What happened this week in the Crypto markets?

How Crypto Fairs During a Stock “Melt Up”

Stock and bond investors had political headlines, corporate earnings, and economic data to chew on last week, and none of this seemed to matter in any material way. The narrative around a “melt up” is beginning to take hold. From our friends at Cantor Fitzgerald:

Melt ups are always possible when markets ignore reality and trade on false narratives, just as small caps did in mid-2018 on a “trade-safety narrative” or just as EM stocks rallied in 2017. Melt ups are typically a product of a fear of missing out (FOMO). In this case, U.S. equities are disregarding the rollover in earnings, the continued global economic slowdown, and the fact that central banks are in fact far less accommodative overall. Moreover, equity markets appear to be trading (wrongly) on the perception the Fed is ready to cut imminently. The Fed’s balance sheet continues to shrink, and the ECB is no longer growing its balance sheet (other than on reinvestment). The Fed just completed 9 hikes to 2.5% after seven years at zero! The absence of a hike in 2019 is not the same as cut, which is unlikely versus market expectations at ~40%. If equities are to move higher, it will require multiple expansion we just don’t think is in the cards. Should a melt up occur, market performance will eventually revert to fundamentals in an even more pronounced fashion if/when a FOMO melt up is done.

FOMO is a term that floats around in crypto as well, especially following the 25% “rip your face off” rally on April 1st that caught many would be buyers flat-footed. That kind of knee-jerk move makes those who aren’t invested panic, and leaves those who are invested feel like they don’t own quite enough. As a result, buying the dip is all but a forgone conclusion right now, which usually means the dips will never happen. This sentiment can of course change on a dime, but for now, the macro backdrop continues to be favorable for crypto assets and risk assets in general.

That said, crypto was incredibly boring last week with most major assets moving in a tight range, while other alt-coins slowly began to decouple (with some performing very well while others were taking to the woodshed).

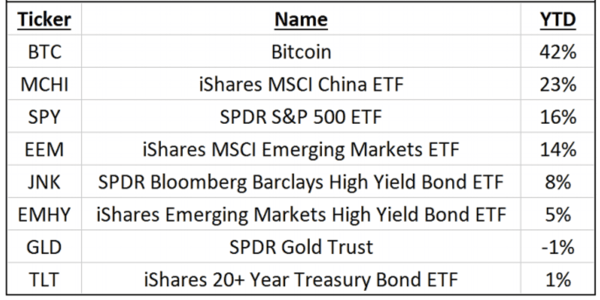

Year-to-date price change by asset class

Three Noteworthy Crypto-Specific Events That May Have Long-Term Implications

Despite the slow week, there were three events last week which investors need to take notice of. One of these was a heavy focus of crypto Twitter and the media, while the other two went largely unnoticed.

1) The delisting of Bitcoin Satoshi Vision (BSV):

Binance is without a doubt the most influential player in crypto currently and they once again made their presence felt last week. The exchange decided to de-list Bitcoin Satoshi Vision (BSV) from trading on their exchange due to the erratic behavior of its controversial founder. Shortly after, other prominent exchanges such as Kraken and ShapeShift followed suit, which naturally triggered a wave of selling pressure. Some argue that it demonstrates an industry immaturity that will turn off investors due to the ad hoc delisting, while others see it as a community defending its values. Further, Nathanial Whitmore and Ari Paul discuss whether or not this is a form of censorship. Regardless, the obvious conclusion is that Centralized Exchanges still hold way too much power in crypto.

A less obvious, and emotionally-detached analysis would focus on why this matters at all? Stocks get delisted all the time according to very specific rules laid out ahead of time (failure to meet reporting requirements, volume declines, etc). But when a stock gets delisted, it can of course still trade broker-to-broker (for example, on the pink sheets). As a result, the stock can retain value, and the only value lost is the value that was solely attributed to liquidity.

BSV is meant to be a form of money. As with all digital assets right now, the primary use case is being drowned out by the allure of short-term trading profits. But if BSV truly has value as a peer-to-peer form of money, the adoption of BSV by merchants, consumers and wealth accumulators will ultimately matter much more than the ability to trade this for another digital asset on an exchange. With BSV falling 22%, this alone doesn’t describe a death-blow, but rather a liquidity premium being drained out. That said, if there is no real use case, then this may be just the beginning. It’s very difficult to “kill” digital assets -- but this may be the best way to expose them.

2) Ocean Protocol Cancels, Shifts, and Retries its offering

Ocean Protocol was one of the first major ICO attempts to test the waters in 2019 after the SEC basically shut down the fire hose in November 2018 with a series of enforcement actions and strict guidelines for digital asset issuance and trading. Its success, or failure, would seemingly have major implications for the future of this form of capital raise. Alas, both happened.

We discussed IEOs a few weeks ago, where Exchanges with large distribution networks take over the underwriting of token sales. Ocean Protocol, after failing to raise funds on its own via CoinList, has now gone the IEO route, looking to sell tokens via Bittrex International’s Exchange platform at half the price of the initial ICO price. This might be more of a poor reflection on CoinList than the ICO market itself, but the Ocean Protocol founder said himself “the U.S. is not the best environment for this kind of fundraising right now” upon reflection of the disappointing token sale. This realistically means that ICOs going forward will not be accessible to U.S. investors. So we’re back to square one in the U.S., where the uniqueness of crowd-sourced token investments are lost, and only Accredited Investors will be able to find hot deals based on word of mouth. The SEC’s stated mandate is to protect retail investors, which they have done. But there is a fine line between protection and being stifling.

3) Bring Out Your Dead - Here come the Hung Deals!

Frequent readers know that we often compare crypto to the high yield bond market and emerging markets, as everything from OTC trading, to fake volumes, to violent illiquid price moves is comparable. One of my favorite soap operas in high yield is when large investment banks get “hung” on bought deals (typically LBOs or CLO financings), and then sit on the inventory for months until the markets thaw, allowing the banks to slowly bleed the overpriced debt out to investors, often at a large loss. This is about to happen in crypto; albeit the losers will not be the banks, but the investors themselves.

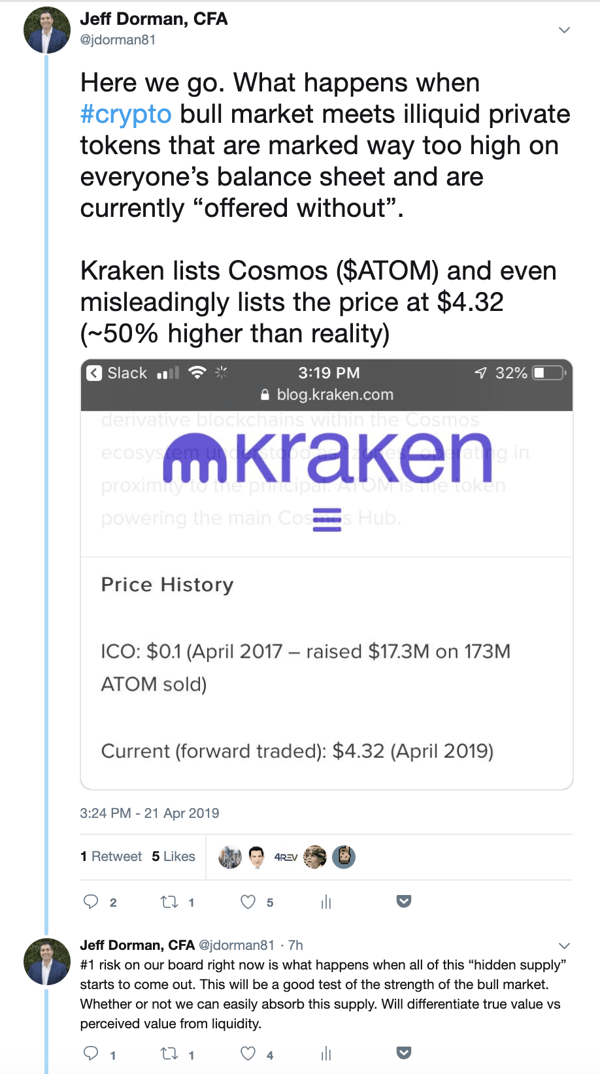

Kraken just announced that they will be listing Cosmos (ATOM) tokens. For those not familiar, Cosmos is one of hundreds of ICOs from 2017 and 2018 that still hasn’t been listed on any exchanges, and is largely owned by hedge funds. Given the swift decline in crypto assets from December 2017 to January 2019, your guess is as good as anyone’s with regard to how many of these token holders are still in business, and where these assets are marked (paging valuation committees). So naturally, investors and OTC dealers get to have fun with the lack of transparency, much like in high yield and emerging markets where dealers quote prices on illiquid assets that are typically nowhere near where a real buyer or seller could actually transact. The quoted price helps bring buyers and sellers to the table, but they are often seated miles apart.

ATOM is being quoted in the $4-5 range, even though just about every hedge fund has been shown offers below $3 by sellers who need liquidity. Kraken even published a $4.32 quote on their blog. Cosmos is viewed as one of the better projects to come out of crypto in the past few years, so this may be the right time to strike given the current exuberance of crypto investors following this year’s large gains. But this will be a true test of the market’s willingness to absorb supply.

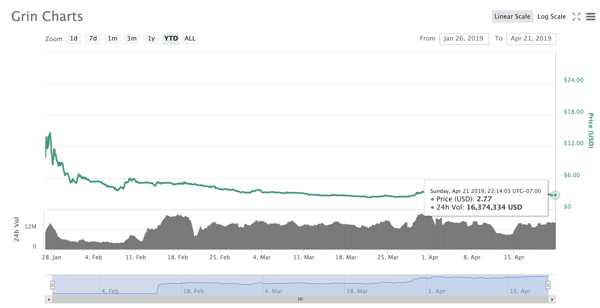

We’ve already seen this play out once this year. Grin (GRIN) began “trading” in the grey markets earlier this year, with many OTC dealers pretending it was trading near $20 (maybe it was actually trading there in a few negotiated transactions between existing investors who were incentivized to walk the price up, but this certainly didn’t reflect reality). Within hours after being listed on exchanges, GRIN fell to $14 and ultimately settled below $3.

Let’s hope the market makers and investors in Cosmos have a more realistic goal, and allow Cosmos to find a market clearing price in a less crushing fashion.

Price Collapse of Grin after Trading Began on Exchanges

Source: CoinMarketCap

Notable Movers and Shakers

Bitcoin held relatively stable last week. Meanwhile, many other tokens (alt-coins) moved in larger strides in both directions. There were, however, a few tokens that offered isolated movements:

- Bitcoin Satoshi Vision (BSV) dropped 22% early last week after Binance announced it would be delisting the cryptocurrency within the week. Kraken put out a Twitter poll to its users to determine if they should also delist (71% voted to delist). As the major liquidity sources for BSV disappear, we may see the end of this token’s dominance.

- Binance Coin (BNB) soared 20% last week following the Thursday launch of their Decentralized Exchange mainnet. The launch was not without controversy as some inside sources claim that the exchange is using its dominance in the space to push projects to migrate to its chain from Ethereum.

- Basic Attention Token (BAT) rallied 37% last week in anticipation of their MVP, Brave Browser, receiving a large update. This update will allow users to monetize their attention by opting into advertisements, receiving BAT tokens in return.

- Monacoin (MONA) gained 73% at the tail end of last week, with strong buy side interest in Japan. As noted on Twitter, Monacoin is in a unique position, being traded versus fiat (JPY) in a legally friendly environment of Japan. It is worth noting that MONA traded at a premium in Japan for most of the rally, with prices consolidating towards the end of the week.

What We’re Reading this Week

The big news last week was that Harvard purchased cryptocurrency in Blockstack’s token sale according to Blockstack’s regulatory filings. This is considered the first time that an endowment has participated directly in a token sale, as most of these funds have historically only invested in Bitcoin and Ethereum directly. In addition to signalling a bullish outlook for crypto, it also signifies that Harvard was comfortable with the regulations and custody procedures for holding these tokens.

Spencer Bogart of Blockchain Capital discusses the importance of crypto on-ramps, such as Facebook (with its potential to onboard millions), to aid in mainstream crypto adoption. If the on-ramps into the ecosystem are simple, seamless and through a familiar means, users are far more likely to explore further and remain within the ecosystem based on other projects they discover. The Arca team touched on something similar regarding JP Morgan Coin last month.

Audit firm Ernst and Young released a beta version of their free software, Nightfall, which allows businesses to assess Ethereum smart contracts and tokens for their own use. What’s so novel about EY’s software is that it also implements “zero-knowledge proofs” (ZKPs) which shields transaction data so the transaction can be publicly tracked, but the parties involved and the assets moved remain private. The availability of this software means businesses can utilize the security of the Ethereum blockchain but maintain the privacy necessary for their business.

The billion dollar market that makes up cryptocurrency mining, which is often overlooked for the flashier side of the business - trading, is no less important and has gone through just as many iterations in its ten year history. This article provides an overview of mining’s history, beginning with the Bitcoin whitepaper’s Proof-of-Work algorithm, the variations in mining equipment and the rise of mining pools.

Consensus, the Ethereum development studio, announced last week it would be raising $200m in its first round of financing at a valuation of $1 billion. To date, Consensus has been funded by founder Joe Lubin who was made wealthy from his early involvement in Ethereum. We’re seeing this trend occur more frequently where crypto organizations transform into real companies via traditional financing.

And That’s Our Two Satoshis!

Thanks for reading everyone! Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA - Chief Investment Officer

Katie Talati - Head of Research

Hassan Bassiri, CFA - PM / Analyst

Sasha Fleyshman - Trader

To learn more or talk to us about investing in digital assets and cryptocurrency

.jpg)

Source: Delphi Digital

Source: Delphi Digital