What happened this week in the Crypto markets?

The Crypto “Loser” Rally

Digital asset price performance has been nothing short of spectacular thus far in January, though admittedly it’s a bit early to celebrate. After another strong week (BTC +5% / Crypto Indices +8-15%), Bitcoin is now on pace for its best January since 2013 (currently +18%), while many other large-cap digital assets are already up 50-100% YTD.

This is a double-edged sword.

On the plus-side, it reminds us of the genesis of 2017's historic climb. At first, Bitcoin and Ethereum were making sustainable w-o-w gains, but then ICO's began to enter the space at a staggering rate (with even more staggering raises). Many of these new crypto projects saw their tokens rise 10x in a week, often on questionable news and suspect “partnerships”, and Bitcoin underperformed the space pretty significantly for a short while. Yet, when Bitcoin picked up steam in the latter half of the year, investors began to rotate back into Bitcoin, as the allure of the shiny new toys wore off. While the dynamics have certainly changed in 2020 compared to 2017 (ICO's are a thing of the past and the amount of people eyeing Bitcoin is magnitudes higher), this nonetheless feels similar. The Bitcoin halving is rapidly approaching (May 2020), and we may be gearing up for a crypto market that leaves all naysayers wondering what just happened.

On the negative side, this crypto rally may not be the best thing for the industry. When every project rushes to throw press releases and Medium posts out just to create artificial double-digit moves in their tokens, it certainly doesn’t feel sustainable nor does it remove skepticism.

Take Augur (REP) for example. Augur is a decentralized betting platform that basically no one uses, and is the leader in the crypto clubhouse for “highest ratio of hype versus people actually using it”. Last January 2019, the REP token surged over 100% in a matter of weeks because of a partnership with a company called Veil… the token then fell 50% over the next week and ended 2019 in negative territory (and by the way, 6 months later, Veil was out of business). One year later to the day, this past week, REP gained 100% in a week again, this time on anticipation of its V2 platform launch. Already at the time of writing this, the token has fallen 33% from its intra-week peak.

Augur is just one example, but the majority of YTD “winners” thus far are assets that were last year's biggest losers. As we mentioned at the end of last year, there were clear themes that emerged in 2019, which led to a very bifurcated return set where a few big winners trumped many more big losers. It's doubtful that investor opinion of these sectors/projects has changed much in the past 3 weeks, nor has the value of these projects improved. While “small cap” or “CCC” rallies are not uncommon in traditional asset classes, when all of the gains for the past 12 months come in the last 20 days, that's not typically a good sign of health, nor something that is sustainable.

Most of the YTD winners in crypto were the biggest losers from 2019

.png?width=600&name=pasted%20image%200%20(2).png)

Digital Assets Evaluation

Evaluating digital assets as an investment class based on how high prices are going during an untethered and largely unexplained rally is likely not the right way to assess progress or risk. Evaluating how low prices drop once the euphoria ends is probably more important.

The reality is, most digital assets are effectively penny stocks with regard to volume traded versus market cap. This means any token can take off at any time for little to no reason. But those that accrete actual economic value and/or show real user growth will hold gains better than others, while most everything else will either come crashing down, or considerably underperform, just like we’ve seen for the past two years.

That said, a “penny stock” rally in crypto shouldn’t invalidate the whole space. The stock market also contains over 10,000 “pink sheet” stocks, and those stocks collectively gained 30% in 2019 despite most investors ignoring them entirely. Does this mean Apple and Google and IBM aren’t real companies just because they are in the same asset class as Basic Energy Services and CreditRiskMonitor.com? Of course not. The only difference is that the size of the real companies listed on the NYSE & NASDAQ dwarf that of the pink sheet stocks, and investors have learned to largely ignore the weekly massive gains/losses of pink sheet listed companies. But for now, the “penny stocks of crypto” are still quite prominently displayed on exchanges and price aggregators, and discussed frequently in the media. Over time, the size of the real projects will dwarf and drown out the rest, and then we’ll be better equipped to filter out the noise created by the “Losers”.

There is a real industry growing here -- don’t let it be overshadowed by the worst representations.

Inflation / Debt -- Where Does This End?

Martin Luther King Day is a good time to remind everyone to be open-minded, and that everyone, regardless of color, shape, religion or net worth deserves respect, and has the right to be treated equally.

Wealth inequality is something we hear a lot about lately, which has been caused by asset prices rising more than wages, and massive inflation in critical spending areas like education and health care. Here’s a fun site to remind you how that happens, courtesy of governments around the world.

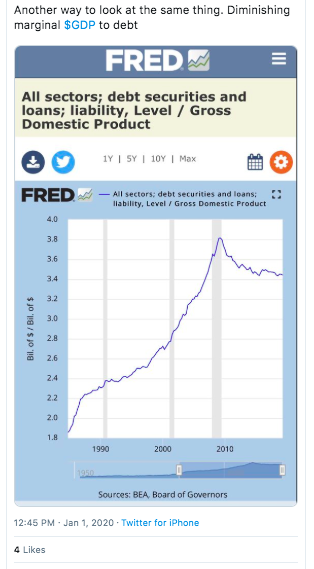

Debt, quite simply, is borrowing against your future. When used correctly and responsibly, it can create levered returns. Plenty of metrics have been developed over time to judge the quality of debt, such as interest coverage (your ability to pay interest relative to cash flow) and Debt/EBITDA (the amount of your debt relative to cash flow). Usually, the borrower is in control of his/her own ability to repay this debt and improve their own circumstances. If you choose to borrow against your future, that’s your decision. But over the past 40 years, we’ve all been asked, correction we’ve all been ordered, to borrow against our future, and we have no control at all over improving our circumstances.

Debt used to be pretty easy to understand. If you are at high risk of not paying back your debt, your interest rate rises. If you have good credit and high income, your debt will be priced at low interest rates.

But debt is now so ubiquitous that no one even cares anymore, so much so that the borrowers are actually setting their own interest rates and the lenders just say “sure”. Where does this end? It’s even worse when the lender (US Treasury) and the borrower (US Federal Reserve) are the same entity (called monetization of debt). In fact, it’s just downright scary.

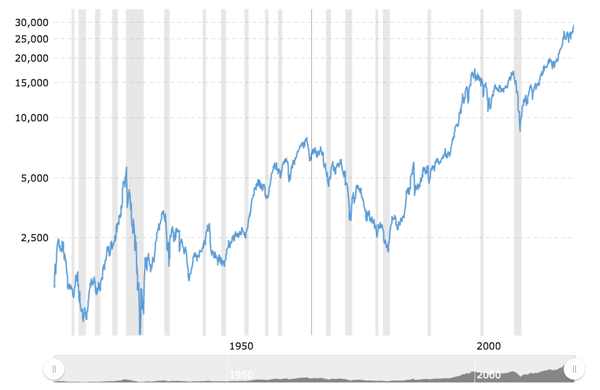

From 1916 - 1982, inflation adjusted, the US stock market basically returned north of 0%. From 1982-present, after 40 years of lowering interest rates and borrowing like a drunken sailor, the stock market has risen 800%.

The Dow Jones was basically unchanged over 50 years, until 1982

Skyrocketing debt only ends 1 of 3 ways:

- Revenue begins to outgrow expenses

- Inflation -- Modern Monetary Theory suggests we inflate our way out of debt

- Default

Most developed nations aren’t going to default, or at least will try everything first to avoid it. And since most countries carry deficits even with record low interest rates, this suggests the only way debt could ever go down via revenue growth is if taxes are raised significantly. This leaves inflation as the only plausible solution.

Inflation is here. Debt is spiraling out of control. Return expectations have to be lowered. Howard Marks, as he usually does, said it best in his recent investor memo.

Marks doesn’t actually offer a solution - but one exists right under his nose. Money CAN be free-floating in space. Money can be deflationary instead of inflationary.

This is precisely why Bitcoin will likely be the world’s reserve currency, sooner than you think.

Notable Movers and Shakers

The market as a whole had a very good week - Bitcoin finished up 5% and the market as a whole finished up 9%, gaining momentum for the third week in a row. However, the way the market has gone up (and the specific assets accruing value) has been quite interesting. Bitcoin dominance fell sharply (67.7%, -2.62%), the largest weekly loss in dominance since May of 2019. There is no way to be sure whether this is a healthy rally or an abuse of illiquid markets, but it is important to look at what drove these moves to understand the underlying motives:

- Bitcoin forks (BCH, BSV, BTG, BCD) continued to significantly outperform the market last week (25%, 69%, 61%, 60%) for the reasons explained in last week’s Movers and Shakers. There also seems to be a narrative building around Bitcoin forks heading into their respective halvings (est. May 24th, est. February, est. May 23rd, no data found), which is treated as a fundamentally bullish event as emission rates decrease by 50% (a disinflationary measure that utilizes a time decay to establish a fixed supply). In fact, DASH and ZEC are also Bitcoin forks that have halvings set for 2020 (est. May 23rd, est. November) and saw significant outperformance last week (+60%, +46%). Worth noting is that LTC had its block halving on August 5th, 2019 and ran as much as 365% ahead of the date. Bitcoin is estimated to undergo its halving on May 12th, 2020.

- Ethereum Classic (ETC) continued to make strides last week, finishing up 54% following the launch of an ETC Futures product by Binance with up to 75x leverage on Wednesday. Another potential catalyst was the successful implementation of their Agharta upgrade, which was pushed in an effort to make Ethereum Classic more compatible with Ethereum. A less obvious but noteworthy observation to take into account is that Ethereum has been actively pushing to move their protocol from Proof-of-Work (PoW) to Proof-of-Stake (PoS) - a choice that seems to have left many miners/market participants disgruntled. For a basic understanding on how Ethereum and Ethereum Classic went from one project to two, read here.

What We’re Reading this Week

According to Grayscale’s 2019 Digital Asset Investment report, the firm received $608m in new commitments, surpassing cumulative investments from 2013-2018. Most of the commitments were for Grayscale’s Bitcoin Investment Trust, which lets accredited investors invest in Bitcoin without having to store the asset. 71% of new capital came from institutional investors, which are majority hedge funds. The large influx of funds can be attributed to the price increase in Bitcoin in 2019, which more than doubled.

In an Investor Alert last week, the SEC stated that Initial Exchange Offerings (IEOs) were not much different than ICOs and offered no investor protections despite being issued by cryptocurrency exchanges. These IEOs may be required to register as securities offerings and although exchanges claim to perform due diligence on these offerings, investors should be wary of claims of new technologies. The SEC further stated that exchanges issuing IEOs should be registered as a national securities exchange or an alternative trading service.

According to a new survey from Bitwise Asset Management, financial advisors are looking for ways to invest into crypto on behalf of their clients. Of the survey respondents, only about 6% have allocations to crypto, however, an additional 7% indicated they would “definitely” or “probably” look to make allocations in 2020. In addition, most advisors indicated that the uncorrelated returns of crypto were its most attractive feature. Finally, 76% of advisors’ clients made inquiries about crypto in 2019. It is clear by the numbers that retail investors have an appetite for digital assets and their advisors need products to allocate to.

LinkedIn released a report last week that covered the top hard and soft skills that companies are seeking in 2020. The top hard skill was Blockchain, beating out AI and cloud computing. The article details how blockchain has emerged from “the shadowy world of cryptocurrency”, promising to solve many business problems across multiple industries. Companies that are looking for individuals with blockchain skills include IBM, Amazon, Oracle, JPMorgan, Chase, Microsoft, and American Express. Data points like these point to the increasing importance of blockchain innovation in order for large global businesses to stay ahead.

Last week, RFR Holdings, one of the owners of the Chrysler building, agreed to sell a Zurich property to BrickMark, with 20% of the transaction in BrickMark’s BMT security token. Supposedly, this is the largest deal ever using digital assets, although the exact amount of the transaction is unknown. The tokens are based on Ethereum using the ERC-20 token standard and are a perpetual bond backed by property in BrickMart’s portfolio. The token’s price is determined by the property’s net asset value performance and offer holders voting rights. We believe we will see more unique tokenization projects such as this emerge this year as digital assets become more mainstream.

And That’s Our Two Satoshis!

Thanks for reading everyone!

Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA - Chief Investment Officer

Katie Talati - Head of Research

Hassan Bassiri, CFA - PM / Analyst

Sasha Fleyshman - Trader

Wes Hansen - Head of Trading & Operations

To learn more or talk to us about investing in digital assets and cryptocurrency

.jpg)

.png?width=1374&name=pasted%20image%200%20(3).png)

.png?width=512&name=unnamed%20(5).png)

.png?width=512&name=unnamed%20(6).png)