What happened this week in the Crypto markets?

Source: TradingView, CNBC, Bloomberg, Messari

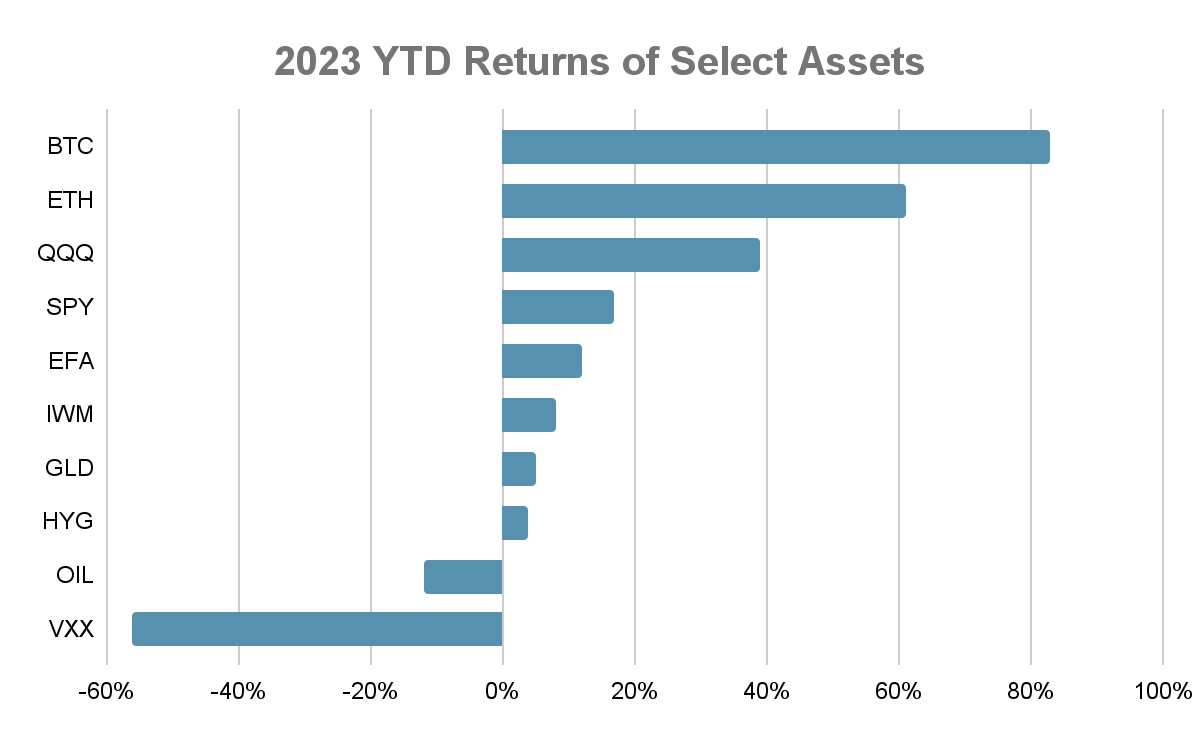

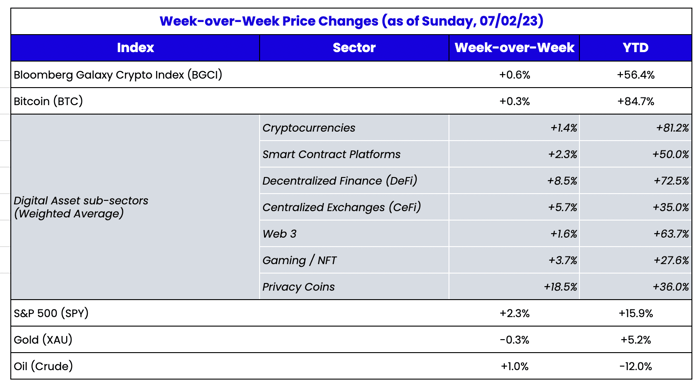

Another good month, quarter, and half for digital assets

The digital assets market ended June on good standing, rallying for the last two weeks on the heels of Blackrock’s Bitcoin ETF application, and a host of other TradFi firms announcing entrance into the digital assets arena. Bitcoin itself continues to broadly outperform. Through June 30th, it isn’t easy to find a better-performing asset across all global markets:

Source: Arca Internal Data and Bloomberg

The majority of this year’s rally occurred long before the Blackrock news, meaning most of these gains happened despite little inflows or excitement. That is

now changing, quickly. To appreciate how important this news was, you have to recognize that most conversations since November of 2022 (FTX implosion) have been centered around “

What happens to crypto when the SEC kills the industry?”, and in just two short weeks, these conversations have changed to “

Will Blackrock and Citadel dominate the industry, and who else will make all of the money?”. This was an incredibly fast change in sentiment.

And it makes sense. Don’t forget, it was only three months ago when investors were roiled by the regional banking crisis. Every investor in the world is overly exposed to traditional banking and finance even if they don’t have any direct investments in bank stocks. Their investment livelihoods are directly or indirectly tied to their fate. But very few (if any) investors are exposed to digital assets in a meaningful way. Blackrock has single-handedly changed this calculus and will have ongoing impacts on capital flows as investors play catchup.

When narratives shift, previously biased views start to become more open-minded and then common sense begins to take over. Which leads to funny conversations. For example, I loved this passage from the most recent Pantera investor letter. A completely unbiased investor with zero preconceived notions would think that regional bank equity, at 13:1 leverage, is a fraud compared to dollar-for-dollar backed U.S. dollar stablecoins. Banks are terribly designed stablecoins may sound funny, but it’s a very accurate description. It will take time for the embedded comfort and workflow to change.

Source: Pantera June investor letter

Not only are TradFi market makers and asset managers putting their hats in the ring, but the accompanying research is also becoming more forward-looking as well. Bank of America recently released a new 100-page report on the state of digital assets, and

it’s quite good, with many common sense narratives replacing previous skepticism.

“We believe the lack of user-friendly front-end interfaces and a disproportionate focus on bitcoin, memecoins, regulatory headwinds and illicit activity are overshadowing the rapid development of real-world use cases that are in active production today.”

With TradFi’s entrance to trading (EDX), asset management (Blackrock, Fidelity, etc) and research (BofA), it’s only a matter of time before every investor recognizes how underexposed they really are to this asset class.

Prometheum, Paradigm, and the SEC

Recently, a broker-dealer, Prometheum, was granted a special purpose license from the SEC to handle crypto asset securities and argued during the House Financial Services Committee meeting that no additional legislation or regulatory authority was required. This Prometheum

story is VERY strange. This past week, Laura Shin invited Prometheum’s co-CEO

on her podcast to debate regulation with Paradigm’s special counsel.

The conversation on this podcast was centered around the fact that no tokens that exist today can currently be listed on Prometheum’s ATS. While true, it's not really relevant. We first need to ask the most important question:

“How many potential FUTURE token issuers will register, and how fast can Prometheum grow the security token market and create the same type of liquidity that we’re getting on current exchanges?”

Arguing that Prometheum's licenses can't list current tokens is irrelevant since there are only like 5-10 current tokens that will even matter in 5 years. The majority will die off, as they always have, and will be replaced by new ones. We need to anticipate the future and figure out how something like Bitcoin and Ethereum (which will survive), stablecoins, STOs and the inevitable new tokens from protocols, companies, municipalities, and universities can all trade in the same venue.

No one should care if they’re holding a tokenized security or a non-security digital asset other than the exchanges who trade them and the token issuers themselves - and that’s only because these parties have more restrictions and reporting rules placed on them if an asset is deemed a security. Tokenholders themselves should not (and do not) care. There’s nothing illegal about holding securities. Whichever venue figures out how to trade & provide the liquidity for all will win.

We dedicated a blog to this topic recently.

The only question that matters is how simply and easily can tokens get issued, and listed, and who can provide the liquidity. Once determined, there will be millions of new tokens issued from individuals, companies, municipalities, universities, and protocols.

I applaud the debate, but it centered on the wrong question.