What happened this week in the Crypto markets?

The Best Defense is a Good Offense

Risk assets got a boost from better-than-expected economic data (strong jobs report) and the Fed's decision to keep rates unchanged until their inflation metrics match what the rest of us feel every day. With this backdrop, US stocks continue to reach new highs. Bank of America (and Zerohedge) pointed out just how ridiculous the speed of this reversal has been:

But Arca’s own David Nage pointed out how manufactured this equity rally has really been. U.S. companies have purchased $272B of their own shares so far this year, on pace to break 2018's record $1.085T. Meanwhile, stock funds have seen $4B of outflows so far in 2019, surpassing the $2.9B of outflows for all of ‘18 when the S&P 500 fell by 6%.

The rally in crypto continued last week as well, with Bitcoin once again leading the pack, gaining another 8% week-over-week, pushing YTD returns over 50%. But unlike the swift and uncharacteristic equity rally, Bitcoin is rallying due to real buying pressure from new participants. Trading Volumes are skyrocketing, and Bitcoin transaction volumes are increasing as well.

Bitcoin Volumes are Increasing

Source: Coincheckup

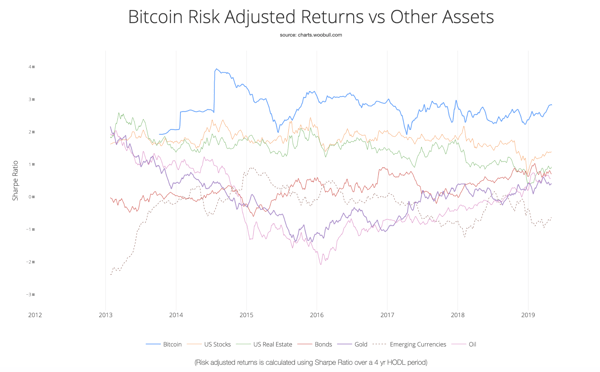

Moreover, while we caution against using Bitcoin (BTC) as a proxy for the entire crypto asset class, the risk-adjusted returns of owning Bitcoin have outpaced that of the longest and least volatile equity market rally in decades.

Source: WooBull Charts

Here Come the Incumbents

It’s important to remember that Crypto is an asset class, and Bitcoin is just one component of this asset class, albeit an outsized one. Comparing the entire S&P 500 to Bitcoin is not a fair comparison, just as it would not be fair to compare a diversified investment portfolio to Apple (AAPL). That said, for the time being, Bitcoin drives the entire crypto narrative, and unlike the headwinds facing other risk assets (as exemplified by the 2-5% selloff driven by Trump’s China tariff talk Sunday night), Bitcoin has a strong wind at its back. Look no further than the infrastructure being built around the crypto market.

Fresh off the heels of Bakkt raising money at a $700mm valuation, ErisX announced the launch of their institutional-grade spot trading product last week. Additionally, there is speculation that Etrade is launching Bitcoin products, and TD Ameritrade is in the mix as well. While Bakkt and ErisX focus on the institutional market, Etrade and TD Ameritrade are focused on the large and growing retail market. Etrade for example already has 5 million users with more than $10B in capital. As our friends at Wave Financial put it, “Every step like this makes it easier for money to flow into the cryptocurrency ecosystem, which makes it more likely that the next market bull will be stronger and more pronounced.”

Sell in May, Go Away… To Crypto

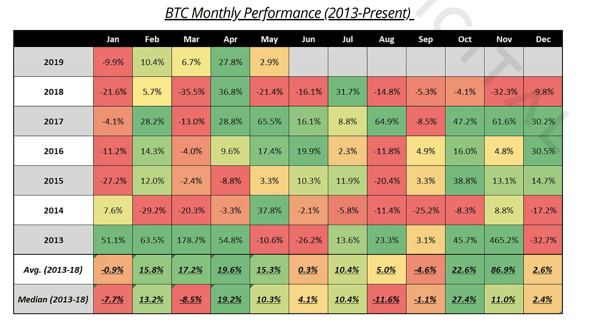

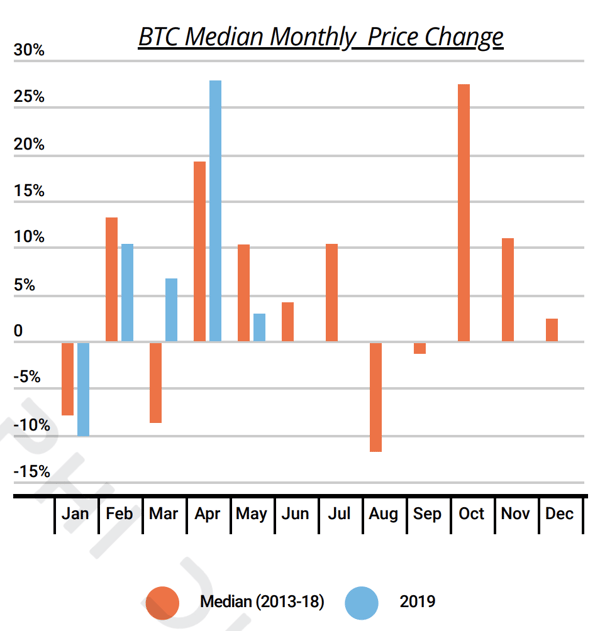

The popular Wall Street motto is once again gaining steam, after an impressive 17% gain in stocks through April. In Crypto, it’s far more likely that people will buy in May. With history as our guide, May has been a historically strong month for Bitcoin prices.

It’s unlikely that this type of focus and investment would be happening if these large financial incumbents thought the rally was ending any time soon.

The Bitfinex Bailout isn’t a Bailout - it’s Brilliant

We’ve come this far without mentioning the elephant in the room. Those already in the crypto ecosystem have undoubtedly been following the Bitfinex / Tether saga for the past few weeks. For those who have not followed it, The Block has done an amazing job covering it, but here’s a 30-second recap:

The New York State Attorney General (NYSAG) is suing Bitfinex, one of the largest and oldest cryptocurrency exchanges, and affiliated firm Tether, the company behind the stablecoin of the same name (Ticker: USDT). In a situation that should have you reaching for your Glass-Steagall history books, let’s summarize by saying $850mm was misappropriated, Tether is now only 74% backed by US dollars (instead of 100%), and Bitfinex has a major capital shortfall. To plug this capital hole, Bitfinex is attempting to issue $1 billion of new tokens (LEO) in exchange for $1 billion of Tether tokens (USDT), whereby Bitfinex will effectively burn the incoming USDT to make up for the shortfall.

- MF Global failed to raise capital; filed for bankruptcy.

- Jefferies and Knight were able to sell equity; both the companies and shareholders were rewarded.

Many crypto market participants (with no capital markets experience or historical context mind you) are calling this a bailout. We disagree. Bear Stearns and Merrill Lynch were bailouts, because taxpayers had no choice as bank suitors were forced to purchase. And the TARP program was a bailout as the government chose to keep bad business models alive. But Jefferies and Knight Capital were not bailed out - they were saved by real investors who believed in the future prospects of the company once the capital hole was plugged.

Back to Bitfinex: shady business practices aside, this is a brilliant solution for Bitfinex and showcases the unique and flexible characteristics of issuing tokens instead of equity or debt. This token will have equity-like features (“dividends” based on revenue growth), debt-like features (auto-paydowns with FCF and recovered assets) and utility features (reduced trading fees on a widely utilized platform).

A bailout is a forced transaction -- this is not forced. This is free capital markets at their finest, where the market gets to decide the now binary fate of a crypto Exchange.

- If Bitfinex successfully raises this capital, and all signs thus far point to them succeeding, investors in these new LEO tokens will likely be rewarded in the same way Jefferies and Knight investors were, as the terms of these new LEO tokens are incredibly favorable for investors. With the capital hole filled, Bitfinex and Tether will likely continue to operate with a well deserved reputational blackeye.

- If the Bitfinex token issue fails, then the market has spoken, either indicating that the terms of this sweetheart deal are not sweet enough, or indicating that deceitful actions such as fund misappropriation cannot simply be undone with fresh capital.

By no means does this excuse Bitfinex or Tether for their actions, no more than Knight should be excused for an inexcusable $500mm fat-finger loss, or Jefferies should be excused for loading up on Sovereign CDS as if they were AAA-rated debt. And we understand that there are a lot of people who want this to fail, in order to help remove an unregulated exchange and a loosely regulated stabletoken. But it’s simply a reality that people move on from scandals, and companies who remain solvent get to continue operating. Bitfinex moral opinions aside, this is a win for crypto, a win for free markets, and a win for the flexibility of token structures.

Notable Movers and Shakers

Last week was dominated by Bitcoin (+8%) - only 15 of the top 100 projects outperformed “digital gold” on a week-over-week timeframe. Nonetheless, certain projects were able to escape Bitcoin’s long shadow:

- Cosmos (ATOM) finished the week up 14%, mainly driven by a successful (and well anticipated) launch in mid-March coupled with a listing on Binance. Investor confidence remains remarkably strong for this nascent project.

- Horizen (ZEN) was the best performing token in the top 100 last week (+27%). While there were no fundamental news or updates, it could be hypothesized that Grayscale Investments’ latest television commerical brought their Single-Asset Trusts to the forefront of discussions, of which Horizen is one of 8 other digital assets. Also, it’s worth noting that in the last week, Grayscale injected nearly half a million dollars into the ZEN Trust (from $2.6M to $3.0M).

- Bitcoin Cash (BCH) posted impressive gains (+13%) last week, likely in anticipation of their May 15th network upgrade, which contains the implementation of Schnorr signatures, a privacy enhancement feature to its blockchain.

- Basic Attention Token (BAT) ended the week down 13%. After running up with strength since the end of February, this correction was inevitable. What remains to be seen is whether or not this correction was just the market breathing, or if this was a knee-jerk reaction to the news swirling around Facebook’s entrance into the digital asset space, with their tokenization model seemingly acting as a competitor towards BAT.

What We’re Reading this Week

According to the Wall Street Journal, Facebook is seeking up to $1b in funding for its crypto-based payments initiative. The project, code-named “Project Libra”, aims to allow users to send and spend the tokens on the Facebook platform with the potential for broader distribution across e-commerce channels. Reportedly, Facebook has spoken with Visa, Mastercard and First Data Corp. for funding.

Spencer Bogart of Blockchain Capital dissects his firm’s recent survey results on Bitcoin sentiment among the American population. Encouraging for those of us in the industry, the survey found that “despite the bear market, the data shows that Bitcoin awareness, familiarity, perception, conviction, propensity to purchase and ownership all increased/improved significantly”. Unsurprisingly, the survey shows that the younger generation is leading the pack in all categories studied.

The AML report highlights the still present negative risks within the crypto ecosystem. The findings conclude that $1.2b was lost in the first quarter of 2019 due to theft, scams, and fraud. This figure includes the losses from QuadrigaCX and Bitfinex/Tether. The report concludes that the massive uptick crypto crime will bring about a new wave of regulation to prevent these crimes from happening in the future.

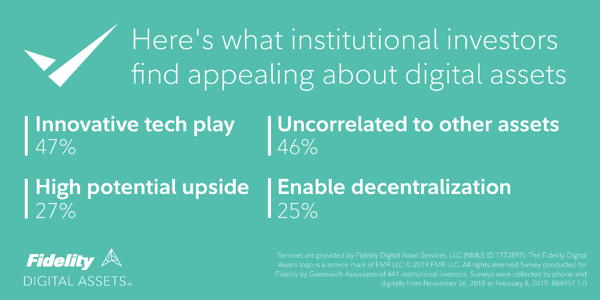

A survey from Fidelity Investments has found that institutional investments are likely to increase over the next 5 years. Although the exact findings of the survey have not been widely released, some high-level findings include that seven in ten respondents cited certain characteristics of digital assets as appealing. We’re excited to see this increase in institutional investor interest as the digital assets space develops.

Last week, Grayscale Investments launched their “Drop Gold” advertisement encouraging individuals to ditch their gold investments and buy Bitcoin (through Grayscale’s Bitcoin Investment Trust - GBTC). GBTC is a listed exchange product, but investors pay a premium to the price of Bitcoin. The World Gold Council issued a response titled “Cryptocurrencies are no replacement for gold”, pointing out gold’s advantages over digital assets.

Consumers are increasingly turning to known platforms like Square as on-ramps to crypto. The company reported over $65m in Bitcoin revenue for Q1, a 25% increase from the previous quarter. Users can purchase Bitcoin through Square’s Cash app which is available to anyone in the US. Despite the increase, Bitcoin sales only account for roughly 10% of the company’s quarterly revenue.

And That’s Our Two Satoshis!

Thanks for reading everyone! Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA - Chief Investment Officer

Katie Talati - Head of Research

Hassan Bassiri, CFA - PM / Analyst

Sasha Fleyshman - Trader

To learn more or talk to us about investing in digital assets and cryptocurrency

call us now at (424) 289-8068.

.jpg)