What happened this week in the Crypto markets?

Source: TradingView, CNBC, Bloomberg, Messari

Idle Capital is Coming Back

The best trade of 2023 has been the contrarian trade. Taking the opposite side of consensus has

worked in just about every asset class year-to-date. So what do you do when just about every leading economic indicator is once again pointing to recession? The

Conference Board’s Leading Economic Index declined in May for the 14th month in a row, but there are two components in the Leading Index that are not currently showing economic weakness: the stock market (S&P 500) and building permits (increase in residential homebuilding activity). The stock market strength has certainly lacked breadth, with a handful of tech giants generating the majority of returns. But still, the overall strength is a far cry from the early 2023 expectations of demise.

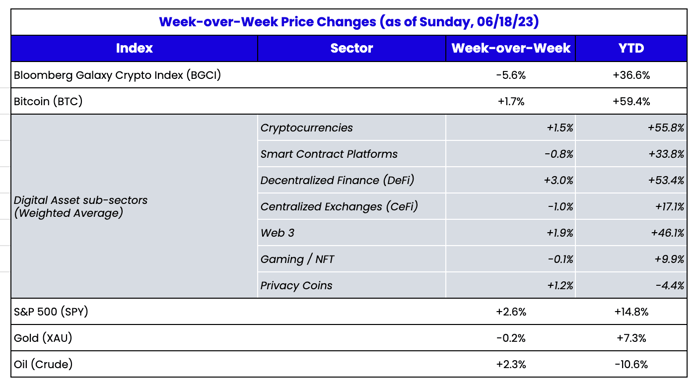

Similarly, Bitcoin’s strength continues to confound the masses after 2022’s weakness. Last week was no exception, as Bitcoin (BTC) jumped another +15% following Blackrock’s BTC ETF application, and now sits +84% YTD. BTC dominance (BTC.D), a mostly useless indicator given the constant additions of new non-Bitcoin tokens, has risen to 51%, its highest level since April 2021, showing just how much BTC has dominated overall digital asset returns.

Traders are speculating that Blackrock’s application for a spot Bitcoin ETF will lead to more participation from traditional investors. Blackrock is not alone. Traditional incumbents are now seeing an opportunity to grab market share with the Citadel / Fidelity launch of EDX and Deutsche Bank applying for a digital asset custody license in Germany. These longer-term tailwinds are offsetting supply and macro concerns. It’s also worth noting that these new entrants weren’t “spur of the moment”- rather these initiatives have been in the works for a long time and no one was in a hurry to make announcements during a one-way bear market. Now that the spigot has been opened, we expect the announcements to keep coming causing “blockchain purists” irritation because they don’t want to see traditional financial powerhouses take over their invention.

The word “disruption” makes its way into a lot of Silicon Valley pitchbooks. Just about every new technology or product is meant to disrupt and displace an incumbent. Many thought blockchain would do the same - disrupt and displace major banks and brokerages. But as the SEC continues to tie up blockchain-native companies in lawsuits, here comes the squeaky-clean TradFi firms to take their place. And honestly, this should have been expected. Almost four years ago to the day, Facebook announced its first foray into the digital assets world, and

we wrote this at the time:

“The crypto world is very good at creating groundbreaking technology, but new technologies without distribution often fail. Robo-advisors are a good analogy. Betterment and Wealthfront have amazing technology, but this technology was easily replicable by financial advisory powerhouses with larger distribution capabilities. So what happened? Every major financial advisory firm now offers similar technology services to their clients. Distribution and brand trumped technology.”

You can replace Facebook with Blackrock or Citadel now and say the exact same thing. Regardless of Bitcoin’s value proposition of being a self-custodied, T+0 instrument, the majority of people just want to own a proxy that entitles them to financial gain, and Blackrock will be able to deliver that better than anyone else who has tried to date.

And market participants are not waiting for Blackrock’s approval. The market has been bid since this announcement, and it seems entirely driven by new capital. So where is this capital coming from? A few theories:

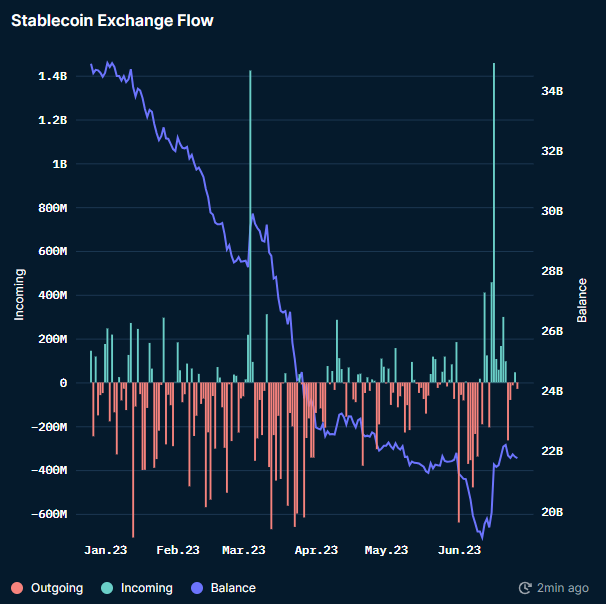

1) Those holding their “cash” as stablecoins are starting to put this capital back to work. Monitoring stablecoin flows into exchanges is a good way to visualize this, as the majority of these stablecoins will be sold in order to purchase BTC, ETH or other tokens. This capital never left the digital assets market per se, but it was certainly uninvested, and the Blackrock news was a catalyst to re-enter the market.

Source: Nansen

2) TradFi funds are start buying and trading again. Similarly, during the bull run of 2021, many TradFi funds (macro funds and long/short equity funds) were trading digital assets, only to exit completely towards the end of 2022. But these institutions largely traded in a few spots – via CME BTC and ETH futures, and via OTC trades with Coinbase, FalconX, Cumberland, Galaxy and other large OTC dealers. While most of these funds stopped trading in 2022, they didn’t necessarily close their accounts, and all indicators suggest that these funds woke up last week and began buying. Volumes have increased at OTC shops, CME futures volumes are at YTD highs, and the CME basis has widened suggesting that funds are using futures to express levered long bets.

Source: VeloData

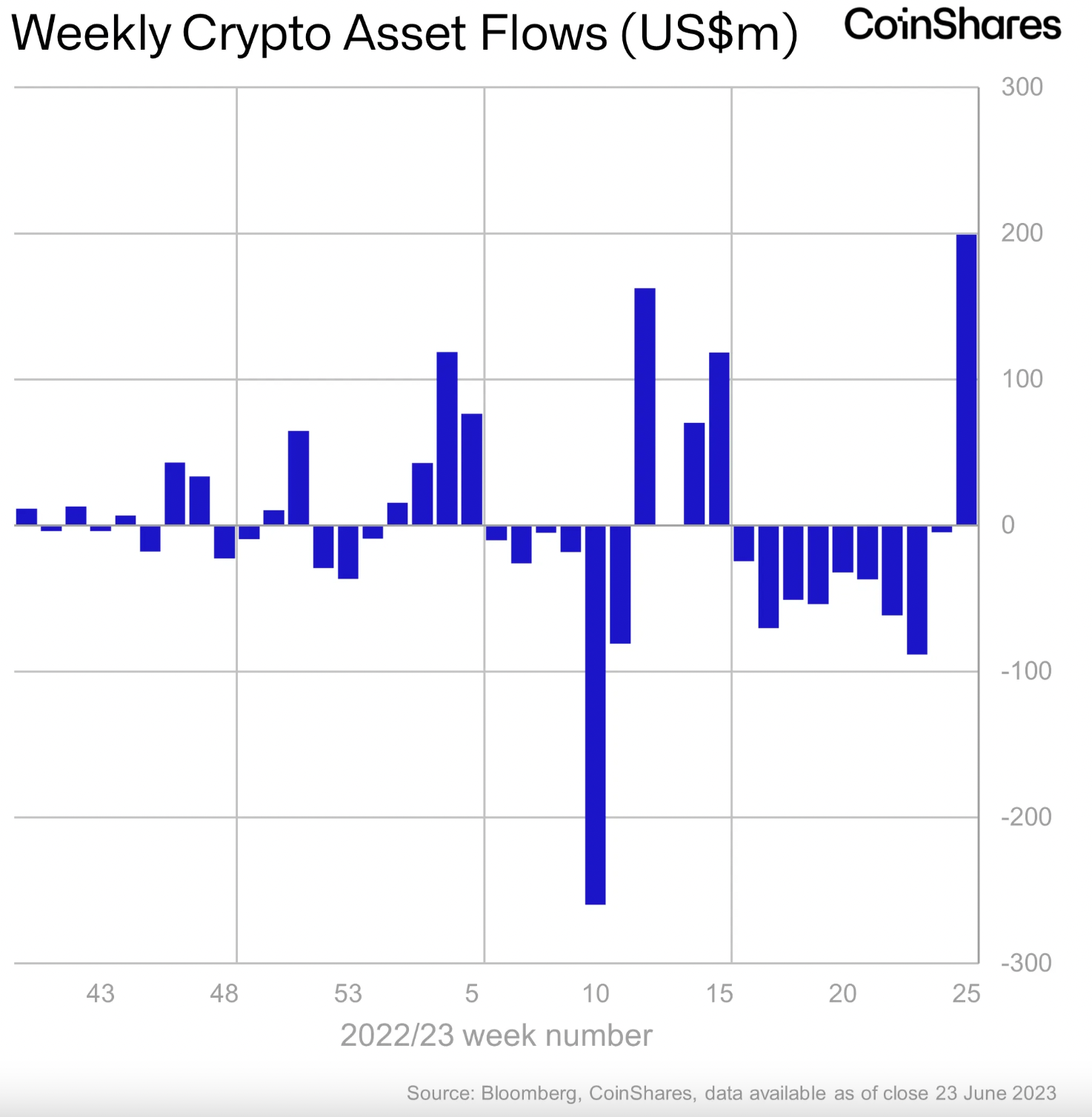

3) The last wave of new capital is coming from first time allocations (or increased allocations) out of cash in banks and brokerage accounts. This is harder to measure. While not a perfect indicator since it fails to take into account Institutional flows into private funds,

CoinShares’ weekly monitor of ETF and ETP fund flows is a helpful proxy. Most recently, we saw the largest inflow of the year totalling US$199m, correcting almost half of the prior 9 consecutive weeks of outflows.

These three sources of capital will be important to monitor. Over the past 18 months, there were certainly more investors moving to cash, or out of digital assets altogether, than there were newly formed digital asset investors. We also saw institutional investors that were in the 9th inning of allocation due diligence completely revert back to the first inning after the fall of FTX. But if these trends reverse, it could prove to be rocket fuel for a market that has already been trading well in the absence of new money.