Source: TradingView, CNBC, Bloomberg, Messari

This week's edition is written by Nick Hotz, CFA, Analyst at Arca

AI + Crypto Re-emerges

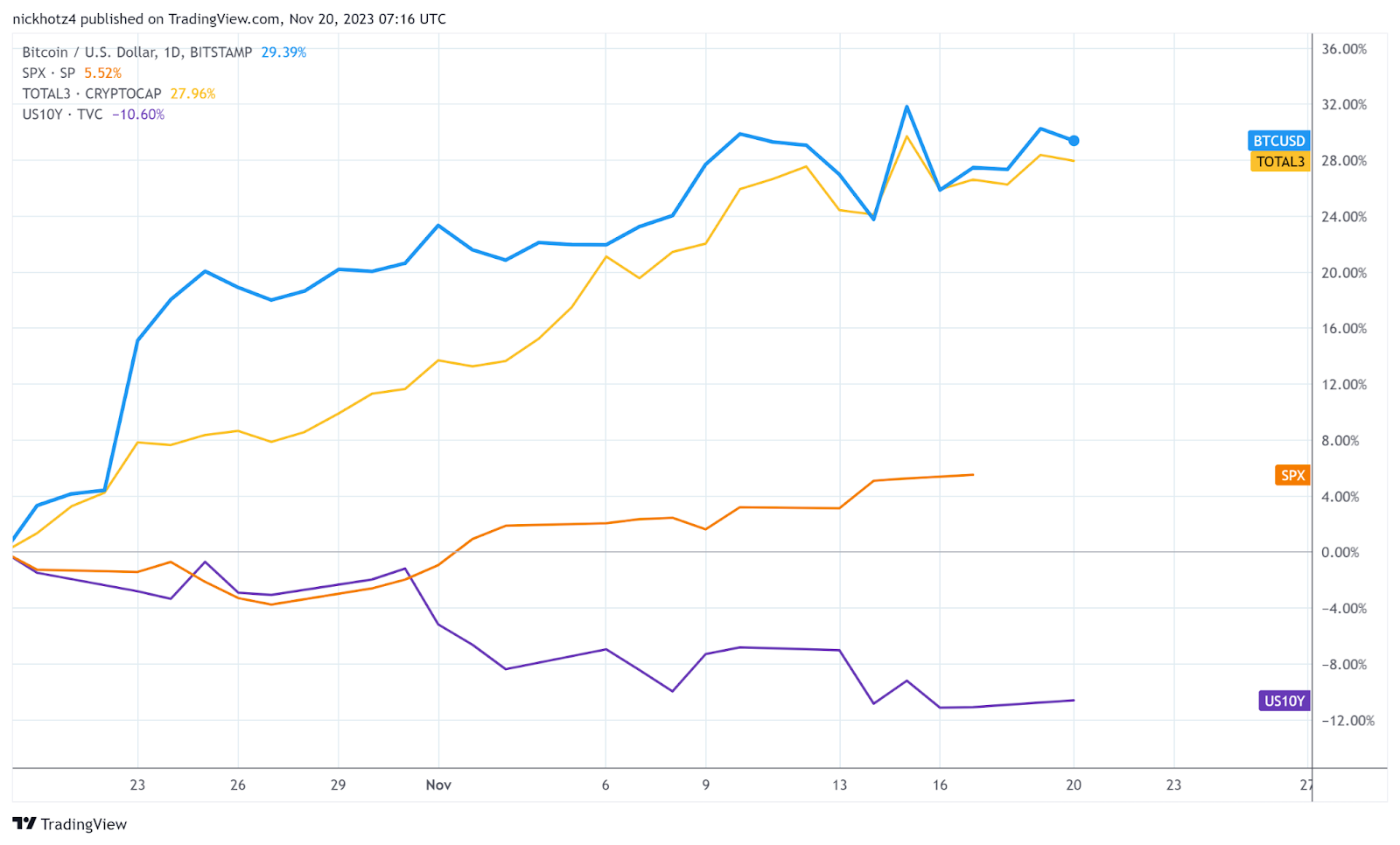

Crypto prices notched a fourth straight week of gains but ended the week on a weaker footing. Equities have also been on a tear recently with the S&P 500 now up 3 weeks in a row and up nearly 8% month to date. Several bank strategists are calling for risk assets to stall in the short-term but consensus has been very wrong all year. Looking forward, we'll get some tidbits of data on the consumer with sentiment and jobless claims numbers out this upcoming week.

It may be a coincidence, but digital assets seem to have, once again, led risk assets off their bottom. While digital assets began their rally on October 20th, macro markets followed a week later when the S&P 500 and government bonds continued to recoup recent losses while the U.S. dollar weakened.

While most digital assets treaded water last week, the dominant narrative moved away from the Solana ecosystem and re-focused on tokens at the intersection of crypto and artificial intelligence (AI).

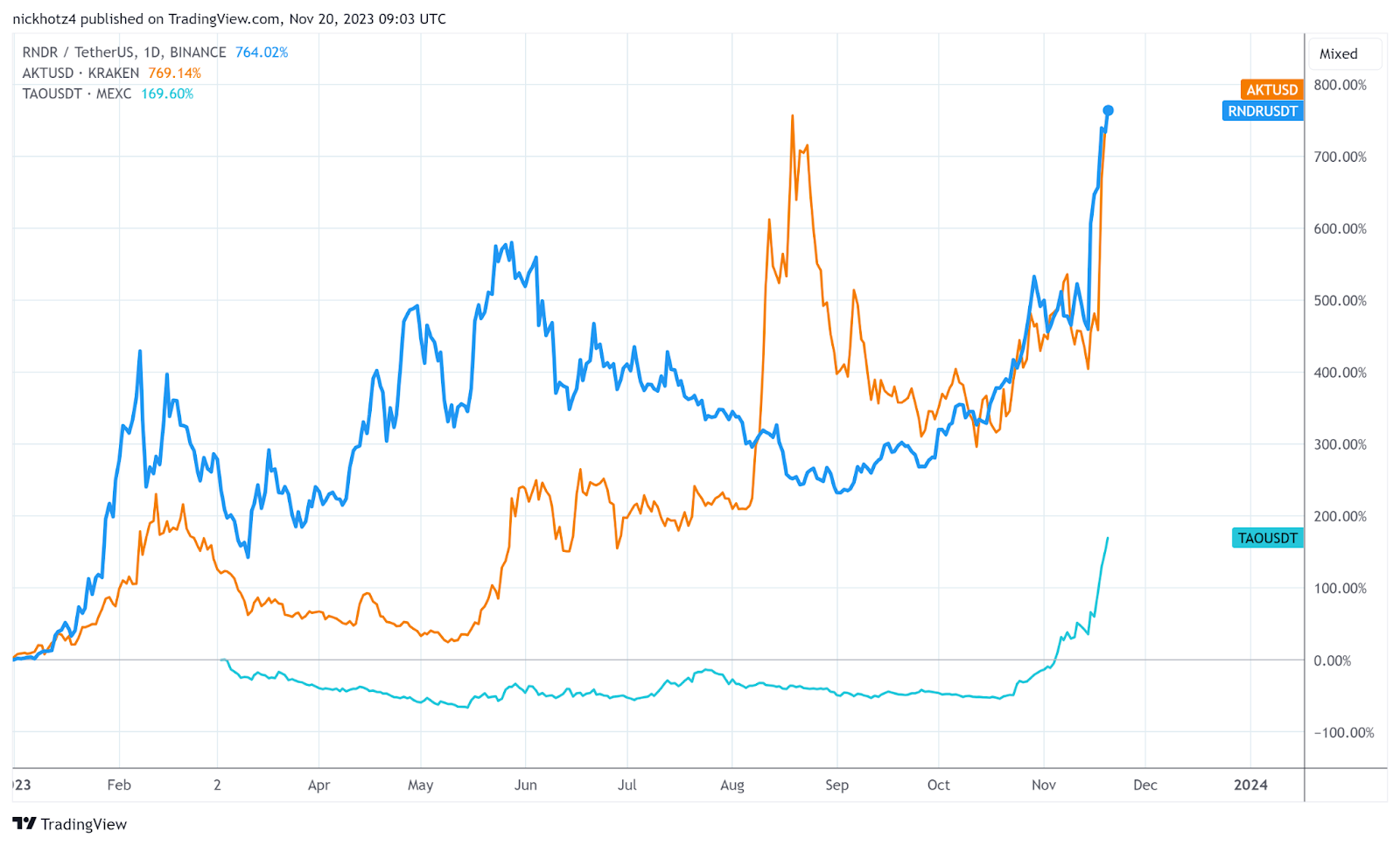

The AI narrative started in January and February after solid rallies in many AI tokens. This narrative breathed in new life this week with the entire sector rallying sharply but specifically led by Bittensor’s TAO (+78%), Akash’s AKT (+55%), and Render’s RNDR (+38%) among the larger capitalization names. Outside of Bitcoin itself, AI has been the one relatively persistent narrative that markets have latched onto this year, with the latter two assets both up over 700% YTD.

Both Akash and Render are marketplaces for computational resources, linking people who have access to CPU or GPU chips with those who need computing power. The “AI” part comes from the fact that the most significant source of demand for high-quality GPU chips is networks looking to train and query AI models. Both projects have recently redirected their efforts heavily towards this AI use case and see a more significant opportunity in this use case than in their original markets of cloud computing and graphical rendering, respectively. We’ll come back to Bittensor a bit later.

Another Bad November For Sam’s

While AI-related tokens had already been performing well, the events from this week, namely the firing of Sam Altman as CEO of OpenAI, kicked this into high gear. The

ongoing saga between the OpenAI board of directors and Altman brought the AI world to a total standstill, as everyone (myself included) turned into soap opera fans hanging on to every development of the drama.

In the Silicon Valley worldview, OpenAI is the new shining pillar of American technological progress, boldly pushing the frontier of one of the most interesting, practical, and potentially dangerous technologies in development today. Sam is considered the new Alexander Graham Bell by some, distributing this powerful technology worldwide to make it available to everyone (*).

And yet, despite the gravitas OpenAI has in the tech world, its connections in Washington, and the blank check access from venture capital firms, the whole concept seems like it might unravel in a single moment.

The reason for this appears to be related to the concept of safety, a term used in AI to describe systems that behave ethically and are aligned with human values. This concern stems from the idea that as AI systems become more powerful (and it seems OpenAI recently made a

big leap forward on this front), there becomes an increasingly large potential for an AI system that is so smart that it can outpace all human intelligence and destroy humanity or, much more urgently, An AI network that teaches humans how to do bad things more easily.

Current reporting states that members of the OpenAI’s board of directors are concerned about AI safety and were increasingly clashing with members who believe either that the company should focus on maximizing profits or those that are “effective accelerationists” who believe it’s in humanity’s best interest to progress AI as fast as possible. The predominant thinking among safety-ists is that centralized control of AI will lead to the safest outcomes - by keeping access from people who can potentially burn themselves with the technology. Warranted or not, the board seems to have used this reason to justify upending the apple cart of one of the most innovative companies of our time.

Bittensor (TAO)

In 2019, two AI researchers experimenting with how distributed computing could improve machine learning outcomes created a new blockchain network called Bittensor. Modeled after Bitcoin, the intent of the network was to use crypto incentives to bootstrap a set of miners who, instead of wasting electricity guessing random numbers (Proof of Work), would compete as AI models to provide the highest quality outputs.

The original text prompt network works much like ChatGPT, with validators proposing queries (e.g. ”Plan a weeklong trip to New York City for me”) to miners, who then provide responses they think are best. The validators then grade miners on their performance based on some rubric (called a reward model in AI jargon) to ensure that the best responses are graded the best. These grades are then sent to the entire network allowing everyone to see how well certain miners are doing followed by the network combining all of these grades into a final score for miners. The A+ miners get a large proportion of emissions of the native TAO token while the D and F miners eventually get kicked off the network and are forced to pay additional TAO if they want to come back.

In 2023, a series of upgrades dramatically expanded the project's scope. The company used only to run the single ChatGPT style prompting network but recently split into several subnetworks. Each subnetwork has the same general framework as the original. Miners compete to provide the best service to validators, validators have some framework for grading miners and relay their rankings to the rest of the network. These are the same basic functions of all DePIN networks. In the weeks since the recent Bittensor Revolution upgrade, subnetworks have sprung up aiming to take on

compute,

storage,

web scraping,

language translation,

time series prediction,

oracles, and doing all sorts of interesting things involving AI models.

To orchestrate the subnetworks, validators throw their voting weight behind ideas they believe can be best monetized or deem important to the network. Subnetworks receive TAO emissions in proportion to how validators voted, with most emissions going to miners on that subnet and a small percentage to the person who created the subnetwork. This makes sure the highest potential subnets get most of the subsidies and also gives an incentive for people to build high-quality subnets.

Bittensor isn’t the first to use crypto incentives to create digital resources. The original was Bitcoin which used BTC tokens to incentivize miners to create secure space on its digital ledger. Others, now known as Decentralized Physical Infrastructure Networks (DePINs), expanded the potential usage into areas like storage (Filecoin, Arweave), compute (Render, Akash), wireless connectivity (Helium), and much more.

The problem for these networks has been two-fold. The first is the lack of demand for a supplied resource. Helium was the unfortunate poster child, directing many of its HNT tokens towards its Internet of Things (IoT) connectivity network, (which doesn’t get much use today)rather than focusing on a much more obviously useful 5G network, which the company has only recently begun to roll out. The second issue is the lack of supply of a resource. Akash provides access to high-quality GPU chips, one of the most highly demanded resources on the planet. However, it has been unable to secure access to more of these chips because the token governance has decided that ratcheting up the token inflation to subsidize new chips on the network would hurt the value of AKT. While securing more GPUs would undoubtedly create a network effect that would benefit Akash, a fall in token value would have the opposite effect and reduce its opportunity to secure more GPUs in the future. These twin issues have been big reasons why the DePIN sector has seen only minor traction thus far within the crypto space.

Bittensor’s incentive system solves both supply and demand problems that have historically plagued DePIN. The demand-side problem originally suffered by Helium is eliminated because validators will only vote for subnets they believe have a monetizable value and quickly stop rewarding ventures that aren’t succeeding. The supply-side problem suffered by Akash is also severely reduced because the aggregation of so many different applications under one token creates a significantly greater network effect and allows more emissions to be fired at promising new applications.

To be sure, Bittensor is still in its infancy. The blockchain is still

run via Proof of Authority where the Foundation controls block production. Many validators simply

copy each other’s homework rather than actually grading the miners themselves. All the live subnetworks are still producing outputs that are either low quality or decent but worse than what centralized alternatives provide (e.g. ChatGPT or DALLE-3).

But the potential is clear. In the six weeks since subnetworks were enabled, 27 have been registered, covering various potential use cases.

Taoshi's time series prediction subnetwork asks miners to predict the price of BTC in 8 hours, rewarding them based on how close they get. The subnetwork is already

distributing more emissions than Numerai, the successful hedge fund run using crypto incentives for machine learning engineers to extract signals from financial data. In the future, these subnetworks can expand beyond Bitcoin to predict not only financial asset prices, but any time series with applications in sports, politics, weather, and much more.

Cortex.t’s subnetwork recently received access

to GPT-4 and DALLE-3, OpenAI’s flagship premium models allow for the production of valuable data from these top-quality models at scale to create something of even better quality.

@replytensor is live on X/Twitter generating images when people tag the account using the image generation subnetwork. Clearly, there is excitement and interest in building on Bittensor, which much of the crypto ecosystem has been starved for recently.

Bittensor imagines a world where the fate of the frontier AI production and safety isn’t at the mercy of a single board of directors, but permissionlessly accessible to and governable by anyone interested. I can think of at least one recently unemployed person who would probably prefer it that way.