What happened this week in the Crypto markets?

Hidden Volatility

Needless to say, it was a challenging week for global markets, despite an unbelievable amount of government resources around the world being thrown at the problem. But there was a bright spot. Just one week ago, Bitcoin was pronounced dead, as many claimed that it clearly could no longer be a safe haven as correlations with equities temporarily spiked. So how did Bitcoin market respond? By doing what Bitcoin does… the unexpected.

|

|

Week ending 3/15/20

|

Week ending 3/22/20

|

|

S&P 500

|

-9%

|

-15%

|

|

Gold

|

-8%

|

-2%

|

|

Oil

|

-33%

|

-28%

|

|

Bitcoin

|

-34%

|

+11%

|

Source: CNBC, TradingView, CoinMarketcap

Now, Bitcoin’s move higher this past week is no more or less relevant than the sharp move lower the previous week. We will look back on this period of time in years and even decades, not days or weeks. Short-term correlations are of course spurious. Two islands can simultaneously burn without one causing or affecting the other -- and one island can put out their fire while the other island still burns.

In 2008, gold and equities initially sold off in tandem, before gold ultimately decoupled and rebounded sharply in November. From our friends at Kraken:

“In 2008, we witnessed virtually every asset class get chopped-up right out the gate as market participants flocked to cash. Gold fell as much as -17% by the end of 3Q 2008 before catching a bid and rallying into year end. Gold ended up closing out 2008 up +3% before then heading off to the races and outperforming several other assets in the years that followed. Although that's not to say that crypto and/or bitcoin will follow the same trend, it's worth drawing attention to the fact that markets can stay irrational up until they can't any longer. Also, don't forget that in a liquidity event, a market like crypto, which has a market capitalization of less than $200B and is rather illiquid due to coins either being in storage or lost for good, is susceptible to getting chomped up and spit out.”

Graph of Gold vs other asset classes in 2008 / 2009 (Indexed from 0)

Given the speed of the equity, credit and oil collapse, it would not be shocking if certain asset classes emerge from the wreckage relatively unscathed when all is said and done. Safe haven can mean many things - in fact quite literally “safe haven” means “a place of refuge”. We do not yet know how Bitcoin or any other asset class will ultimately respond to these market conditions. But what we do know is that the constant manipulation of equity and credit markets lulled investors to sleep, whereas the free crypto markets (despite all of their flaws) have at least prepared investors for what was possible.

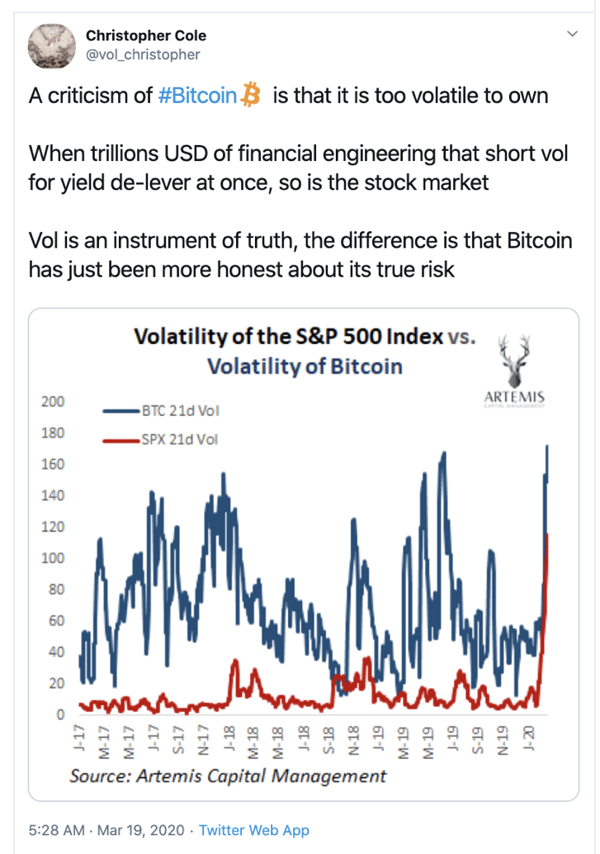

Christopher Cole of Artemis Capital is one of the world’s top authorities when it comes to volatility. As he points out, hidden and suppressed risks are still risks.

Bitcoin is a Wolf; Traditional Markets are Domesticated Dogs

Infinite rate cuts. Unlimited repo facilities. Commercial Paper facilities. Fully backstopped money markets. Bans on short selling. Helicopter money sent directly to individuals. Industry bailouts. The Fed, the ECB, the BOJ and central banks around the world are rapidly firing their bazookas, and each headline seems more insane than the last. Billion dollar solutions are almost immediately insufficient, and must therefore be trumped by Trillion dollar solutions. And now the ECB and the Fed are explicitly ending any doubt altogether -- the ECB has said “There are no limits” and Federal Reserve members said “There is an infinite amount of cash".

This is quite literally why Bitcoin was invented.

Bitcoin sold off earlier this month during a liquidity crisis, as everything that could be sold for US dollars was liquidated. But if this liquidity crisis turns into a solvency crisis, the game changes completely. Our friends at Anchorage put it best.

“It is also worth remembering, in this time of crisis, that Bitcoin literally has ‘crisis’ written into its base code. Bitcoin was born from and intended for times of crisis, and today’s pandemic — and the reactions of the central banks around it — may be the proving ground for one of its implicit theses: that Bitcoin is an inflation hedge.

It is important to note that, on Thursday, blocks were still being produced, onchain transactions were still taking place, and the network was fully functional. With no need for circuit breakers or market halts, the network was working. The market did not close, while futures gave investors — who could only wait for a violent move at the open — the shakes. And it did not have to bet on when a central bank might come in to “rescue” the markets, or what shape that rescue might take. The BTC network just kept producing blocks. All price action aside, it worked like it was supposed to, and that is a huge win for Bitcoin. While the traditional markets figure out how to de-lever, and choose which industries and companies to bail out, Bitcoin, it seems, will continue operating as it was originally coded, block after block after block.”

We can’t underscore this sentiment enough. While the headlines focus on Bitcoin’s volatile price action, there is another world out there where Bitcoin owners only care about one thing -- it works great without intervention. Their Bitcoin still exists, and it can still be used. While the traditional financial system is buckling even amidst record injections, bailouts, regulations and stimulus, Bitcoin is trading and transacting uninterrupted. It is working just as designed. There is of course no guarantee that Bitcoin’s price will react favorably, as many (including Arca) believe. But there is no doubt that Bitcoin is functioning better than traditional financial markets right now.

Bitcoin truly is a wolf in the wild; fully adapted to the unstable conditions surrounding it, while stock markets and bond markets around the world are acting like domesticated dogs, waiting helplessly for their masters to ensure their survival.

We Don’t Believe Digital Assets Will Be Affected By a Recession

There are big differences between how Bitcoin, gold, equities and credit have sold off in March, albeit this is quite subjective. Gold, for the most part, is being sold due to forced liquidations and margin calls. Credit is being sold due to rising risks of defaults as cash flows evaporate. Equities are being sold because they are incredibly overvalued amidst cratering earnings expectations and investors have thrown in the towel after a decade of false comfort. Meanwhile, digital assets have mostly been sold by those who simply believe they will be able to buy them back at lower prices.

The different value-drivers between equity, debt and digital assets may begin to manifest from this. All three are arguably part of the new "cap structure", but with very different "values".

Debt = Claim on assets

Equity = Claim on profits and cash flows

Tokens = Claim on Future Services / Customer growth

Tokens issued by companies and projects are like gift cards - they speed up revenue recognition (booked upfront),but create a liability of services and products offered in the future. This is similar to airline miles, where customers earn them (or buy them), which then creates a future service liability for the airline. Digital assets also allow companies and projects to pre-fund themselves via their community engagement tokens, thereby creating a service liability in the form of how the token is redeemed in the future (for discounts on services rendered, or in some cases, direct claims on future revenue).

Global quarantine is simultaneously causing both demand shocks (lack of customers, job losses) and supply shocks (lack of production). This is having disastrous effects on revenues and profits (destroying equity value), and asset coverage (destroying debt recovery), but apparently has less of an effect on customer loyalty and no effect on future service claims (which implies tokens are not losing value). While fundamentals haven't mattered in the past 10 years, they will matter in the years ahead as revenues stagnate and debt begins to impair cash flows. It’s at times like these that we’re reminded that equity and debt valuations rely on actual cash flows and hard assets, not just multiples.

Companies with public debt and equity most often rely on physical customers and physical locations, and always rely on supply chains. Conversely, most crypto companies and projects don’t have physical stores or customers or supply chains. They are the epitome of "a truly digital world". From trading exchanges, to video games and virtual worlds, to Decentralized Finance and Web 3.0 - the shift from physical to digital is happening, and COVID-19 has simply accelerated it. As a result, most of these digital projects and companies are not subject to demand shocks (quarantined customers) or supply shocks (lost production). Just like your Delta SkyMiles and Target gift cards don’t go away or lose value during an economic crisis, neither do the intrinsic value of digital assets. These tokens are claims on future services, not claims on revenue, profit, or assets. They are essentially immune to supply and demand shocks, even if prices in the near-term are not. One might even say they are recession proof.

Crypto prices may of course still go lower. After all, risk is risk. But value is not actually being destroyed from digital assets like it is from stocks and bonds. You could certainly argue that digital assets are overvalued, but not because of what has transpired over the past 6 weeks.

Notable Movers and Shakers

From the ashes of last week’s carnage came the phoenix - Bitcoin surged as distressed investors took advantage of capitulation. The rest of the market rallied alongside Bitcoin, albeit with a dampened effect (BTC.D up 2%); only BCH and BSV outgained BTC from the Top 10. For the first time in a few weeks, there were idiosyncratic events that led to alpha in the market:

- Maker (MKR) held a debt auction in an effort to recapitalize the ecosystem following last week’s “Black Thursday”, in which Maker DAO liquidations resulted in losses throughout the network. The auction was successful (although with peering eyes), with volume pouring into MKR both on and off exchange. With distressed investors backing Maker, confidence seems to have been restored (or at least stabilized), which reflected in price action (+23%).

- Steem (STEEM) rallied hard last week after it was announced that the community and developers alike had decided to hard fork the blockchain, minting new HIVE tokens at a 1:1 rate (excluding Steem.it/Justin Sun’s portion of the STEEM tokens). The project has been in the spotlight as of late after their public dispute with Justin Sun (Tron CEO/Founder), who was attempting to assimilate STEEM into the TRX ecosystem (at first respectfully, and then maliciously). It seems the market supported the community’s bid for autonomy, as the token rallied as much as 295% before finishing the week up 15%.

What We’re Reading this Week

In a note from CZ, CEO of digital asset exchange Binance, the executive provides insight into the question everyone has asked this week: is Bitcoin truly a safe haven asset after last week’s sell-off? that caused the sell-off but reaffirms that the fundamentals for Bitcoin and Bitcoin inflation-resistant monetary base has not changed. Indeed, its fixed supply has become even more important as central banks around the world continue to print money to deal with the economic crisis they face.

Bakkt, the exchange backed by the Intercontinental Exchange (ICE), announced last week that it raised a $300m Series B from Pantera, Microsoft’s M12, PayU, Boston Consulting Group, Goldfinch Partners, CMT Digital, and ICE. After spending the last year launching a regulated options and futures market, the exchange recently announced that it would be focusing on retail clients with an app expected to launch in the summer. The move to focus on retail also makes sense given their February acquisition of Bridge2 Solutions, a loyalty services provider. With this acquisition and new app, Bakkt hopes to create a digital goods exchange for loyalty points and rewards, an area ripe for tokenization.

Last week, Coinbase’s Chief Legal Officer, Brian Brooks, resigned from his role at Coinbase to join the Office of the Comptroller of the Currency (OCC), the independent banking regulator for the US. What is more surprising is that Treasury Secretary and crypto skeptic, Steve Mnuchin, appointed Brooks to the position. Coinbase along with many others in the crypto community believe that Brooks will bring a crypto-friendly perspective with him to the OCC.

After 11 months of research, Toyota has unveiled its blockchain lab which has spent almost the last year researching blockchain technology’s capabilities for the car company. With the conclusion of its research, Toyota now wants to accelerate incorporation of blockchain. Toyota has use cases for the technology in areas such as supply chain, vehicle registration, and digitizing financing options.

And That’s Our Two Satoshis!

Thanks for reading everyone!

Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA - Chief Investment Officer

Katie Talati - Head of Research

Hassan Bassiri, CFA - PM / Analyst

Sasha Fleyshman - Trader

Wes Hansen - Head of Trading & Operations

To learn more or talk to us about investing in digital assets and cryptocurrency

.jpg)