Source: TradingView, CNBC, Bloomberg, Messari

Why We’re Buying The Dip

Last week was heading towards “bad’, and accelerated to “awful” over the weekend. What looked like a fairly common and pedestrian -10% weekly decline in crypto markets turned into a -20-30% rout by Sunday night. As always, when a move like this occurs, traders are left looking for answers, and, more importantly, trying to determine if this is an opportunity to profit from.

While you’ll undoubtedly hear rumors that “XYZ fund blew up”, that’s the story you hear every time a big market dislocation happens, and it’s difficult to substantiate until it’s too late (and often not true). What is easier to decipher is what factors led to the carnage in the first place, and whether or not these are long-term changes to the market or short-term dislocations that will soon revert.

So, let’s review each of the 6 factors heavily involved in the selloff that ultimately crushed markets over the weekend and explain why this is looking more like a buying opportunity than a risk-off scenario.

Reason #1: Global macro events

Just about every risk-off signal percolated last week, and crescendoed into Friday. The 10-year U.S. Treasury yield fell over 50 basis points following weak language from the Fed, and softer economic data, prompting Fed Fund futures to price in 100 basis points of rate cuts by year-end. Oil fell almost 5%, the VIX spiked +25% on Friday alone, and at one point in the week, had almost doubled, U.S. equities continued to bleed as the Nasdaq entered “correction” territory, and the Nikkei has now fallen -20% from all-time highs reached just a few weeks ago after the BOJ raised rates, crushing the carry trade as the Yen appreciated versus the dollar.

What is the long-term effect on crypto?

It’s become consensus that the Fed will cut rates in September, possibly as much as 50 basis points. The VIX has been conditioned to retreat from any fast moves higher over the past 10+ years, and we’re still heading towards a U.S. Presidential election which has historically been good for markets post-election. Meanwhile, policymakers in Japan have been trying to get out of deflation for multiple decades, and the government has been encouraging retail investors to buy equities. They can’t afford a massive collapse in equities and a hit to wealth, so there is a high probability that they will blink. Crypto has had a very low correlation to equities over the past 18 months, and while it tends to exhibit more downside beta than upside beta, these relationships are short-lived. Bottom line – this does not seem to be a long-term problem for digital asset investors.

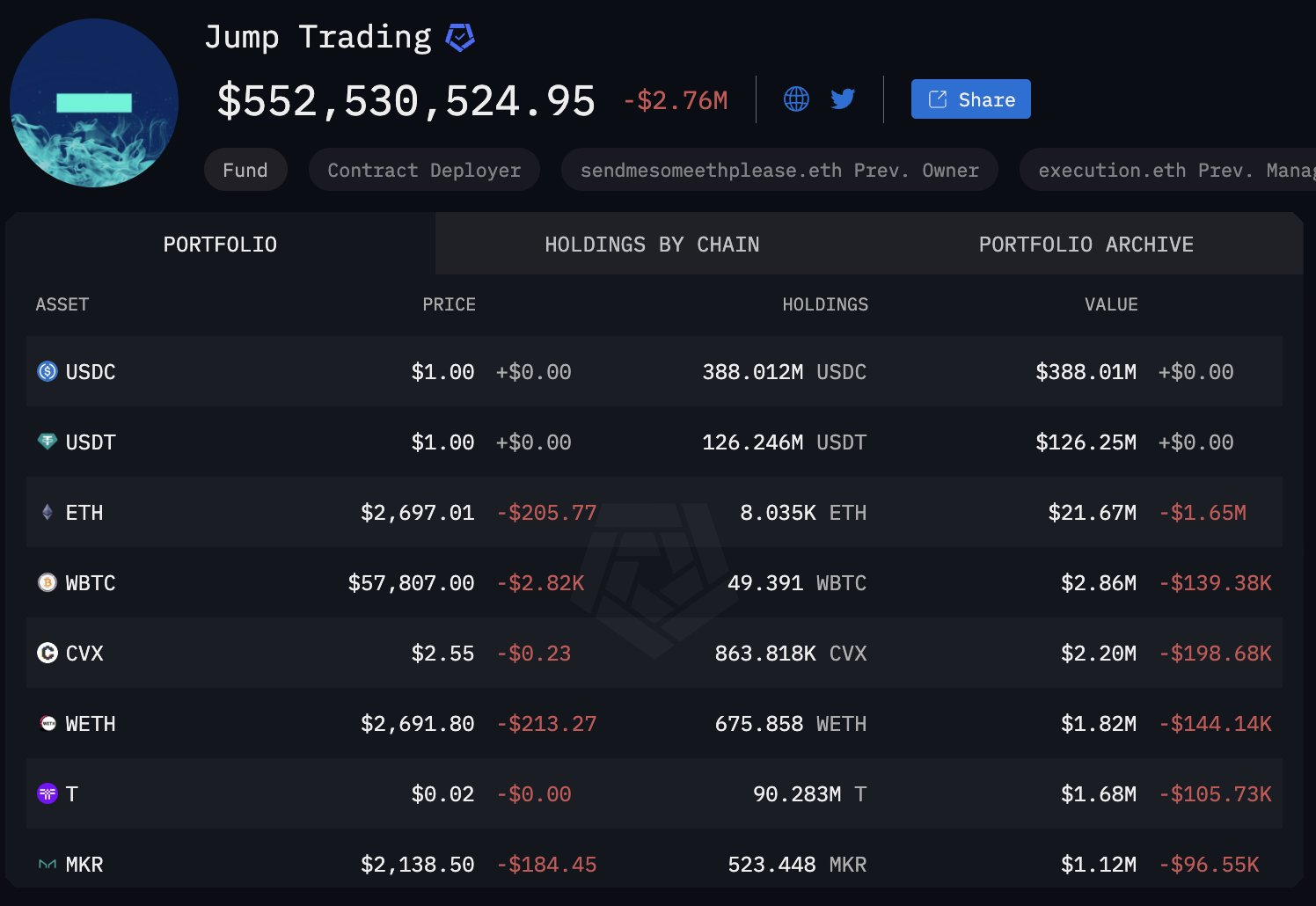

Reason #2: Jump selling ETH

Perhaps the biggest new piece of news over the weekend was that Jump Trading was unstaking and liquidating a big portion of their ETH position, over $500 million worth, on Sunday. Rumors suggest they are exiting the crypto market maker business altogether. But why would they do this on an illiquid Sunday? A few possibilities:

- They are actually unwinding, but this is a forced sale… either by Feds or other regulators, or because they need collateral quickly due to issues in other markets (like the Yen carry trade)

- They fear a massive "Black Monday" like equity dump when markets open Sunday night / Monday and don’t care that they are getting terrible liquidity on a Sunday because they fear it will get worse quickly.

- They saw an opportunity to “stop hunting,” trying to sell into an illiquid market and force futures liquidations to buy back lower. Perhaps they have ETH puts and are pushing the market down to their strikes.

What is the long-term effect on crypto?

If I had to guess, I’d say scenario “b” is unlikely, and this is much more likely to be scenario “a” or “c”. If it’s because Jump is exiting the market, that would likely be a long-term positive for crypto since Jump has been at the forefront of many problems in this industry, but a short-term negative as it sucks even more liquidity out of trading. Regardless, this selling is already over, as 90% of their wallet is now in stablecoins, so any long-term effect would be based on sentiment, not actual flows.

Reason #3: BTC and ETH ETF flows

While ETH ETF flows have been net negative, the trend was moving in the right direction towards the end of last week as Grayscale ETHE outflows were slowing and inflows into ETH ETFs offered by Blackrock, Fidelity, Bitwise, and others were beginning to close that gap. On the other hand, BTC ETFs had net outflows on Friday of $237 million, perhaps due to a rotation trade out of BTC into ETH.

What is the long-term effect on crypto?

The new BTC and ETH ETFs are killing the digital assets market in the short term as all attention and flows are being sucked into this vortex, but it is a necessary evil long term to increase adoption and awareness. Unfortunately, there is no edge here, and the market has been at the mercy of these flows all year, and that doesn’t look to be changing anytime soon. If these flows are the reason for the selloff, it’s a stay away.

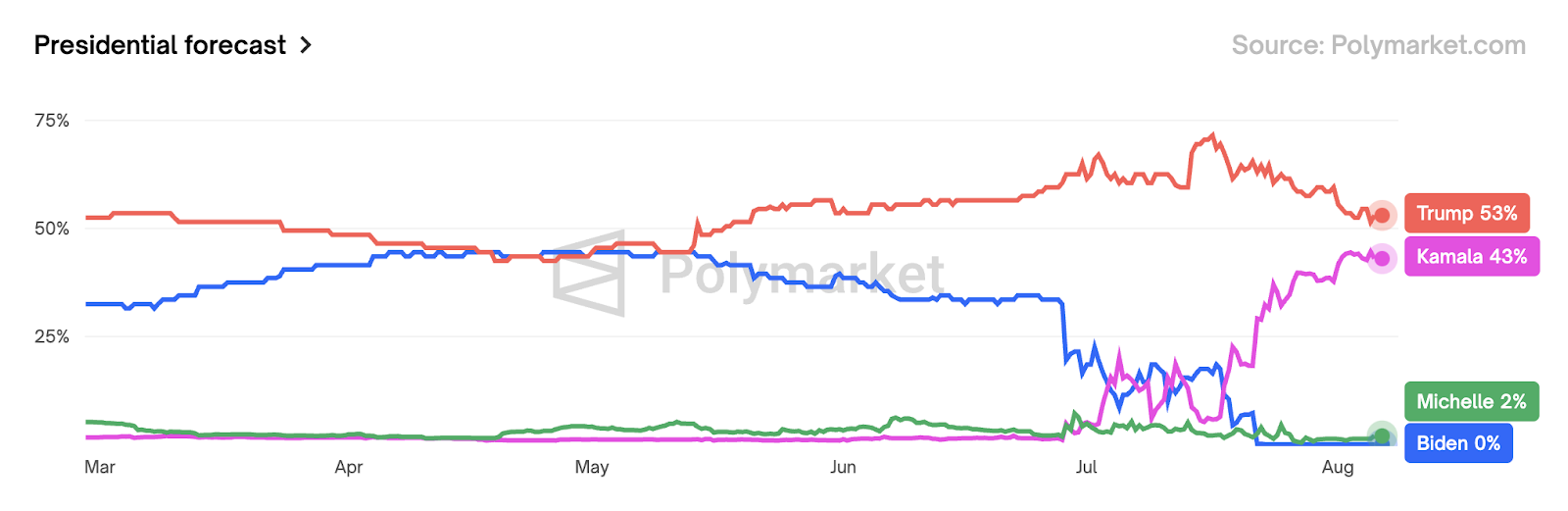

Reason #4: Kamala Harris jumping in the polls versus Donald Trump

While Trump still leads Harris, the gap has been closing quickly. As we’ve discussed for the better half of this year, a Republican victory in the polls is considered very pro-crypto, especially after Trump gave a bullish speech at Bitcoin Nashville last month. Trump announced that the U.S. would have a strategic national Bitcoin stockpile and that billions of U.S. government-owned Bitcoin would not be sold. Trump also announced he would remove SEC Chairman Gary Gensler if elected. Even if Democrats are less evil towards crypto now that they are starting to feel the ramifications of their miscalculations, the entire equity and crypto market favors a Trump win, and as Trump declines, so do markets.

What is the long-term effect on crypto?

This one is much easier. As Harris rises, crypto sinks. While it is unlikely that some of the recent positive U.S. regulatory wins will be unwound if Harris wins, it is almost certain that a Democrat victory will not be as supportive as a Republican victory will be.

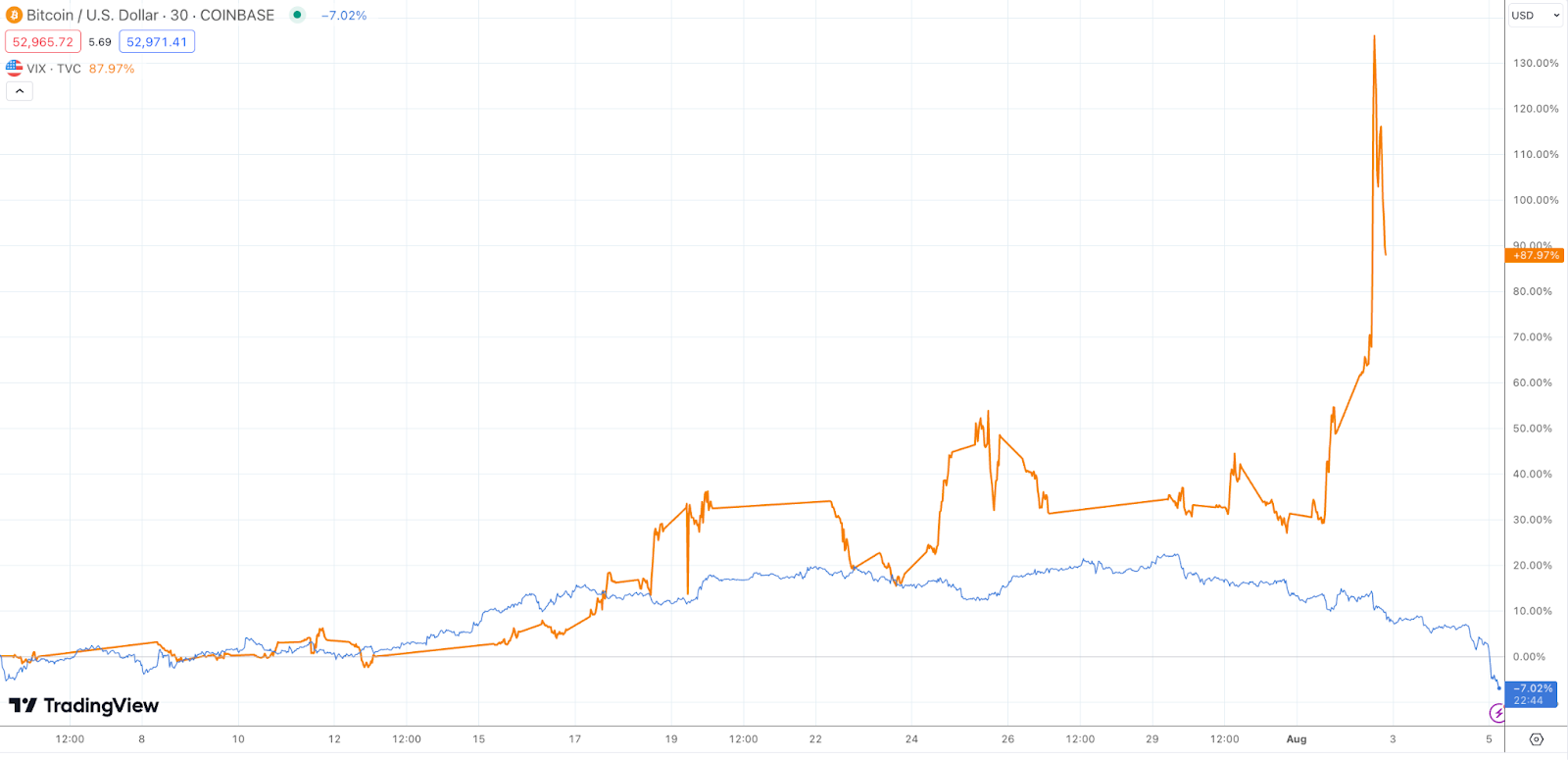

Reason #5: Middle East tensions rising

This is likely to be the least influential factor. While this is always unsettling for markets and a good reason to drive the VIX higher and equities lower, any fear driven by Middle East tensions almost always reverts in days. Plus, if this was really the culprit for global weakness, we would see oil prices spiking, and that is not happening.

Source: TradingView

What is the long-term effect on crypto?

The only relevant factor here is that Bitcoin is once again not acting as a “flight to quality asset” when it comes to wars and political theatre. While Bitcoin has historically spiked when banks or governments fail, it does not spike when geopolitical tensions exist. Bitcoin is a lot of things, but it is not gold, and it is not a fear hedge. The graph below shows the divergence between the VIX and BTC. Further, as more and more institutional investors start to trade Bitcoin, its correlation to other assets actually rises, since correlations often have more to do with WHO owns an asset than WHAT the asset actually is (see Archegos Capital’s seemingly uncorrelated stock holdings).

Source: TradingView

Reason #6: Supply overhangs

This has been a huge driver of markets for the past 4 months, but it’s doubtful that this had much to do with this week’s sell-off. While the Jump Trading ETH sales definitely had an affect, the majority of other supply overhangs are done, or muted. Mt Gox distributions are largely done, Grayscale selling seems subdued, and the German and U.S. government sales from seized assets are over as well. Genesis is now distributing BTC, ETH and SOL in kind post their bankruptcy, but that’s unlikely to be big enough to affect markets in a big way.

What is the long-term effect on crypto?

The actual flows are nothing to worry about at this point, but the continuous front-running of supply still looms over the market. The market is so fragile right now that any hint of selling pressure leads to multiples of actual selling ahead of the forced selling.

So why are we buying the dip? When we break down the factors, there seem to be way more reasons to buy than sell. There are only a handful of tokens in the market that are even positive YTD despite one of the most positive years in crypto’s history from both a regulatory, and fundamental, standpoint. Many tokens are now down -50-75% from the March highs. If you were ever bullish on the market, there’s no reason you should be less bullish today after this week’s events.

It’s been a while since we’ve had a global selloff like this, and the magnitude of this weekend’s events was certainly abnormal but also not unprecedented. We’ve seen similar global macro events where crypto markets were used as the weekend liquidity to front-run selling pressure in other markets (December 2018, March 2020, November 2022), and most were massive buying opportunities.