What happened this week in the Digital Assets market

What happened this week in the Digital Assets market

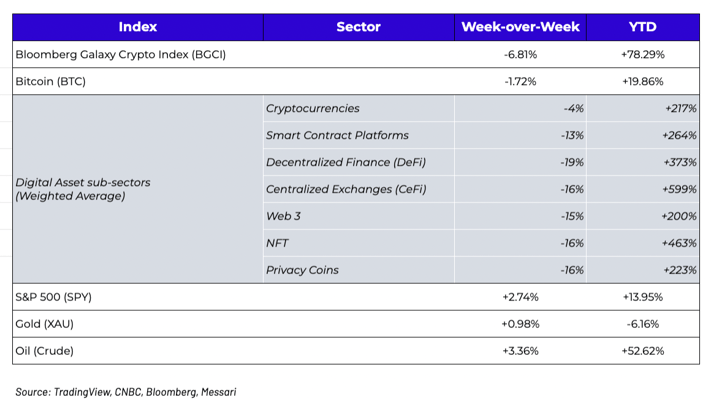

Week-over-Week Price Changes (as of Sunday, 6/27/21)

Debunking the Bear Market ThesesDigital assets had another horrific week across the board, with prices of most assets down 10-30%. And sentiment is as bad as we’ve seen in over a year, as buyers remain on strike while shorts continue to build. This is perhaps a bit surprising given just about every digital asset other than Bitcoin is still up triple-digits YTD. But everywhere we look, someone is shouting “digital assets bear market!”. Here’s the problem though -- we can’t come up with a single reason that validates why the market is all of a sudden so convinced that digital assets are going into an extended funk.

We spent all week asking industry leaders, funds and traders what the bear thesis actually is that has traders (and random BTC number generators) so confident about upcoming price declines. As best as we can determine, here are the most popular bear cases, and our rationale for why each of these is most likely inaccurate:

Debunking Bear Thesis #1: CCP regime change is intent on killing digital assets

The biggest change to the market since mid-May has been China’s stance on digital assets. Our friends at Galaxy Digital put out a nice timeline of the recent events. China’s crackdown has been focused exclusively on Bitcoin miners and digital asset exchanges that offer leverage, but not the actual underlying assets themselves. While China is a very large player in digital assets, and the short-term price declines have potentially been warranted given the shock to the system, it’s difficult to believe that this entire global asset class is at the mercy of a single government interjection. In fact, most market participants agree that long-term results from China’s potential exodus are actually positive, from a redistribution of hash power globally to more ESG-friendly mining facilities. But perhaps more importantly, we’ve already seen exactly what happens when an asset itself is unaffected but the means with which to trade it are shut off. In December 2020, Ripple (XRP) was delisted by almost all relevant exchanges following an SEC complaint about its status as a security and its unregistered token offering. Over a one-week period, peak-to-trough, XRP fell 68% (NOTE: today, XRP is +200% off these lows, and the recovery started roughly 6 weeks after the initial selloff). While most agree XRP has no value, the market told us exactly what liquidity was worth… about two-thirds of the value of the token, for a short period of time. Similarly, when BSV was delisted in early 2019 by the majority of exchanges, the BSV token fell roughly 40%, and this too lasted for just a few months before the token rose again. So if the biggest takeaway of the China news is that exchange access is going to be shut down, and that miners are relocating, we’d expect a similar 40-70% drawdown of the assets affected, and a swift recovery. Well, we’re 6 weeks into this selloff and most assets are already down 40-70%. It would be reasonable to argue that we have already bottomed.

Debunking Bear Thesis #2: Massive regulatory pressure from the US

We already debunked this two weeks ago, and even if it were true, it would be a net positive in the long-run. While it’s cute watching El Salvador pass a law in 3 days, in the US, laws take years to get passed. As enjoyable as it is to watch the markets trade violently every time an official from the Fed, SEC, CFTC, Treasury or a congresswoman opens their mouth, the reality is laws have to change before anyone has jurisdiction. This is years away from happening given laws need to be enacted before any governing body has jurisdiction to regulate this asset class.

Debunking Bear Thesis #3: The Fed will be tapering soon and that is bad for risk assets

Stop. Tapering is not happening anytime soon, the 10 year is still at 1.5%, the US dollar is at a six year low, the VIX is back to pre-Covid lows, tech stocks are booming again… it’s safe to say this is overblown. And even if true, the digital assets market seems to be the only asset class affected by it. Is the most retail-dominated, inefficient, immature asset class really the only market that has the Fed tapering view correct?

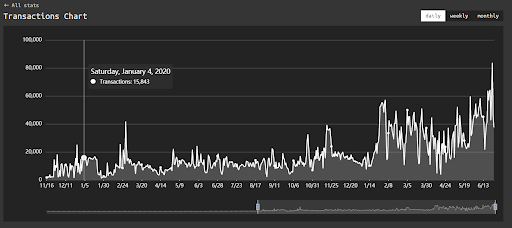

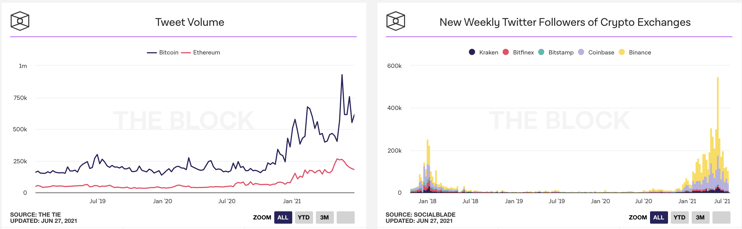

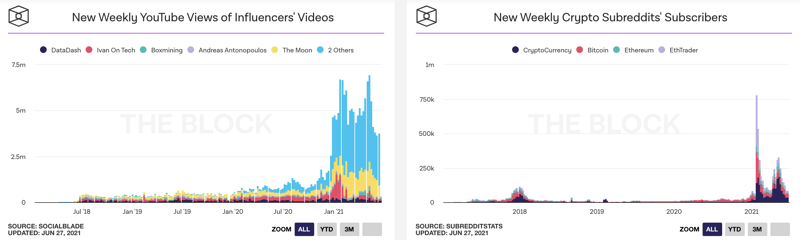

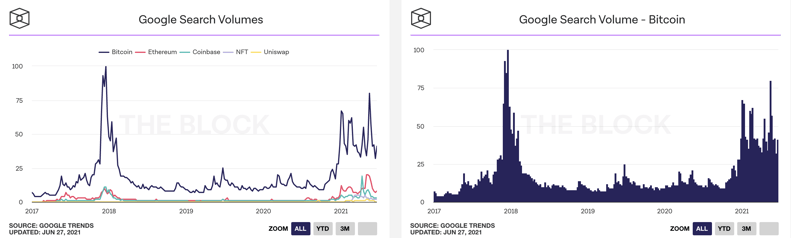

Debunking Bear Thesis #4: Retail momentum and interest is dead

Off the highs… sure.

Dead and never coming back? Not. Even. Close.

Source: TheBlock

Debunking Bear Thesis #5: Lack of institutional interest

We speak to institutional investors every day. They are still allocating to funds, in record sizes. Goldman Sachs and Citi just launched digital asset divisions specifically due to client demand. a16 just raised a record $2.2 billion fund dedicated to digital assets. For the first time on record, junk bonds yield less than inflation… tell me again where you think money will be flowing if not into new asset classes like digital assets?

Debunking Bear Thesis #6: ESG concerns

First, the ESG concerns are entirely specific to Bitcoin, and not at all relevant to most other digital assets. In fact, most other digital assets are positively influenced by the conveniently forgotten S & G. Second, as noted in #1 above, the redistribution of hash power away from China to more clean energy sources around the globe will be a net benefit for the environmental concerns. Stay tuned for Arca’s ESG paper coming next week.

Debunking Bear Thesis #7: Tether, Celsius, BlockFi, Binance risk

It would take 40 pages to summarize all of the conspiracy theories about these four companies. What’s most relevant to the current market selloff, however, is that none of these concerns are new, and therefore cannot be used as a valid excuse for the current market correction. The market discount regarding this constant uncertainty overhang has been persistent, and has had no reason to widen over the past six weeks. Should any of these companies actually run into financial or regulatory issues, then the question of systemic risk will rightly be discussed, but these “what ifs” are lazy excuses for a current market correction. In our opinion, only Tether poses systemic risks, given how intertwined USDT is to the working capital of all exchanges and DeFi, but even that would quickly be replaced by other perfectly comparable stablecoins should a problem actually arise.

Debunking Bear Thesis #8: Microstrategy is going to be a forced seller of Bitcoin

This is the dumbest of all fears as it is 100% not accurate and can be easily disproved by looking at the bond covenants. Any fears of MSTR being a forced seller of BTC, or being "liquidated" is a complete farce and a misunderstanding of how bond covenants work.

Debunking Bear Thesis #9: Grayscale (GBTC) unlocks are going to crush the market

Nope. When you buy GBTC from Grayscale, you are subject to a 6-month lockup. The biggest unlocks are happening over the next 2 months, which could lead to heavy selling of GBTC on the open market. But this has no effect on Bitcoin itself -- the Bitcoin in the trust does not trade, only the shares trade (and thus, GBTC will likely continue to trade at a steep discount to Net Asset Value). Moreover, since most buyers of GBTC were doing it for the arb back when GBTC was trading at a premium to NAV, they were also shorting Bitcoin. A hedge fund would:

a) borrow bitcoin

b) contribute bitcoin in-kind to create GBTC shares

c) short futures or spot to hedge out directional risk

Thus, as funds unwind this trade (even though it will now be at a massive loss since the arb went from a premium to a discount), it could actually put BUY pressure on Bitcoin, not sell pressure, as those who sell GBTC will have to buy back Bitcoin to cover the short-leg of the trade.

Debunking Bear Thesis #10: Digital assets are reflexive and fundamentals are deteriorating as price declines

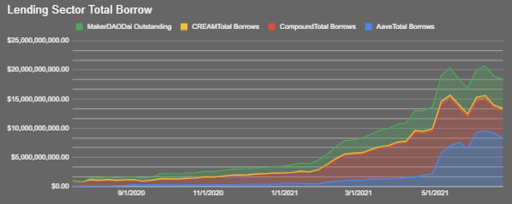

This is probably the most important of all of the bear cases, and it’s just not true. Bitcoin and other cryptocurrencies have no fundamentals, so we can dismiss that sector. But everywhere else you look, across DeFi, gaming, Web 3.0, and other pockets of digital assets with real users, cash flows and adoption metrics, the fundamentals have never been stronger. Many metrics are lower than the May euphoria, but quarter-over-quarter, and year-over-year, the growth is nothing short of phenomenal. When prices go down but revenues go up, it means multiples are contracting -- does multiple contraction make sense for the fastest growing asset class in history?

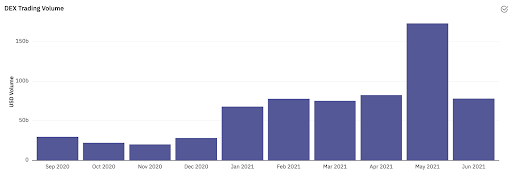

Let’s start with DeFi. The fear of DeFi slowing is more narrative than substance. Across DEXs, Lenders and Stablecoins, the 2Q of 2021 is the best quarter in history, and June is the 3rd best month in history. The problem is, May was the best month ever, so month-over-month, we are witnessing a steep decline. Do these look like graphs worth being concerned over? “We’re back to levels not seen since 2 months ago!” (and still more than double any month in all of 2020).

Moreover, you can look at many individual projects with tokens that are down -50-70% even though metrics are at all time highs. This of course doesn’t mean the tokens are cheap today (maybe they were expensive last month), but it does show you that the declines in price are not indicative of a decline in fundamentals, and there is no impetus for a multi-month bear market. For example (amongst many others):

- Aave (AAVE): all-time high on TVL (total value locked = assets under management); AAVE token -66% since mid-May.

- Yearn Finance (YFI): Quadrupled revenue in 2Q (vs 1Q), and has the same AUM as Acorns. YFI Token -66% since mid-May.

- Axie Infinity (AXS): $28 million of volume in May; did $6 million alone yesterday. Record revenues, record DAUs, record growth. AXS token -65% since April.

- Chiliz (CHZ): Generated $10 billion of trading volume for its Fan Tokens in May, with one of its latest FTOs seeing over 19k users participating. We estimate CHZ may have generated ~$30mm of revenue in June, growing over +200% on a 6-month rolling basis, and have signed partnerships with NHL and NBA teams, along with soccer, racing, cricket, esports and fighting leagues. CHZ token -73% since mid-April.

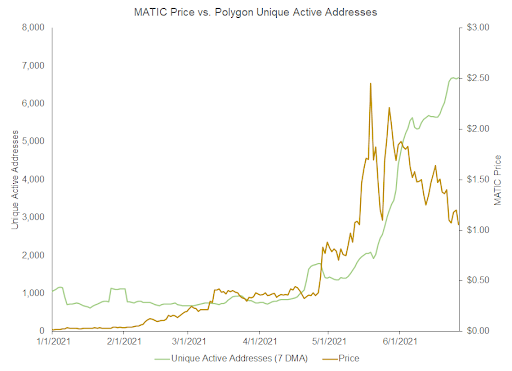

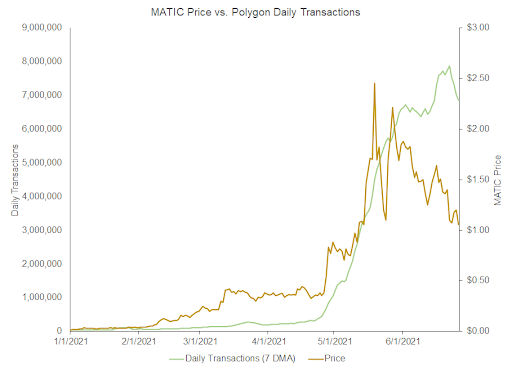

- Polygon (MATIC): Record growth in unique addresses, transactions, and network revenue; MATIC token -55% since mid-May.

|

|

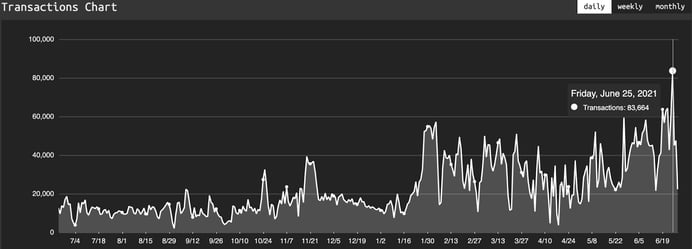

- Arweave (AR): transactions hit all-time-highs on Friday, +30% above previous record. AR token -56% since mid-May.

We will soon find out if this really is an asset class. When other asset classes crash for no reason, opportunistic buyers step in, as value investors rotate from one asset class to another. There is clearly value in digital assets today. While many are calling for a bear market -- the data simply suggests otherwise. Whether or not this is enough to attract new buyers remains to be seen.

What’s Driving Token Prices?

Prices are down a lot… but not based on any substantial news developments:

- SUSHI (-7%): A substantial development bridging traditional finance with digital assets as ITrust Capital allowed for investing in SUSHI within an IRA. As this precedent has been set, expect more developments between digital assets and traditional financial planning.

- FTT (-24%): FTX partnered with MLB as their official cryptocurrency sponsor. This is their third branding deal within the last three months with major sports teams. Exchange volumes bounced on Friday making this week a positive overall boost.

- UNI (-12%) : The digital asset space is attracting top talent from major Wall Street companies. Uniswap Labs hired COO Mary Catherine-Lader, who previously worked at Blackrock.

- NXM/wNXM (-9%/-6%): iTrust.finance, a staking platform, launched vault staking for NXM and wNXM, allowing users to stake against an index of NXM contracts to spread out their risk. This should open up additional capacity on NXM. Revenue was down WoW but the number of covers purchased remained flat indicating consistent interest but lower asset prices.

What We’re Reading This Week

And That’s Our Two Satoshis!

Thanks for reading everyone!

Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA - Chief Investment Officer

Katie Talati - Head of Research

Hassan Bassiri, CFA - PM / Analyst

Sasha Fleyshman - Trader

Wes Hansen - Head of Trading & Operations

Alex Woodard- Analyst

Mike Geraci- Trader

To learn more or talk to us about investing in digital assets and cryptocurrency

Source: Dune Analytics / Arca Estimates

Source: Dune Analytics / Arca Estimates