What happened this week in the Crypto markets?

What happened this week in the Crypto markets?Week-over-Week Price Changes (as of Sunday, 6/22/20)

|

|

WoW

|

YTD

|

|

Bitcoin

|

Flat

|

+28.9%

|

|

Bloomberg Galaxy Crypto Index

|

-1.3%

|

+32.9%

|

|

S&P 500

|

+1.8%

|

-4.1%

|

|

Gold (XAU)

|

-1%

|

+16.3%

|

|

Oil (Brent)

|

+7.8%

|

-35.3%

|

Source: TradingView, CNBC, Bloomberg

The Traditional Markets Are a Mess

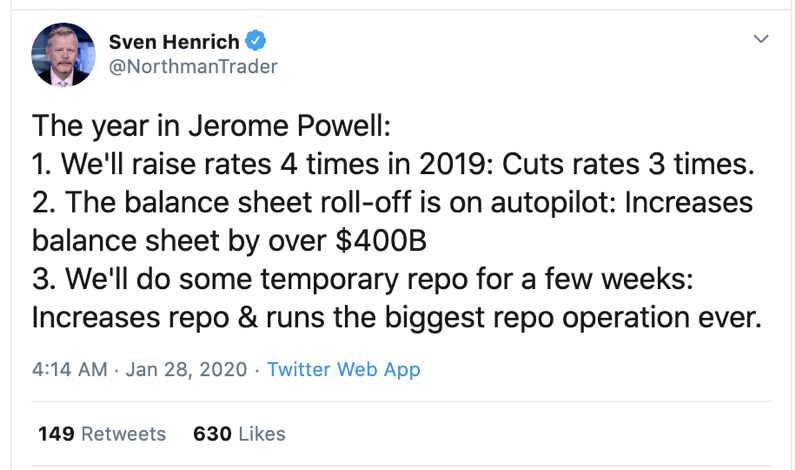

The capital markets are a complete mess, despite what asset prices are telling us. The Fed's Neel Kashkari warned that bank losses during COVID-19 could “trigger the next financial crisis”... as if to imply that we’re not already in a financial crisis. If the below isn’t a financial crisis, then what is?

Every action by the Treasury department, the Federal Reserve and central banks around the world has probably been warranted, to some degree. This isn’t even an argument against their actions. But to pretend like we’re not already in a financial crisis just because the paper mache dam hasn’t burst yet isn’t entirely genuine. Every single prediction and statement the Fed has made regarding repo, “not QE”, rate intentions, balance sheet reductions, inflation and employment has been wrong for years, yet we still hang on their every word.

We’ve talked about moral hazards many times, assuming that these were unintended consequences. But just this week, Joe Weisenthal at Bloomberg flat out spells out the moral hazard in plain and no uncertain terms, as if this is a good thing:

“...even though the amount of corporate bonds the Fed has bought (primarily through ETFs at this point) is nominal, the Fed has helped catalyze a massive boom in credit issuance. In 2020, corporations have already issued over $1 trillion in investment grade debt, which is by far the fastest pace ever. By establishing itself as a "lender of last resort" in the corporate credit space, other players have rushed in and done the Fed's job for it. If you know there's a lender of last resort, you don't need the lender of last resort. (The ECB is still the GOAT at this, with Mario Draghi having established a program to backstop sovereign debt in 2012 that ended the euro crisis without ever having spent a single euro cent).”

Government lending of last resort is not the way functioning capital markets are supposed to operate. Of course, none of this matters for debt and equity and real estate investors who are required by mandate to invest in debt, equity and real estate. But for those not required, perhaps fresh eyes are warranted.

Quick aside: My 7-year old son recently took an online animal course and learned about snakes. My wife and I are terrified of snakes after 40 years of being taught to some degree to be terrified of snakes, while my son started from scratch with no preconceived notions. He researched snakes, put together a PowerPoint presentation… and long story short, we now own a ball python. And you know what? They are great, simple, safe pets. The only reason my wife and I were even willing to entertain this idea is because we love and respect our son, even though it seemed crazy at first.

People love and respect their money too. Those that are not willing to listen to new ideas on how to grow and preserve their money are the ones that stand to lose the most from change. Everyone else should be listening right now, and those that are starting from scratch may be the best ones to listen to (and they are buying digital assets).

Can You Invest and Adapt alongside a Company?

Let’s go further into the above concept of fresh eyes and change. When you buy the debt of a company or government, you should know what you’re getting -- a fairly certain fixed or floating rate of return regardless of what this company does over a set period of time. When you buy the equity of a company, you know that you will gain somewhat proportionally to the revenue and profit growth of the company. This all seemed fine when companies actually did what they said they were going to do. Forty years ago, an airline flew planes, a toy store sold toys, and a movie theatre sold tickets to movies. But today’s top companies, largely technology focused, morph and change faster than investors can keep up. Sometimes these pivots workout for the best (YouTube started as a dating app), other times they are unmitigated disasters (WeWork started as a co-working play, but what exactly was WeWork a few years later when JP Morgan tried to stuff investors with $50 billion of toxic equity)?

So this begs the question, “What would you prefer”? Is there value in the investor protection of knowing exactly what you are buying as spelled out for you the day you buy it, knowing full well that it is highly likely that HOW these revenues and profits are ultimately achieved are nothing close to what you thought they’d be, and that you are potentially leaving a ton of money and value on the table as the company pivots? Or would you prefer the flexibility of getting to benefit in new and different ways as the company grows and morphs, but having less investor rights and protections along the way?

Let’s consider the latter for a minute. What if all equity and bondholders of Amazon got to grow as Amazon grew? No one knew all of the different business lines Amazon would ultimately get into, nor did they know that Amazon Prime would be such a great utility for households across the world or that being an Amazon member would give you special access at Whole Foods. Sure, bondholders have done fine and equity holders have crushed it, but could early stage users and investors have benefited even more if they were able to get “rewards” from Amazon as they figured out these new business models? Similarly, could Amazon have benefited more had they taken care of customers as much as they took care of shareholders?

That is exactly what is happening in the digital assets world today. When you invest in a company or project, you are forgoing certainty for the chance to participate in the adaptation of the company. And this is playing out in real-time, with great effectiveness.

The New Compound Token - The Good and Bad of Digital Assets Experimentation

Compound was founded in 2018, backed by well known VC funds Andreessen Horowitz and Paradigm. Compound is an Ethereum-based money market protocol where rates for lending and borrowing are set algorithmically according to supply and demand at any given time, with no middlemen, banks or brokerages.

This company is part of the “Decentralized Finance” (DeFi) or “Open Finance” sector of digital assets, and it is on fire. While there is a tremendous amount of growth happening in this space, from insurance to asset management to banking, the most important aspect is that they are entirely dependent on bootstrapping user growth and adoption.

Compound released a token (COMP) this week, which rose from essentially no value to $300 per token in less than a week (a $0 market cap to over $3 billion, fully diluted). A lot has been written about Compound and how it essentially manufactured growth, so we’ll spare you the details (great recap here and here). But we want to focus on the positives and negatives from this experimental capital markets event.

The Good:

- Product market fit - First and foremost, Compound had already achieved product/market fit long before introducing a token, versus historical projects that used a token as a fundraising mechanism (ICO) before even knowing what their product would become. This allowed the team to understand how best to implement the token, rather than force a token into their capital structure and product design.

- Bootstrapping usage and interest - While they had already achieved product/market fit, this innovative token design and incentive program jump started their growth. Key performance metrics including unique users, outstanding debt, and interest accrued are all up several hundred percent in less than 100 hours preceding the launch.

- Flexible token structure - By waiting, Compound was able to issue a token that fit their needs and their users’ interests. And because the token holders now effectively run the company via governance, the token may change over time too.

- Rewarding early investors and users - Those that took a chance on Compound two years ago via purchasing equity are being rewarded with essentially an “early exit”, and those that have been users of Compound since the early days are being rewarded with the distribution of tokens that have shot up in value.

- Innovation - While somewhat manufactured, the way in which tokens are distributed to both lenders and borrowers in equal increments encourages more borrowing, which had historically been outweighed 3 to 1 by lending.

The Bad:

- Lack of equitable distribution - From the outset of the project's life cycle, Compound founder Robert Leshner signaled his intention to progressively ‘decentralize’ the protocol by removing administrative control privileges from the core Compound Labs development and instead encourage a community of individuals and entities to set market listings, rate curves, risk parameters, among other features. This is great, but it will be 4 years until this token is fully owned by its users, and most of the users will likely take no part in its governance. Instead, the early VCs and the company will own the majority of the tokens and the voting rights.

- Low float, massive supply pressure - Because only 2880 tokens are being released per day, but 10,000,000 tokens exist and almost 2.4 million tokens are unlocked and owned by early stage equity holders, this creates a dynamic where the low float causes huge swings in price, but will eventually be met with massive sell pressure and a lack of a buyers.

- Growth completely driven by unsustainable arbitrage - To earn COMP tokens, you must borrow or lend, which becomes attractive even at unattractive rates as long as the COMP price goes higher. To date, COMP has benefited from positive reflexivity: as the COMP market price appreciates, the value of the subsidy increases, driving in more liquidity and ultimately boosting protocol earnings. At the same time, Compound is also exposed to negative reflexivity: if the COMP price falls, the subsidy value decreases, causing liquidity to flow out, driving the price of COMP down further. With Uniswap currently the primary secondary market and such a small percentage of total supply circulating, it does not seem unlikely that this scenario could arise, especially as lenders and borrowers begin to realize gains on their COMP holdings.

- Misleading narrative - The “Market cap” at a price of $300/token = $3 billion, fully diluted. However, with only a handful (~10,000 to date) of the tokens actually in the public domain, the market cap is a bit misleading, and is being perpetuated further by the Compound team itself in marketing materials. This seems a bit noncompliant.

- Non-transparent unlocks / vesting - There are various levels of information regarding when the team and early-stage equity investor tokens can unlock and be sold. In general, lack of full disclosure and transparency leads to greater risk and uncertainty.

- Massive leverage - We are in uncharted territory with regard to how much leverage is being used to “farm” these COMP tokens.

- Coinbase listing - Seems incredibly premature given the low float and insane price moves, fueling fire for why Coinbase would list this token so quickly considering no one even owns it yet.

At the end of the day, this was a raging success for Compound, digital asset investors, and the growth and evolution of this space. We talked last week about how the term “cryptocurrency” is largely a misnomer, and is being replaced by value investing where tokens can be modeled financially and usage is understood, and the COMP token exemplifies this transition further. That said, there will still be growing pains in this process. The reward seems appropriate for the level of risk, but make no mistake about it, there are plenty of risks.

Given all that is happening in the debt and equity markets, and all of the pivots that happen with technology companies, it is refreshing to see innovation with regard to investor and user participation. We applaud the optionality of backing a company with uncertain but promising investor protections and value propositions, instead of locking into “certainty” way too early.

Notable Movers and Shakers

For those that use Bitcoin as a barometer for the Digital Asset market, last week would seem to be mellow: Bitcoin was flat, and Bitcoin dominance was also flat. A closer inspection of the market would yield a much different conclusion, with the top 100 assets by market cap having a wide distribution (25+ finished 10%+, 50+ finished 5%+, 60+ outperformed Bitcoin). The sector rally in DeFi raged on this week, with one other notable mover:

- Decentralized Finance (DeFi) continues to defy Newton’s Third Law of Motion - COMP (+375%), LEND (+87%), MLN (+74%), NEXO (+48%), CEL (+24%), SNX (+22%), and REN (+14%) all posted significant gains independent of the market.

- Chiliz (CHZ) had their Fan Token Offering (FTO) for FC Barcelona ($BAR) tokens (announced on Tuesday), and token holders were prepared. The new FTO was meant to be offered for up to 48 hours, but sold out in under 2 minutes (faster than the time it took to write this paragraph). This was the 7th FTO held on the Socios platform, with FC Barcelona joining the likes of Juventus, Paris Saint-Germain, Atlético Madrid and more, with UFC and e-sports tokens on the way next. These token offerings can only be purchased using the native $CHZ token, which was evident in the price action last week (+22%). For more information on the $BAR token offering, read here and here.

What We’re Reading this Week

In a report by two JP Morgan strategists, it was reported that Bitcoin successfully passed its first “stress test” during March’s global selloff. According to the strategists, Bitcoin has traded closely to its intrinsic value, that is the cost to mine it, outperforming every other asset class. In addition, they also noted that despite the flight to quality across all asset classes, including digital assets, the market structure for digital assets was “more resilient” than FX, equities, treasuries and gold. The strategists concluded that Bitcoin proved its “longevity as an asset class” although it had not yet proved itself to be a store of value. Although we disagree with the evaluation of Bitcoin’s safe haven status, it’s encouraging that JP Morgan, which has traditionally been negative on digital assets, is reconsidering its stance.

Last week, Japanese Bank Nomura in partnership with Ledger and CoinShares, launched a digital asset custodian Komainu. Komainu will offer custody services similar to other traditional financial service companies such as Fidelity and the Intercontinental Exchange (ICE), supporting only clients and digital assets that have passed AML checks. Nomura has long been focused on the growing digital assets space with the hope that one day traditional bonds and stocks will be digitized, reducing back office costs.

Findings of a Deloitte survey released last week showed that about 40% of surveyed firms (up from 23% in 2019) had already implemented some form of blockchain technology to improve their processes, however, challenges remain around broader implementation. In addition, the survey found that for 55% of firms, blockchain is one of the top five strategic priorities for organizations and 82% of firms are hiring for blockchain expertise in the next 12 months. Deloitte’s global and US blockchain leader Linda Pawczuk said, “while blockchain was once classified as a technology experiment, it now represents a true agent of change”.

In today’s digital world where news is reported from a variety of sources, false information and doctored images have risen, leaving journalists to puzzle out truth from misinformation. The News Provenance Project, created by the New York Times and IBM, aims to track the lifecycle of photos online. Using blockchain technology, the project captures and tracks how photos are taken, shared, edited and captioned across social media platforms. The goal is to help readers understand the origins of images they see online and track how they have evolved from their original incarnation. Despite a promising prototype, it was noted that there are many hurdles to rolling this technology out at larger scale.

And That’s Our Two Satoshis!

Thanks for reading everyone!

Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA - Chief Investment Officer

Katie Talati - Head of Research

Hassan Bassiri, CFA - PM / Analyst

Sasha Fleyshman - Trader

Wes Hansen - Head of Trading & Operations

To learn more or talk to us about investing in digital assets and cryptocurrency