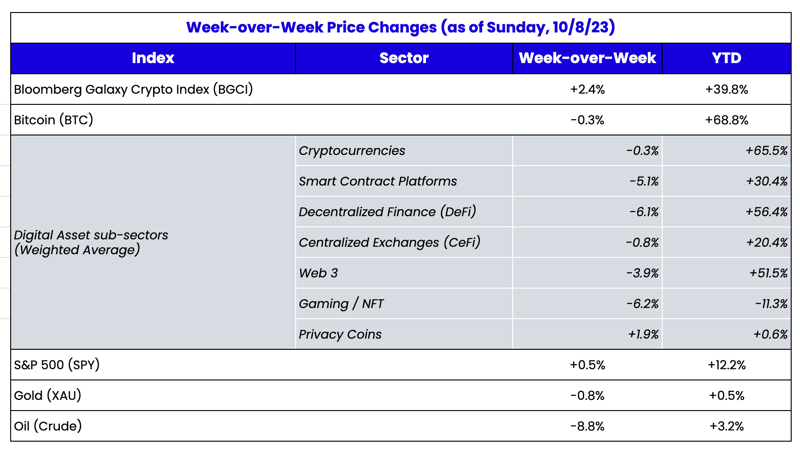

Source: TradingView, CNBC, Bloomberg, Messari

The Wall of Worry Seems So Far Away

Prior to 2022, few crypto traders or investors followed jobs data, CPI reports, or corporate earnings. The correlation between digital assets and equities/bonds was virtually non-existent.

Fast forward to today, and the near-zero correlation is largely true again. As it turns out, 2022 was the anomaly, caused by increased (but short-lived) participation in digital assets trading from cross-asset traders, including the now defunct Alameda Research. As correlations dissipate, some investors have moved back to focusing exclusively on digital asset-specific data, while others are still hanging on to 2022 macro trends.

Source:CoinMetrics

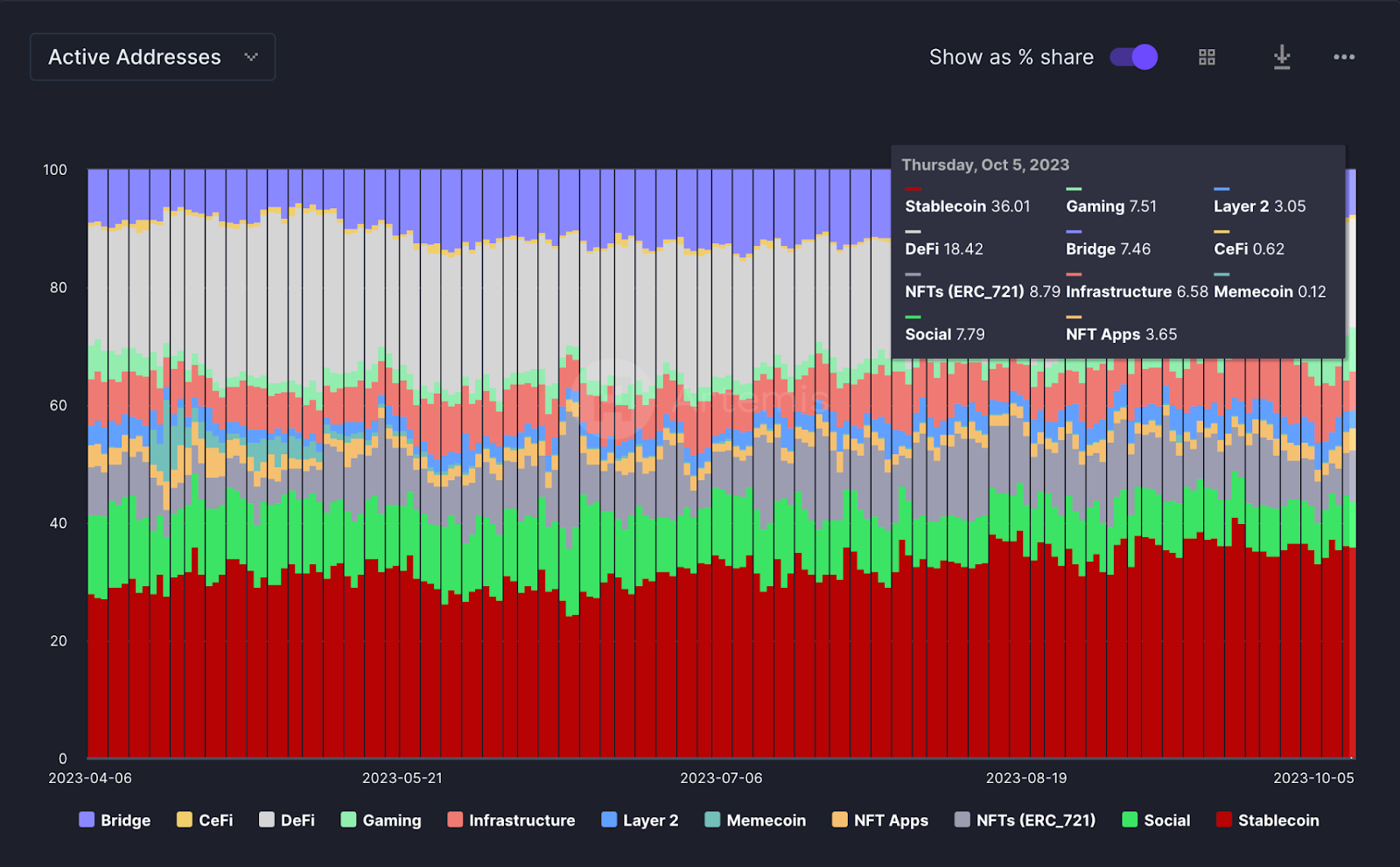

And unfortunately, the digital assets-specific data is not great this year. While the long-term future potential of blockchain seems more inevitable than ever, the current picture remains bleak. The below chart shows overall market activity (by active addresses) across all chains. Stablecoins continue to account for the majority of activity at 36%, with DeFi second at 18%, and likely declining further as DeFi exchange and lend/borrow levels remain at 2-year lows. Social apps only account for 7.8% of activity despite all the recent hype and noise around them. The rise in stablecoin activity relative to other applications continues a trend that we’ve seen since the middle of last year. This is not a bad thing per se, it’s just not terribly innovative.

Source: Artemis

At some point, today’s transaction data needs to start matching both the historical levels and the future expectations. Coinbase recently put out an infographic showing how

America loves crypto. It’s filled with data that paints a rosy picture today but mostly uses lifetime aggregate data. It basically tells a story that most people own some crypto, and have tried to use crypto at some point, while today’s data shows that few are actually using crypto today. The industry definitely needs a spark.

At times throughout history, geopolitical tensions have created these sparks. So with the news of the sad and terrifying Israeli/Palestinian war this weekend, the question (purely from an investing perspective), is will this matter? Will any 2022 historical parallels be repeated, or will the reaction once again be unique?

In February 2022, the Russia/Ukraine war began. Obviously there was a different investment sentiment in early 2022 versus now, but there may be some takeaways. It looks like the war officially started on 2/24/22 and BTC popped almost 30% over the next few days (ETH had a similar performance). Could the same happen here with Israel? Maybe. Certainly, macro investors will look to make this connection.

But how much of the Bitcoin and Ethereum price moves in late February 2022 can actually be attributed to the Russia/Ukraine war itself? I wrote the following at the end of February 2022. Re-reading my own thoughts from a year-and-a-half ago makes me think the price move had more to do with the Russian sanctions than the war itself. From our February 2022 investor letter:

“In February 2022, we learned that money is no longer an asset you own; instead, it is a liability owed to you by a bank, brokerage, or government that may or may not pay. Digital assets rose +3-10% in a month during which:

- Canada sanctioned its own citizens.

- Russia caused complete financial ruin to its economy.

- The U.S. and Europe made a mockery of the financial system by handpicking which assets individuals could invest in and which banks could be utilized. This was a watershed moment for the current and future adoption of digital assets.

Bitcoin initially crashed following the first news of Russia’s invasion around 3:00 UTC on Thursday, February 24th, dropping from $37K to as low as $34.35K. But less than 24 hours later, BTC regained its previous price and began to move up to its highest level in weeks. On Saturday, February 26th, digital assets didn't react at all to Russian bank sanctions until almost 24 hours later when FX markets opened, causing Bitcoin to drop over 5% on the Sunday night open. The digital assets market was open first, and everyone had all the opportunities in the world to sell but didn’t until the cross-asset quant/macro desks got involved. The tail was wagging the dog. Upon the U.S. open on Monday, digital assets ripped higher again. “

You would expect equities to be a hair weaker this week, and Treasuries may regain a bid due to the uncertainty and fear. Gold and Bitcoin should get a bit of a bid as well, and oil… well, who knows?

I’m not sure any of the events this weekend will ultimately matter for digital assets. That is unless banks and governments once again join the war by restricting payments and money flows. Regardless of where you live, when you go to bed tonight, you can be certain that your Bitcoin or Ethereum, held in a self-custodied wallet, will still be there when you wake up. If you live in a geopolitical hotspot, or in a region that is about to be tied up in this war, I’m not sure you can confidently say that.