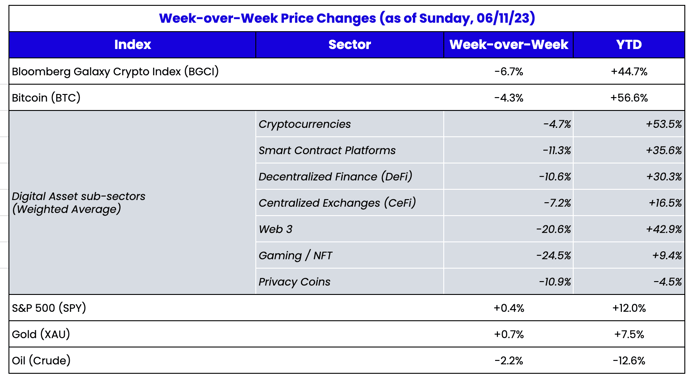

What happened this week in the Crypto markets?

Source: TradingView, CNBC, Bloomberg, Messari

The SEC is torturing this industry

Holy shit this is frustrating. Put your own investment gains, losses, schadenfreude, and political leanings aside for a second, and just put yourself momentarily in the shoes of any legitimate person trying to build, invest or experiment in the digital assets industry. Everything you’ve worked on is now at the mercy of a handful of U.S. bureaucrats. Regardless of who is right or wrong, this is torture for those tangentially involved in these lawsuits. More on this in a bit.

The SEC fired some more shots last week, filing civil suits against the world’s two biggest digital assets exchanges: Binance and Coinbase. The SEC

sued Binance, Binance.US, and its CEO Changpeng Zhao (CZ) for operating an unregistered securities exchange, as well as alleging misconduct including commingling client and proprietary funds. The SEC also

sued Coinbase, alleging that it operates an unregistered securities exchange, broker, and clearing agency. In these lawsuits, the SEC explicitly declared several tokens are “securities” (notably, BTC and ETH were not mentioned. If you recall,

SEC Chairman Gensler refused to explicitly answer this question when testifying in front of Congress last month. Both Coinbase and Binance seem committed to fighting these allegations, which means there won’t be any resolution or progress for (likely) years.

At first, the market didn’t care, and rightfully so. Even though these actions came on Monday and Tuesday, the market largely shrugged it off because none of this was new information. We already knew Coinbase was being sued (the

Wells notice was issued in March), and we already knew Binance was under investigation by both the DOJ and the SEC. As a result, prior to Friday night, both BTC and ETH were largely unchanged, while those tokens mentioned by the SEC explicitly had fallen only slightly.

This was the appropriate response. The Binance news itself is mostly irrelevant since Binance (and really all offshore exchanges) no longer operate in the US, and a bunch of non-criminal charges for past wrongdoings (2018) will likely result in nothing more than fines and a further commitment to stay out of the U.S. There were only two pieces of new information that should have been deemed negative:

- The SEC explicitly defined certain tokens randomly as securities which could lead to delistings on Kraken and Coinbase or any other U.S. exchange if they choose to stay out of the way

- Potentially negative sentiment effect if CZ is pushed out since many digital enthusiasts adore him

The Coinbase news was slightly worse. It is certainly bad for Coinbase stock given years of legal costs ahead, plus at the margin, some US institutional customers may flee, deciding that it is not worth the hassle of explaining why they trade on Coinbase amidst active SEC lawsuits (COIN -17% week-over-week). But mostly this too is irrelevant for the price of digital assets since Coinbase will fight this suit, and drag out the court process for years, likely until we get a new administration. Per

Matt Levine of Bloomberg:

“Coinbase Global Inc.’s stock is down about 17% this week, and I don’t entirely understand why. Sure yes the US Securities and Exchange Commission sued Coinbase on Tuesday, alleging that its core business is an illegal securities exchange; if the SEC wins that case it will be devastating for Coinbase. But everyone knew, with an unusually high degree of confidence, that that case was coming, and what the SEC’s arguments would be. I wrote about it in March, because the SEC formally notified Coinbase that the lawsuit was coming, and Coinbase publicized that notice and its response. And the SEC’s arguments — that most crypto tokens are securities, so if you run a crypto exchange you are running an illegal securities exchange — are also well known, and the SEC made them when it sued another crypto exchange, Bittrex, in April. There’s nothing really new in the Coinbase complaint. If the Coinbase complaint said “Coinbase is offering illegal trading in crypto tokens, plus stealing customer money,” that would be bad, and news. But the complaint just says “Coinbase is offering illegal trading in crypto tokens,” which we already knew. Surely that was priced in?”

So heading into the weekend, you could argue that all of this negative news was pretty benign and irrelevant for digital assets. How many times can you expect to rally on the same news (2020 - corporates buying BTC) or sell off on the same news (2023 - SEC hates crypto)? These headlines simply don’t have much impact anymore. In a global industry with perfect substitutes and low barriers to entry, targeting any single product (Bitcoin mining, stablecoins) or any single player (Binance, Coinbase, Kraken, BlockFi, etc) doesn't move the needle. Businesses will always continue somewhere else. The SEC warpath is bad for a few US entities; but mostly irrelevant for crypto as a global industry.

But the new news came out on Friday. While Kraken and Coinbase did not announce any token delistings,

Robinhood did. Robinhood's subsequent announcement that it would delist SOL, MATIC, and ADA, and particularly of note that it would auto-sell tokens that remained in accounts on the 27th of June, resulted in a steep Friday night selloff in these three specific tokens, as well as a delayed response lower for other tokens deemed securities by the SEC. Most tokens fell in the neighborhood of 20-30% over the weekend. While it’s impossible to know exactly why the selling started, it was most likely that market makers front-running the selling, combined with fresh shorts taking advantage of upcoming sell pressure.

Market response of SEC-named tokens last week

Source: TradingView

Markets don’t react to known information (Coinbase/Binance), but they do react to new information (Robinhood). Unlike Binance and Coinbase, whose sole business model relies on the ability to have customers trade these “securities”, this is a fairly meaningless part of Robinhood’s business model these days and certainly not worth the fight. The last quarterly report from Robinhood suggested that there were

$1.3 billion worth of crypto tokens owned and held on the Robinhood platform, so it is fair to estimate that a few hundred million dollars worth of ADA, SOL and MATIC will have to be transferred off the platform, or sold, in a matter of weeks.

New information led to selling, and that was a fairly efficient market response.

Here’s the thing. IF you believe that any of these 3 tokens have real value, whether that be financial, social, or utility value, then its designation as a security or not is irrelevant to that long term value. The only thing this designation does is limit current liquidity options due to the lack of infrastructure available to support security tokens.

And therein lies where my earlier frustration stems from. I don’t give a damn what is a security, and what isn’t. I trade securities all the time. There’s nothing illegal about being a security as long as securities laws are followed. Please feel free to call all tokens securities if you want. It won’t bother me in the least, it doesn’t change the long-term value proposition, and I welcome a registered exchange and rock-solid, “tried and true” U.S. securities regulations to help shepherd in the next wave of blockchain adoption…

… BUT…

… if you (the SEC) are hellbent on calling every digital asset a security and regulating the whole industry, then for the love of god, find a way to make it cheaper and easier for exchanges to get licenses in order to trade them, and for token issuers to be able to issue them, and for truly decentralized projects to be able to comply. The everyday people in this industry do not need to continue to suffer simply because Congress hasn’t issued new laws yet, and the SEC is unwilling to adapt its 80-year old laws to new technology.

When you, the SEC, say that every exchange is “commingling assets”, you are essentially making an argument that exchanges and brokers need to be separate- and anything else is commingling. This is not wrong, but also impossible to adhere to with T+0 blockchain settlement. Blockchain finance uses real-time settlement, which means anyone who trades a digital asset must:

- Hold tokens where you trade (i.e. exchanges) so you can transfer them immediately upon a transaction

- Trade over-the-counter (OTC) and settle later, which invalidates the whole point of blockchain technology

Everything coming out of Washington DC indicates that regulators are either going to force T+1 (or 3) settlement, or don't fully understand that blockchain by design is T+0. Neither of which is good.

In general, any investor or founder can deal with bad outcomes. Constant uncertainty, however, leaves everyone in limbo.

Meanwhile, the U.S. House Financial Services Committee, chaired by Representative Patrick McHenry, who

co-authored the recently released Digital Asset Market Structure proposal, will meet this week on June 13 to discuss “The Future of Digital Assets”. While it is just a draft, it is moderately encouraging, at least relative to everything else. As Galaxy Digital wrote in its weekly note to clients:

“Most importantly, the Bill establishes a sound framework to determine whether a protocol is decentralized or centralized. From this, a key takeaway is the Bill places more emphasis on token ownership concentration over network control by validators/miners. The Bill considers insider ownership of 20% outstanding supply to be deemed centralized, which could ensnare protocols like Solana, Arbitrum, and Uniswap in which insiders hold larger percentages of the supply. In the event this Bill is enacted, these protocols, among many others, will be heavily incentivized to reduce insider token concentration to avoid legal pressure in the U.S. Protocols with large DAO treasuries will have to evaluate the tradeoffs between decentralizing to avoid securities regulation and retaining tokens to innovate towards product market fit.

Additionally, the Bill provides a clear roadmap for U.S. crypto exchanges to register domestically to mitigate the trend of U.S crypto entities moving operations overseas due to regulatory uncertainties. The proposed path for crypto exchanges to register as Alternative Trading Services (ATS) will require the SEC to revise their guidelines for ATSs to exempt exchanges that offer digital assets, digital commodities, and payment stablecoins from registration as a national securities exchanges. This requirement also involves the SEC modifying their rules to allow broker dealers to custody digital assets among other regulations for digital assets. The pressure imposed on the SEC to update their outdated legal frameworks would help foster growth for U.S crypto exchanges, enabling the U.S. to sustain its global dominance in the digital asset space in light of crypto dominance rapidly growing overseas. Ultimately, on the question of exchanges, the Bill provides all the workable clarity that the SEC currently lacks, and clearly addresses all the registration points the SEC is arguing in court.”

It’s a big week ahead for digital assets. Unfortunately, it’s just not what any of us got into this industry for.