Source: TradingView, CNBC, Bloomberg, Messari

A Bitcoin ETF Fight

Stocks experienced their largest weekly decline of the year, with Nasdaq down close to 6% and S&P 500 down more than 4%. The weak jobs data showed that the labor market is softening but not collapsing yet, which likely opens the door for just a 25 basis point cut by the Fed later this month. This will be the last FOMC meeting before election day, November 5th.

The digital assets market continued its weaker trading last week, though last week felt different. While previous weeks were led by spot selling and general apathy, last week it was clear that fresh shorts were developing, trying to push the market lower alongside equities, and that may be why the market bounced easily over the weekend after hitting key support levels. The sellers found actual buyers for the first time in weeks. The Bitcoin ETFs have now seen a combined $1.2 billion in outflows over the last eight trading days, which matches the inflows over the previous two months.

Most readers know I don’t care too much about Bitcoin or the ETFs. Bitcoin is an interesting, binary asset akin to a

CDS contract or options contract, either worth $0 or tens of trillions, and every price in between simply illustrates the probability of hitting one of these extremes. The ETFs themselves are just a

necessary evil – we should strive towards bringing the world’s assets on-chain, not bring on-chain assets to Wall Street’s outdated ETF rails.

That said, it’s always interesting to see how extreme the reactions are to the Bitcoin ETF. Somehow, Bitcoin has become just as polarizing as politics, so, I suppose, it’s fitting that crypto finds itself in the middle of the U.S. Presidential election debate.

Take this

recent tweet by Jim Bianco of Bianco Research about the failures of Bitcoin ETFs. On the surface, this tweet thread contains many facts.

- Bitcoin price has been down recently

- Volumes of the BTC ETFs are lower than the volumes of MAJOR stock and bond indexes

- Inflows have slowed

All of this should be fairly obvious without an 8-page Tweetstorm. But if you actually read the tweet thread, it is written in a decisively negative way to try to, I don’t know, embarrass the ETFs? Perhaps this is just clickbait because Bianco knows that Bitcoin is polarizing and will generate many pro and anti-responses. Maybe he really hates Bitcoin and wants everyone to know he thinks it will fail? It’s really hard to fathom why you would write this when you’re a respected research analyst with a lot of good data.

First, to suggest that the 6-month-old Bitcoin ETFs, which represent a largely misunderstood and relatively new technological asset, is a failure because it isn’t as popular yet as SPY, QQQ, LQD, HYQ and GLD is hilarious. These are the largest and most popular ETFs in history that represent the largest asset classes that exist. Even comparing BTC to these assets should be viewed as a win for crypto.

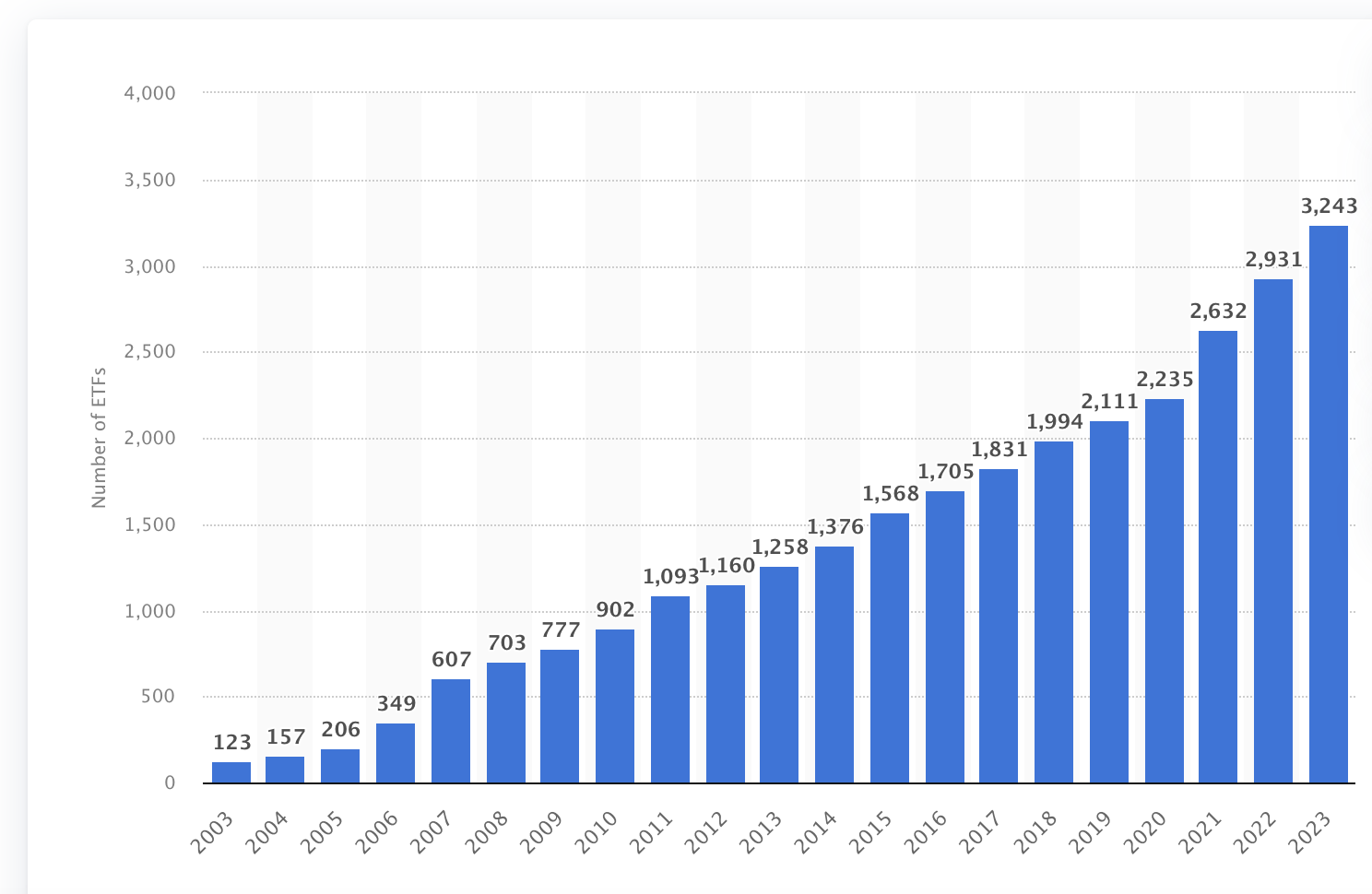

Second, has Bianco Research ever issued an ETF analysis this in-depth about any other ETFs that have been issued? The graph below shows the number of ETFs listed in the U.S. over the last 20 years. How many of these still exist or have surpassed even $100 million in assets (let alone the $46 billion that the BTC ETFs have amassed)?

Naturally, Matt Hougan at Bitwise came out with a

rebuttal.

The reality is that both Jim Bianco and Matt Hougan are right. Bitcoin ETFs have slowed, but they are still a success. But all of this is just so tiring. By all objective measures, the Bitcoin ETFs themselves are a massive success, and they are not expected to be as popular as SPY or QQQ. And whether or not Bitcoin ultimately succeeds or fails will have nothing to do with the ETFs. In fact, whether blockchain ultimately becomes a technology that is utilized by billions of people or not will eventually have nothing to do with the Bitcoin ETF.

It’s fine to hate Bitcoin. It’s fine to love Bitcoin. It’s also fine to ignore Bitcoin. But it is exhausting to hear, write, and talk about the same things repeatedly. So many continue trying to create a narrative out of nothing, and others feel the need to defend this narrative. Yet very little is actually being accomplished.

As we wrote a few weeks ago about the “

Crypto Investing Paradox”, we’re at the point now where almost everyone can see the potential of blockchain technology, but there are real regulatory and legal hurdles in the way of mass adoption. And that’s probably all that matters right now. The tech is great; but investing in the tech is at the mercy of timing factors that may be out of your control. But talking about the technology will get you new followers.

Some Stats for September

According to our friends at Cumberland:

- Bloomberg's Global Aggregate bond index has seen a negative total return for each of the last seven Septembers.

- 10-year U.S. Treasuries have seen higher yields in 7 of the last 8 Septembers, with Gilts higher 9 out of the last 10. In addition, the previous 9 Octobers have also seen higher Treasury yields. One argument for why this pattern may occur is that global bond issuance (government and corporate) dries up over the summer holidays (encouraging a bond rally) and then surges in September and October (encouraging a sell-off).

- Gold has been lower in 10 of the last 11 Septembers.

- The iTraxx Crossover index has been wider in 8 of the last 10 Septembers.

- The S&P 500 has been lower for the last four Septembers.

- Much has already been said about September as a historically bad month for crypto. And indeed, over the last 7 years, 6 out of 7 of those Septembers have been in the red, with an average move of -7%. Only in 2023 did we see a green move of +4.07%.

- By the end of the month, we’ll also be just 5 weeks away from the U.S. election, and close election races (as this still is) usually promote sideways to lower equity markets in the build-up, before a big rally after, regardless of who wins. This ties into the seasonals, as we’ve only seen 6 negative Novembers for the S&P 500 since 1995 with 11 of the last 12 higher.

That said, the best way to make money in 2023 and 2024 has been to fade consensus. So… um… guess we’ll see.

How Service Providers Have Changed

Written by Wes Hansen, Head of Trade Operations

Lately, a huge push has been made toward launching new service providers in the digital asset industry. A lot of the more established trading and lending desks have baggage from the last cycle or have defaulted, and many want to start fresh and offer something without residual issues from 2021-2023. The same is true for many hedge fund managers who don’t want to regain their high water mark or can’t afford to stay in business while trying. As such, it’s easier for people to start a new business from scratch.

There was no consolidation during the last cycle. There should have been a consolidation of service providers and sell-side desks during the bear market, but everyone was so beaten up and gun-shy that nothing really happened. Therefore, this industry is still incredibly fragmented, leaving plenty of opportunities for new entrants to steal market share.

BUT, the biggest problem is that none of these new entrants are doing anything differently. Countless new firms are pitching their services – “come trade with a new OTC desk because we have the best liquidity and connections for trading Bitcoin.” This is the same generic pitch that has been pushed endlessly for years. For one, it shows that few are bothering to understand the client's actual needs, but it also indicates that many think they can make enough money just by being one of many without trying to improve on what’s already out there. It’s simply “if you build it, they will come”. The investment side of our space has become stale because there is money to be made without trying too hard. The new entrants aren’t hungry enough, and so progress has slowed.

But it isn’t all bad news. Some innovators are out there, and entrepreneurs are trying to advance the space. They just have nothing to do with the investment management of digital assets, and maybe that’s a good thing. They’re actually building and advancing the cause of digital assets without considering the quick cash grab that is the current state of sell-side digital assets service providers. There’s a strong possibility that the firms and protocols that ultimately drive this space forward for decades are being built entirely under the radar of most investment-focused participants.