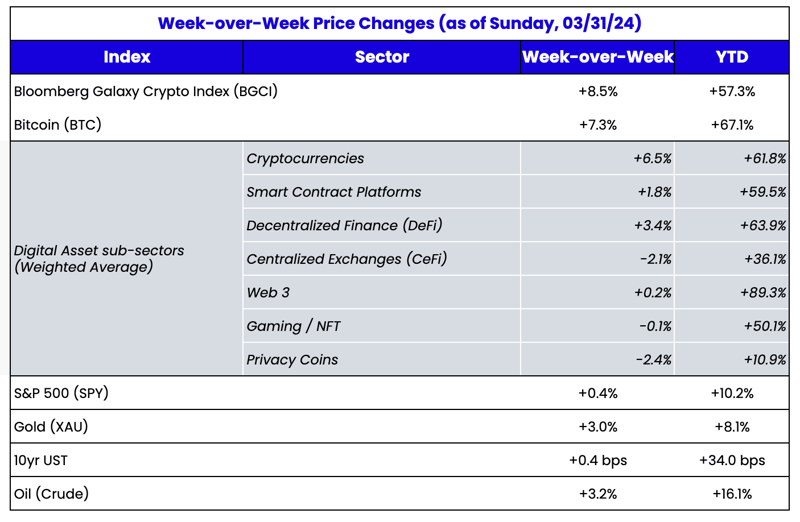

Source: TradingView, CNBC, Bloomberg, Messari

Source: TradingView, CNBC, Bloomberg, Messari

Special Edition Written By Nick Hotz, Analyst at Arca and Sami Kassab, Partner at OSS Capital

Over the weekend, Bittensor emerged as a primary target of criticism, with some prominent investors dismissing it as a useless project or labeling its token, TAO, as merely a memecoin. Arca has been a fan of Bittensor and an investor in TAO since mid 2023 and wanted to dispel some of the incorrect information being disseminated while presenting our own optimistic view on the protocol's future. We brought in

Sami Kassab, former Messari analyst and current partner at OSS Capital, as a co-author.

In this piece, we aim to address Bittensor critics, and having some background in crypto and AI is helpful. If you are new to the space or Bittensor, we recommend checking out one of

our earlier pieces or

other excellent overviews.

In short, Bittensor is a launchpad for AI applications and the underlying infrastructure they require, similar to how Ethereum serves as a foundation platform for smart contracts. Within the Bittensor ecosystem, various specialized networks, known as subnets, are dedicated to specific AI use cases such as

financial forecasting,

intelligent search capabilities, and

creative image generation. Other infrastructure-focused subnets augment application-driven subnets, providing resources and services such as model pre-training, fine-tuning, data collection, and data storage.

Each subnet is overseen by an owner responsible for designing a unique incentive system tailored to the subnet's objectives. Within these subnets, there is a dedicated set of validators and miners. Subnet validators all run the same validator software (i.e., incentive mechanism) designed by the subnet owner, directing the focus of miners (model operators and resource providers) towards targeted tasks. Additionally, subnet validators serve as the exclusive gateway for external access to a subnet’s services and resources, as they alone have the ability to query miners.

We see Bittensor’s subnets falling into two main categories:

- Public good subnets

- Validator service subnets

Public Good Subnets Accelerate Open Source AI

“Open source initiatives” have long faced challenges due to the lack of financial incentives for freely sharing one’s work. This has been particularly true in the open-source AI sector, where reliance on voluntary contributions has hampered growth. Bittensor’s public good subnets emerged as a solution by allowing open-source AI researchers and engineers to monetize their work, thus propelling the field forward.

Take

Nous Research’s subnet as an example. The

subnet rewards the fine-tuned models that most closely match GPT-4’s performance through a competitive leaderboard framework. To compete, miners must upload their models to HuggingFace, ensuring it is open-sourced for validators to benchmark. This prevents validators from charging for exclusive access.

This incentive model actively motivates contributors to fine-tune open-source large language models (LLMs). As a result, a wealth of fine-tuned models has been generated and shared, becoming a public good that benefits the entire community and propels the advancement of open-source AI.

Other subnets following this model include:

- Subnet 3 by MyShell: incentivizes advances in open-source text-to-speech technology

- Subnet 9 by RaoFoundation: incentivizes advances in open-source pre-trained models

- Subnet 24 by Omega Labs: incentivizes collecting open-source multimodal datasets

While these subnets may not offer direct revenue-generating opportunities for their validators, their contributions allow Bittensor’s application-driven subnets to integrate and monetize their outputs. For instance, the Vision subnet plans to integrate top models from Nous’ subnet into its decentralized inference network. This integration will allow validators on the Vision subnet to offer monetized access to these models, such as through a chatbot interface provided by

Corcel.

In the future, subnets focused on fine-tuning and pre-training subnets may evolve from the public goods model. For instance, by utilizing zkML, a subnet could allow validators to evaluate the performance of miners' models without revealing their proprietary weights. This could lead to new monetization strategies that preserve intellectual property privacy.

Validator Services Subnets Monetize Miner “Intelligence”

For those familiar with finance jargon, public goods subnets are the “back office,” while validator service subnets are the “front office.” Validator services subnets use existing AI models and infrastructure to create monetizable B2B or B2C products or services.

Subnet 8,

Proprietary Trading Network (PTN), falls into this category. The subnet incentivizes miners to provide profitable trading strategies across digital assets, forex, and equities. Miners who suggest successful trades are allocated an increasingly large amount of TAO emissions, while miners that drawdown by more than 10% are deregistered. Validators can access these signals to make trades themselves or package them to sell to other traders or funds. Critically, validators like

Timeless, who understand the miner landscape, can create a product that is better than the sum of the parts - aggregating the best miners’ predictions to create high-conviction trade recommendations.

Corcel is another example of a validator building a monetizable product atop a subnet. Subnet 18, Cortex.t, arbitrages the cost of premium subscriptions to Anthropic, OpenAI, and Google, and has miners serve responses from these centralized models. Corcel serves these models for free but gets its value from having low latency and access to miners on subnet 18. As it aggregates users, Corcel plans to charge for API access, undercutting the price point of centralized providers while providing an identical product.

The validator service subnet model provides a compelling incentive for entities to either become validators on specific subnets or to pay for access to a validator’s API. By doing so, a company can create and monetize products and services that capitalize on the intelligence generated by miners. Other subnets that adopt this business model include:

- Subnet 4 by Manifold Labs: enables the creation of products leveraging a decentralized and verifiable inference network

- Subnet 5 by Kaito AI: provides the foundation for building applications with a decentralized search engine at its core, enhancing data retrieval and analysis capabilities

- Subnet 21 by Philanthrope: offers a backbone for applications and cloud storage solutions, leveraging a decentralized network for decentralized data storage

Addressing Bittensor Criticism

Recently, Bittensor has encountered criticism concerning its operational

efficiency and reward system, which some

believe hinders miner innovation and incentivizes miners to respond similarly.

Addressing the efficiency concern, it's important to dispel the myth that all queries on a subnet are sent to every miner. In fact, only queries for the purpose of miner evaluation are distributed to the entire subnet. User-initiated queries are routed selectively, either to a single miner or a group, based on the validator's routing strategy. This allows validators with insight into the miner ecosystem to create sophisticated routing algorithms tailored for specific applications. Additionally, queries are not made on the blockchain itself but rather over an API layer entirely separate from the blockchain stack.

The critique regarding the reward system holds some weight. The incentive mechanisms, crafted by subnet owners, direct miners' optimization efforts. This means the incentive design's effectiveness constrains the subnet's collective intelligence. Most subnets currently employ centralized models to judge miner outputs, which could potentially limit surpassing these models in quality or performance. This method is sufficient while open-source models are still catching up, but innovative benchmarking strategies will be necessary once they reach parity.

This challenge injects a competitive element into the Bittensor ecosystem. Subnets are incentivized to outdo one another based on the efficacy of their validation mechanisms. This is already prompting the

development of more refined incentive and validation frameworks. One example is a

proposal by some teams to incorporate human evaluation into the validation process, which could significantly enhance outputs.

Critiques of the reward system suggest that it encourages similar responses from miners when in reality, miners are driven to outperform each other by optimizing for the specific objectives of their subnet. This not only promotes diversity in outputs but also drives innovation. The Yuma Consensus mechanism incentivizes validators to rank miners similarly to ensure consistent evaluation of outputs.

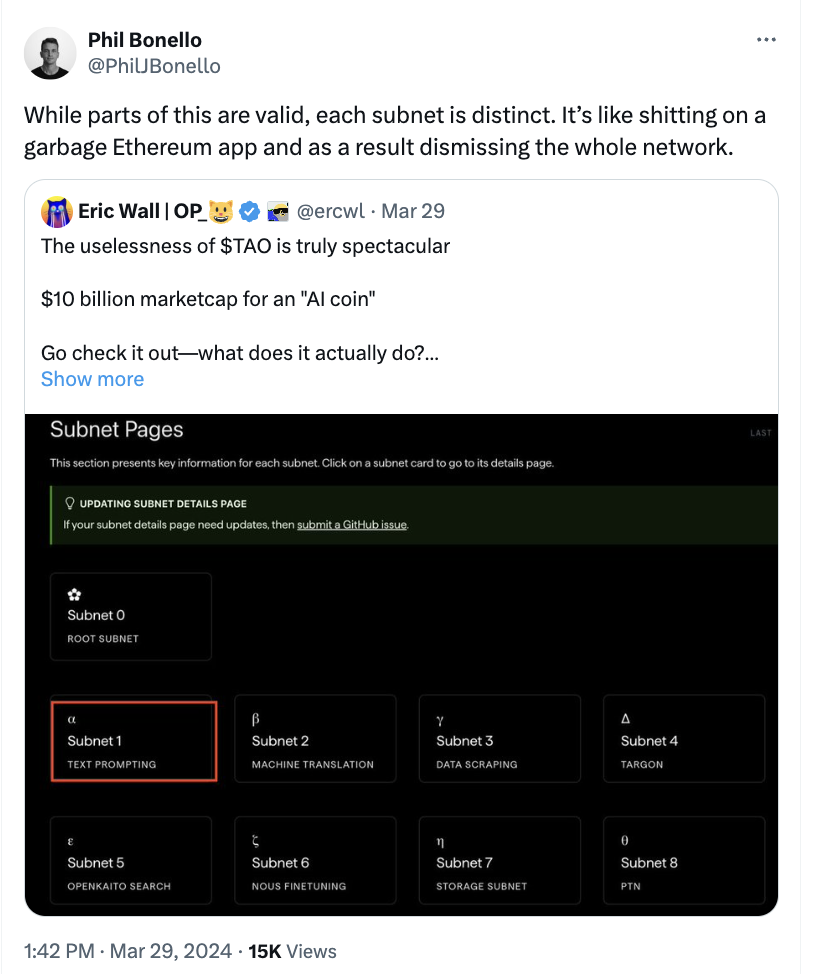

In the midst of these critiques, subnet 1, created by the RAO Foundation for text prompting, has come under scrutiny for its incentive design. However, the criticism stems from a lack of understanding of the subnet's

objective. Subnet 1 is not merely a chatbot, it aims to reward miners for efficient information retrieval within its models. Validators use these retrieved files to construct reference answers, allowing them to measure which miner can retrieve the correct information the fastest.

It’s important to note that subnet 1 represents just one team’s approach to solving a specific problem. Critiquing the entire network based on the perceived shortcomings of subnet 1 is like evaluating the Ethereum network on the basis of a single application (H/T

Phil Bonello).

Source: X

Another concern is that the current system relies heavily on the altruism of validators to function properly. Validators get to determine the amount of emissions each subnet receives but there is no explicit incentive to choose subnets that benefit Bittensor’s long-term productivity. In the current design, validators could easily resort to pay-to-play schemes and cronyism. Contributors from the Opentensor Foundation recently proposed

BIT001: Dynamic TAO to address this issue, which proposes adding a market-based mechanism for determining emissions to subnets that all TAO stakers will compete in.

The Native TAO Token Is Deeply Integrated Into The Bittensor System

Finally, others argued that Bittensor’s native TAO token was a

useless, “

nonsense” “

memecoin” and it only gained value because of the

narrative around crypto and AI, and whose true value is zero. As much as we would love for the memetic value of Bittensor to be on par with that of

dogwifhat, we begrudgingly recognize there is far too much utility of the TAO token for that to be the case.

To recap, TAO is emitted by the protocol to the three main stakeholders - miners, subnet owners, and validators:

- Miners complete specific ML tasks, like inference or fine-tuning, or provide infrastructure such as file storage or compute

- Subnet owners design the reward landscape to facilitate maximum value creation

- Validators use a reward model designed by the subnet owner to determine how well miners complete a task

Source: Messari

Additionally, the four primary mechanisms from which TAO derives value include:

- Validators who stake TAO gain the ability to direct emissions to their, or another, subnet, proportional to the amount of TAO staked

- Subnet owners must lock TAO to register a subnet

- Miners and validators must burn TAO to get registered on a subnet

- Validators must stake TAO to get access to miners in order to sell the goods and services they produce

Individual subnets rely on a native token issued to network contributors to bootstrap supply and future network value, just like most decentralized physical infrastructure networks (DePINs). For example, a file storage network like Filecoin, Arweave, or Subnet 21 - FileTAO, needs to pay miners to store and retrieve information to grow sufficiently for the demand side to see value in the network.

Critically, the TAO token also serves a unique role in the Bittensor network by distributing the emissions to subnets. In the current iteration of the network, validators are tasked with determining which subnets deserve TAO emissions. The network implements a delegated staking system to choose validators, where delegators stake their TAO to validators who vote on their behalf. While validators are relied upon to make decisions in the network's best interest, the responsibility of directing emissions is potentially valuable in itself. If top validators were ever to stop believing in the future of the network, cronyism and self-dealing could allow them to monetize their powerful position substantially.

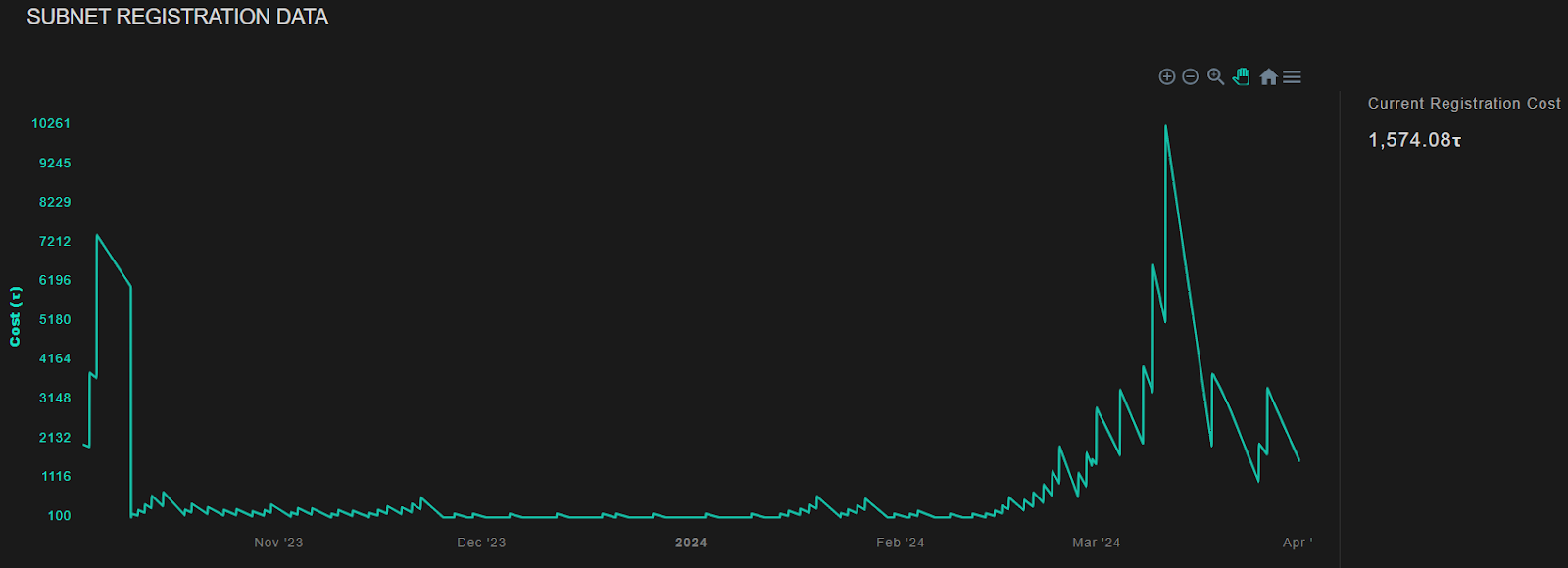

When new subnet owners register a subnet, and once the subnet cap is reached (currently 32), the system automatically deregisters the subnet with the lowest emissions. Importantly, this weeds out low-quality projects and allows new potential talent to try to attract emissions. The system algorithmically determines how much TAO a subnet owner needs to lock by reviewing what past subnets have registered. The mechanism aims to balance accessibility to build on Bittensor with existing subnet owners. Contention around this balance increased recently as registration locking costs reached 10,000 TAO, representing significant demand to build on the network.

Source: Taostats.io

Like many other DePIN projects, miners and validators participate in a burn and mint equilibrium (BME) system that adds a disinflationary effect to the token. The token is on a similar issuance schedule to Bitcoin with a 21M token cap and 4-year halvings. However, the BME temporarily removes tokens from the circulating supply, creating a consistent source of demand for TAO, thereby pushing back future emission halvings. On average, this effect has mitigated 11% of new emissions, pushing the halving back 5 months from its typical 4-year schedule (H/T

Will Scheinman). As subnets and reward landscapes mature, miner competition will increase, resulting in lower margins and a greater proportion of issuance being burned.

While all these intra-system utility mechanics are nice, validators' ability to monetize access to miners is the most critical mechanism as it moves the tokenomic system away from being a reflexive loop into real-world value territory. Miners have a financial incentive to respond to validators because it increases their “trust” scores. This trust score is a key determinant in the amount of TAO emissions miners receive. As a result, validators act as the sole access point to miners.

Different validators achieve different levels of utility from accessing miners. In the previously referenced PTN example, validators can view miners' trade recommendations. One validator may simply route trades from the best-performing miner to their clients for a subscription fee. However, another could aggregate miner responses to add conviction to their recommendations, use responses to create diversified portfolios, or even analyze individual miners. to realize, for example, a specific miner has a clear edge when trading the Euro, but not the Aussie dollar. Adding this additional layer of value in routing will allow the validator to monetize at a much higher level. As a result, these two validators have sharply different individual utilities of owning and staking TAO.

Critically, because validators can differentiate themselves via their routing algorithm, the market is not commoditized, with profits trending to zero over time. Instead, it is a monopolistic competition with differentiated skills, brands, technology, and teams creating new products on top of miners' commoditized outputs. On PTN, the value to validators of buying and staking one additional TAO (marginal cost) equals the incremental value they can capture by selling their outputs (marginal revenue).

Obviously, Bittensor is in an extremely early stage, with most subnets in pre-earnings and even pre-revenue stage. However, as a generalized rule, the minimum fair value of TAO should equal the total revenue validators can earn from routing miner outputs plus the discounted future revenue from monetizing outputs from potential future subnets. We see the rise in the price of TAO over the past six months reflecting not memetic speculation but increasing expectations about the potential future revenue validators will attain.

In contrast to early crypto flywheels like the first iteration of Helium’s HNT or Axie Infinity’s AXS, the TAO token is naturally resilient to reflexivity. Validators, and eventually token stakers, are charged with determining emissions across subnets. As the value of TAO rises, a greater dollar value of emissions can be directed across various projects, and the proverbial “hurdle rate” for receiving emissions will fall. Like any market mechanism, this will eventually create waste and inefficiency as low-quality projects suck up a greater proportion of emissions, which eventually can lead to a downward repricing of TAO as growth prospects weaken.

As belts tighten, validators are forced to re-diligence their emission decisions and increase the hurdle rate for providing them, weeding out bad actors and poor performers. As prices plumb their lows, only the highest quality subnets that provide the most growth and potential value for Bittensor will receive emissions, helping stabilize the system, similar to the difficulty adjustment in Bitcoin. The more efficient allocation of resources subsequently sets the stage for the network's future growth.

An Optimistic View of Bittensor

The passion of the Bittensor community was immediately apparent from our first visits to the project’s Discord, where community members were in deep conversation about technical machine learning concepts and how to participate in and advance Bittensor and not debating the token price, like many other crypto servers. Originally a grassroots initiative driven by independent contributors, Bittensor is maturing into a vibrant ecosystem attracting established builders such as Nous, Kaito, MyShell, Wombo among others, who are all drawn by the substantial business value and cost savings offered by Bittensor.

We both came into the crypto space as strong, quasi-maximalist believers in Bitcoin and weren’t quite sure that anything else valuable would ever come out of crypto at the beginning. However, we saw the vitriolic immune defense of the Bitcoin community as it rejected Ethereum as a “scam”, all while believing that useful projects were being built on Ethereum. We later saw the same vitriol happen with Solana (“valueless”) as Ethereum believers noticed that Solana was encroaching on their territory though DePIN projects were migrating en masse to the only chain capable of handling them.

This weekend reminded us of Ethereums’ and, later, Solanas’ struggles to gain acceptance among the mainstream crypto audience and the condemnation they both endured. Where others see a redundant ChatGPT clone attached to a worthless memecoin, we see a dynamic community of crazy-smart people passionate about using new incentive mechanisms to accelerate the development of open-source artificial intelligence.

We are still very much in the early days of Bittensor’s journey, yet all signs indicate it’s on the right trajectory. There is a big difference between a good project struggling under the weight of its own success and a useless project. Ultimately, believing in Bittensor is a bet on the power of market dynamics; it’s a belief that, given the right financial incentives, the brightest minds will converge to surmount any challenges.