What happened this week in the Crypto markets?

Don’t Let a Terrible Finish Distract You From a Great Quarter

The crypto markets may have limped to the finish line, with Bitcoin declining 24% from the mid-week peak (more on this later), but not before putting up one of the greatest quarters and first halfs of any global asset class in history.

Bitcoin rose 26% in June, following monthly gains of 12%, 7%, 29% and 62% over the prior 4 months. Bitcoin gained a respectable 11% in the 1Q, and then 163% in the 2Q. Year-to-Date, Bitcoin is now up 192%. The rest of the Digital Assets space kept pace, with a variety of passive crypto indices also up 100-150% YTD.

As a general reminder, snapshots based on arbitrary points in time are not very relevant. We all know that digital assets, including Bitcoin, were demolished in 2018 posting 70-90% declines. So by no means are we trying to erase the past. However, it’s worth noting that the arbitrary 2019 timeframe is no different than the arbitrary 2018 timeframe. Falling from a peak in January 2018 is no more credible of a data point than rising from the ashes in 2019. Instead, let’s frame this a different way.

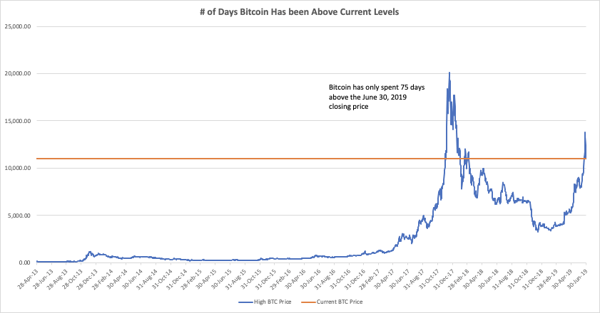

There have only been 75 days in Bitcoin’s history where BTC traded above where it is currently trading.

That means, unless you bought Bitcoin from December 2, 2017 to February 10, 2018 (or a few days in March 2018), you now have a gain on your investment in USD terms. Let that sink in before moving on.

The Perfect Storm

We continue to believe that Bitcoin is in a Goldilocks situation. If global markets rally, Bitcoin and the rest of the digital assets space will likely rally too, as there is no better risk/growth asset on the planet right now than digital assets. But if macro factors continue to deteriorate, crypto markets with Bitcoin may also continue to rally as a global safe haven.

Take for example the outlook for US Equities from our friends at Cantor Fitzgerald:

“We think U.S. equities are making new highs for several reasons:

- They are rich (at just under 19x LTM earnings)

- Earnings are at best flat for the first two quarters with revisions now negative for the third quarter

- For two quarters, lending standards have tightened to U.S. businesses and the consumer, whose wages are too slow to grow in real terms (only +1%)

- Corporate leverage is now excessive on a ‘stock’ basis but with rates still relatively low, it can be ignored on a ‘flow’ basis

- The global economy is weak, led by China, which is likely in the midst of a default crisis after the seizure of Baoshang Bank

- Oil markets are reacting to a potential conflict with Iran with oil prices back above $60/bbl despite weaker demand

- Property prices are rolling over and beginning to fall in some of the largest U.S markets, with NYC leading the way

- And, the Fed is concerned about a U.S. slowdown (don’t be fooled by the inflation smokescreen) and will likely cut at its next meeting, and the ECB is putting QE back on the table given horrible growth in Europe

If that did not make sense, it should not have. Risk-reward to equities is as poor as we’ve observed since 2007, and investors have pushed their chips ‘all-in’ on the ability of a late cycle cut to save the day.”

These macro headwinds are all leading to global instability, declining currencies, and loss of purchasing power. Further, the debt spiral can only be controlled via default or inflation. This is undeniably bullish for Bitcoin, and of course, also very bullish for Gold. But as our friends at Messari wrote recently, “Imagine being spot on the trends underpinning your 10 year macro thesis, but still being dead wrong on the optimal way to invest effectively around that thesis.” This hit home, as there are thousands of very smart investors who have been calling for this Central Bank debt-fueled circus to unwind since 2011, shortly after the start of coordinated global Quantitative Easing. Many of these investors expressed their views by shorting equities, in the face of the largest and longest bull market in history. Others bought Gold, and have since lost 22% from 2011 to today (even with the recent rally).

We may be finding out that Bitcoin is, and has been, the best way to play this “end of the world” scenario. Some of the big banks don’t seem to recognize this yet, and may regret publishing such hilarious artifacts.

Hit The Brakes -- Didn’t Bitcoin Just Implode to End the Month?

Yes, yes it did. June may have ended with headline-worthy numbers, but it was a brutal month with unprecedented volatility.

- From June 1 - June 10: BTC fell 12%

- From June 10 - June 26: BTC rose 81%

- From June 26 - June 27: BTC fell 24%

- From June 27 - June 30: BTC rose 3% but traded in a 15% peak-to-trough range

Volatility itself is not a dirty word, as long as the returns are commensurate with the risks - and thus far in 2019, they have been. That said, there is a difference between high volatility caused by natural market forces, and unnatural volatility caused by excessive leverage and outsized risk-taking. Bitcoin rallied through June 26th essentially without retracements, resembling the trajectory it had in 2017. Such rallies are inherently unstable and prone to sudden and violent collapses, which we just witnessed at the end of the month (and which we warned about last week).

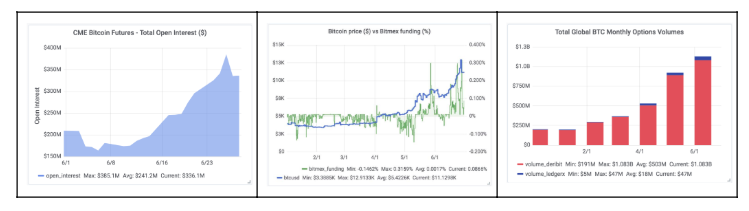

This rapid ascent in price started for real reasons, but ended with massive levered gambling buying. We witnessed record futures, options and other derivative volumes all skewing bullish and short-dated, coupled with unstable long/short ratios, and unregulated exchanges offering 100:1 leverage to investors who thought higher prices were a foregone conclusion. In a 24-hour period, shorts were all liquidated on the way up, and levered longs were all liquidated on the way down. Crypto OTC dealers indicated that some clients were maxing out post-trade settlement limits, and requesting increases. When funds can’t meet capital calls, everything becomes for sale. As we joked earlier in the week, only the crypto markets could turn a rampant bull market into a 2008 leveraged unwind.

The fallout from this 24-hour, 30% rise and fall has yet to play out. Some funds will undoubtedly unwind over lack of risk controls. Some of this can be traced back to poor risk management, while some is due to the lack of prime brokerage services. Leverage requires collateral, but it’s virtually impossible to keep all of your crypto collateral in one place, which means it’s very easy to get liquidated on the upswing and downswing even if your total assets easily cover your capital calls. Further, it’s almost a slam dunk now that an ETF won’t be approved any time soon, as an 81% 14-day levered rally, most of which occurred after US trading hours, is not exactly the formula for successful SEC approval.

The long-term trend for digital assets is still incredibly bullish. Bitcoin has transcended crypto, and has now infiltrated mainstream media, economics, finance and politics. Similarly, there is a whole slew of other companies and projects that have used tokens to issue valuable, investable securities, while other projects have grown their networks via strong partnerships with Fortune 500 companies. The future is very bright; but don’t be surprised if July starts off on rocky footing.

Crypto Leverage in 3 charts:

Notable Movers and Shakers

Bitcoin finished this week exactly where it started, but the path taken was volatile. On Monday Bitcoin was well on its way to achieving year-to-date highs, by week end, however, it somewhat mercifully rested at $11,000. In fact, it was so volatile that the high-to-low drop was a staggering 25% in a 24-hour span. This kind of volatility makes it easy to lose sight of the market as a whole but there were some noteworthy performances:

- Chainlink (LINK) continued to show strength this week (+87%). Following Google Cloud press release two weeks ago, last week LINK was the benefactor of two liquidity events. Coinbase announced Wednesday that Chainlink would be listed on Coinbase Pro, with a secondary announcement Friday that the token would be available on Coinbase’s retail platform. According to a blog post from December of 2018, Coinbase had been reviewing the addition of Chainlink for a while now.

- VeChain (VET) received a flurry of interest after Walmart China announced their partnership Tuesday, rising as high as 63% before finishing the week up 15%. The significance of this partnership is discussed in the next section.

- Neo (NEO) had a week that paralleled Bitcoin in terms of price action - although finishing flat, their Wednesday announcement regarding the official launch of the $100M EcoBoost fund created significant volatility (+46% at highs). The EcoBoost fund is a three phase program, with the first phase focused on “establishing long term partnerships to facilitate the organic growth of the whole NEO ecosystem”.

What We’re Reading this Week

Walmart China has launched a blockchain platform in partnership with VeChain to trace food safety beginning with 23 products. The purpose is to allow customers to scan products and view a detailed history of the item’s source and history. VeChain allows Walmart to conduct such a program on a large scale, giving peace of mind to consumers who purchase food at Walmart.

Big Banks Ramp Up Crypto Efforts

In the wake of Libra’s launch last week, large financial groups are gearing up to launch their own digital tokens. According to Bloomberg Japan, JP Morgan will start trials of its JPM coin with corporate customers before the end of this year. The coin will mostly facilitate settlement of intercompany remittances in addition to assisting with bond and commodity settlement. It was also reported that Goldman Sachs’ CEO hinted that the bank may launch its own competing cryptocurrency. The firm is apparently carrying out “extensive research” as they believe that tokenization and stablecoins are “the direction in which the payment system will go.”

Malta’s Prime Minister, in an interview last week, announced that the country would be putting all rental contracts on a blockchain. The plan has been approved by the country’s cabinet with the goal of increasing security while preventing tampering. Dubbed the “crypto island”, Malta began enacting crypto friendly legislation last year, attracting large businesses such as Binance.

Aid.Tech and PharmAccess Foundation created a project in Tanzania aimed at providing women access to pre and post-natal care using blockchain technology to store their medical information. The project was created after a huge amount of waste and fraud was observed in the aid space. Blockchain based programs remedy these issues ensuring that services and goods are actually being accessed. The program’s first baby was born July 13 last year, giving many hope that blockchain can be used to remedy some of the largest healthcare issues in Sub-Saharan Africa.

And That’s Our Two Satoshis!

Thanks for reading everyone! Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA - Chief Investment Officer

Katie Talati - Head of Research

Hassan Bassiri, CFA - PM / Analyst

Sasha Fleyshman - Trader

To learn more or talk to us about investing in digital assets and cryptocurrency

.jpg)