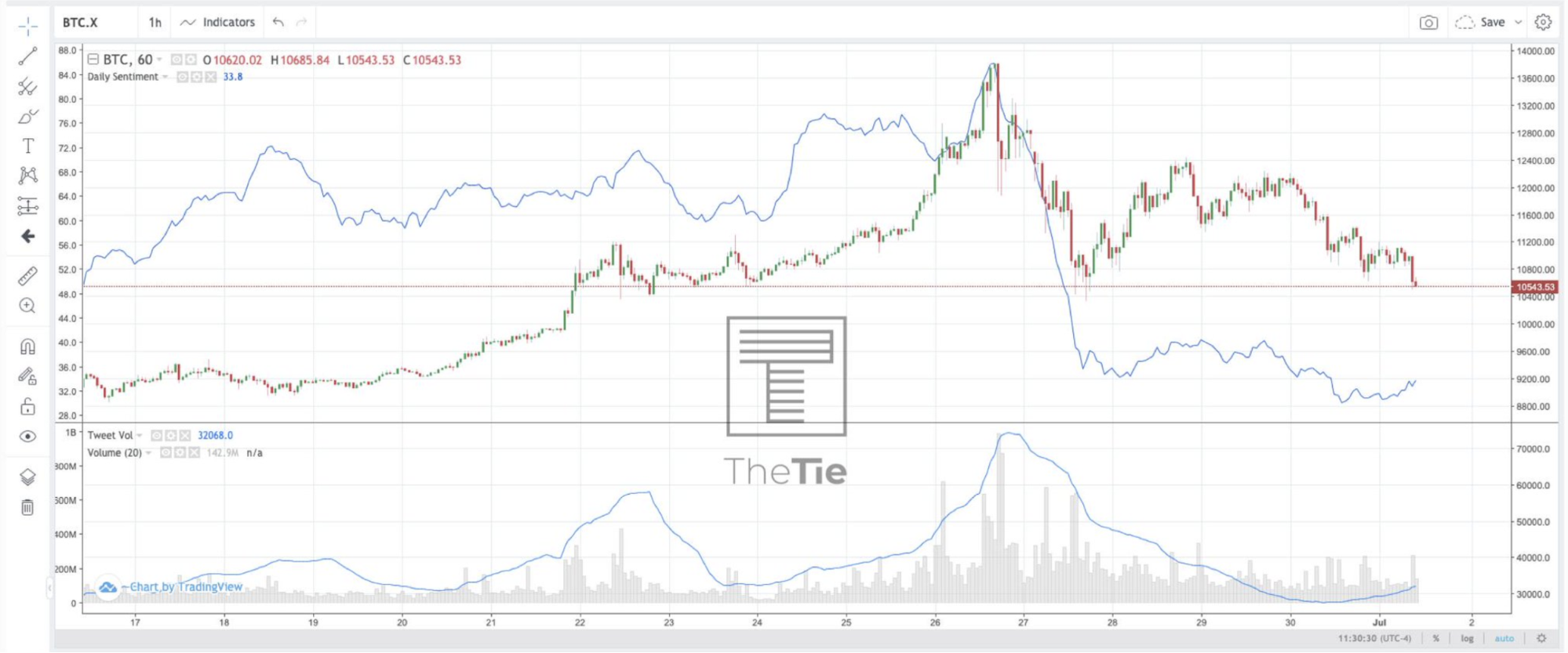

The Bitcoin price ascent from $4k-$10k was based on a confluence of real factors (depreciating Chinese currencies, the Fed’s pivot to a dovish stance, excitement about infrastructure growth including Fidelity and Facebook, etc), but the recent moves from $10k to $14k, and back to $10k, and back to $13k, and back to $10k seems to be entirely based on leverage and sentiment. Little, if any, new money came in or out over the past 4 weeks, but new money was created via leverage. And levered bets are what cause massive volatility, on the way up and down.

Courtesy of TheTie, we can see how we may have gotten into this mess. The Facebook Libra announcement on June 14th led to a sharp increase in sentiment (blue line), which drove the Bitcoin price run-up until the June 26th crash, and since then, sentiment has declined dramatically.

Bullish Sentiment jumped on June 14th after the Facebook Libra announcement

When sentiment shifts dramatically, so does confidence. And confidence is often expressed using leverage.

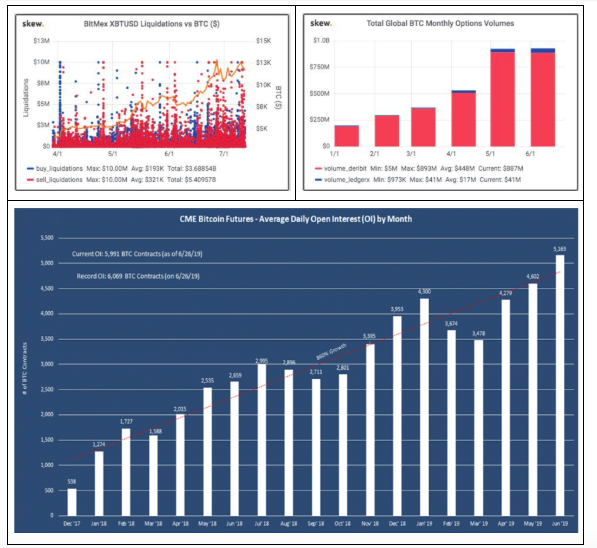

Courtesy of our friends at Skew:

“Since the start of Q2 when the Bitcoin rally resumed, total liquidations of longs (margin calls) = $5.4bln, while total liquidations of shorts = $3.6bln. This is despite Bitcoin going from 4k to 13k in basically a straight line. This is the best evidence that longs use more leverage than shorts structurally. The growth in trading leveraged derivatives instruments such as futures, perpetual swaps and options can be measured by the growth in open interest and volume.”

Crypto Leverage as Measured by Long/Short Liquidations and Growth in Options/Futures

The irony of course is that Bitcoin’s birth in 2008 was a response to absurd monetary policy pumping up stocks, bonds and hard assets, which ultimately caused rampant inflation while saddling society with unsustainable government and private debt.

Yet in the past 4 weeks, crypto has been pumped up by unsustainable leverage via futures, options and decentralized finance tools, while the crypto community continues to chastise monetary policy.

Until this leverage gets sucked out of the system (and it will, it always does), the market may remain very volatile. We’re already seeing the effects of such levered unwinds in the form of other tokens for sale that have nothing to do with this leverage (EOS -25% in one day earlier this week for example). In order to raise collateral to meet margin calls, people will sell anything they own rather than selling based on views/news.

Does the introduction of derivatives lower the volatility of Bitcoin or do they increase it? Derivative contracts provide an interesting conundrum.

In theory, with equal buyers/sellers, it smooths volatility. The reality is, with so much momentum chasing and many unregulated exchanges offering as much as 100:1 leverage on perpetual swaps, it most certainly adds to volatility.

Notable Movers and Shakers

Last week was nothing short of a bloodbath (BTC down 11%, while BTC’s market cap relative to the rest of crypto rose 3.5% to 65.8%), there were notable movers - just not in the direction one would hope. Regardless, there was real fundamental news that offer new data points for various tokens:

- Binance (BNB) announced on Thursday that the team would be giving up just south of $2.4B (80M BNB), contributing them to the overall burn of BNB. The total number of BNB to be burned has not changed (100M BNB), so the main takeaway from this action is that the team is forfeiting their tokens, opting to base their success off of their revenue stream in the future as opposed to their original allocation. While this reads as positive news, the token still fell 16% this week - a testament to the carnage this week offered.

- Siacoin (SC) stated in a blog post Wednesday that they closed a funding round of $3.25M led by Bain Capital Ventures. They went further in stating that this seed round will ‘help the company scale the development and adoption of Sia’. While this news was received well, the token suffered the same fate as the rest of the digital assets space (-11%).

What We’re Reading this Week

Last week Blockstack became the first token offering to be approved by the SEC to raise under the Regulation A+ framework. Regulation A+, known as the "mini-IPO", allows a private company to sell up to $50m in securities to all investors (not just accredited investors). This is considered a milestone for digital asset offerings as it is the first token offering to be approved under this framework. Of note: by seeking this route for approval, the Blockstack token is considered a security, although it is designed to eventually become "decentralized enough" to be considered a utility token the same way Ethereum is. This will be an interesting project to watch unfold especially with additional issuances, developer rewards and mining - all of which are technically considered "offerings".

Since Facebook’s Libra announcement, many central banks and financial incumbents have scrambled to pull together their respective strategies for digital assets. The latest is the People’s Bank of China, whose research bureau director commented last week that the potential for a global payments system like Libra will push the PBoC to continue working toward a central bank digital currency. The main concern the PBoC and other central banks have with Libra, is that it is highly dependent on the US Dollar. Such dependency can make it difficult for these countries to dictate their own monetary policy.

Last week, Laura Shin, host of crypto podcast Unchained, spoke about how the media coverage in crypto does not always hold themselves to the highest standards with journalism. Many outlets engage in “pay to play” schemes where journalists accept gifts or money in exchange for positive coverage, often misleading unsuspecting consumers. Shin attributes this to the “global nature” of cryptocurrency where other writers don’t necessarily adhere to the journalism norms of the West.

Visa Pours Millions into Crypto Custody Provider Anchorage

Last week, Visa and Blockchain Capital announced it was backing a $40m Series B round into Anchorage, a crypto custodian. In addition to offering custody of digital assets, Anchorage is also working to incorporate broader features such as support for staking, auditing and tax preparation. These are all currently major pain points for investing in digital assets and barriers to entry for institutional investors. Interestingly, Anchorage is a member of the Libra Association along with Visa and Andressen Horowitz (Series A investors).

TZero, the alternative trading system backed by Overstock, announced it would be working to tokenize the first major theatrical film, “Atari: A Fistful of Quarters”. The film production and financing company, Vision Tree, is hoping to raise $40m through the offering, with tZero assisting with production and distribution of the token. The token will not only pay out investors from the movie’s earnings, but also allow investors a chance to become more involved through voting on the trailer and the movie’s cast. The tokenization of non-traditional assets, such as movies, through Security Token Offerings (STOs), allows for broad distribution and differentiated returns.

And That’s Our Two Satoshis!

Thanks for reading everyone!

Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA - Chief Investment Officer

Katie Talati - Head of Research

Hassan Bassiri, CFA - PM / Analyst

Sasha Fleyshman - Trader

Wes Hansen - Head of Trading & Operations

To learn more or talk to us about investing in digital assets and cryptocurrency call us now at (424) 289-8068.

.jpg)