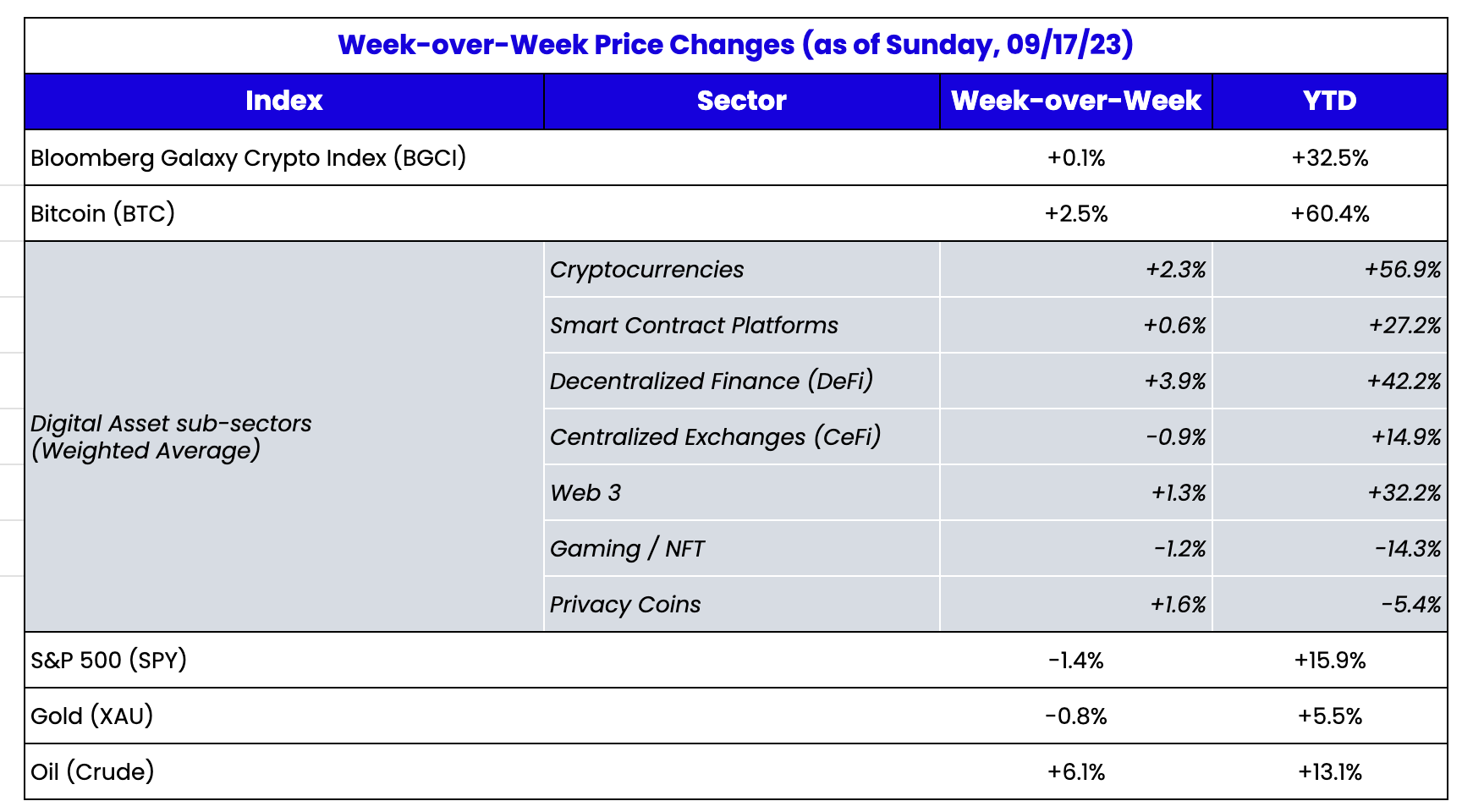

Source: TradingView, CNBC, Bloomberg, Messari

The Wall of Worry Seems So Far Away

Financial markets are nervous. And possibly for good reason. There are a lot of warning signals in the market. The problem for investors is that none of these obvious and potentially big negatives seem likely to happen immediately, which means, they may not actually happen at all.

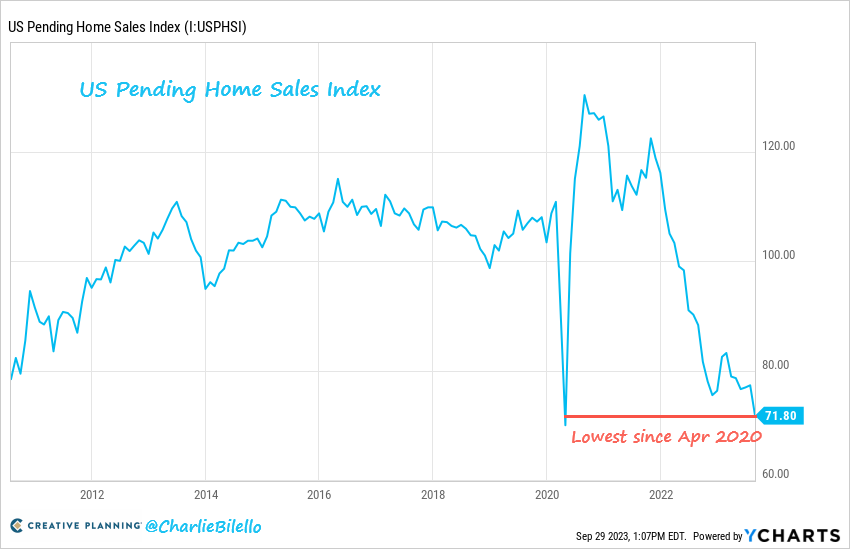

Take the housing market. Pending home sales in the U.S. are at their lowest level since April 2020, when much of the U.S. economy was shut down. The housing market is frozen. High rates make housing largely unaffordable for new buyers, but it’s also unaffordable for people to sell because nearly every existing homeowner was able to refinance their existing mortgages at record-low rates between 2018-2022. Couple that with high employment rates and a work-from-home culture, which makes the need to move low, and, in turn, limits the effect of rising rates. Is the housing market a problem? Yes. Will it have any near-term effect? Unlikely.

Take the bond market. The Total U.S. Bond Market ETF (BND) had a negative return over the last 7 years. The 10-year U.S. Treasury yield has nearly tripled over this time period, resulting in the longest bond bear market in history (38 months and counting). All of these bond investors currently underwater must be in trouble right? Well, most bond market buyers don’t mark-to-market. The Federal Reserve, global central banks, U.S. banks, insurance companies and mom-and-pop boomers don’t have to realize these losses. Further, like homeowners, most corporate borrowers have locked in lower rates on their debt, kicking any refinancing issues at higher rates out to 2025-2027. Is the bond market a problem? Yes. Will it have any near-term effect? Unlikely.

You can climb the entire “wall of worry” from inflation to government shutdowns, to debt spirals, to rising healthcare costs, to social security, and come to the conclusion that all of these well-known problems are, in fact, huge problems that should not be ignored. However, these problems also carry a very low probability of near-term timetable for comeuppance. Some may move to cash for years and wait it out. But, many others will continue to invest in the same manner they have for decades, knowing that over the long term, they will likely make money even if some of these issues become bigger problems.

Last week, U.S. Stocks and bonds struggled, yet again, amidst the newest problem - an imminent government shutdown. But per the above, at the last minute, the crisis was averted with no long-term plan, but yet another short-term “kick the can down the road” solution. Notably, the digital assets market shed its recent downside beta to stocks and rates and held pretty well despite the declines in bonds and stocks. At the time, it felt like this was directly related to the impending government shutdown. Any time the general public loses confidence in banks or governments, Bitcoin, specifically, tends to rally. But then the crypto market rallied even more over the weekend after the shutdown aversion. This also may have been obvious in retrospect, since the government shutdown was averted over the weekend, and Bitcoin and Ethereum are the only liquid “risk on'' investments that can be entered in reasonable size over a weekend. Either way, the strength of digital assets last week was apparent when the market didn’t go down, days before it actually went up.

It’s more difficult than ever to pinpoint the exact drivers of gains and losses in the digital assets market. With low liquidity, low volatility, and lower participation in the market, each broad market move can just as easily be explained by market setup than by any near-term or long-term factor. A lot of shorts had built up recently, and those were liquidated this weekend on the move higher. Ultimately, it continues to feel as if there are no more natural sellers other than a few bankruptcy estates and tokens with heavy inflation / unlock schedules. But there are also very few reasons why new buyers will emerge. Perhaps the marginal new buyer related to an impending government shutdown was all the market needed.

It remains to be seen whether the myriad of global market concerns comes to fruition before more buyers return.

Tokenomics - A Misunderstood Art

By Christoper Macpherson, Analyst at Arca

Digital asset participants have had A LOT of time in this crypto bear market to reflect on the two previous bull markets in 2017 and 2020. The recovery from 2022’s terrible year has taken far longer than we all hoped. Most investors are spending their time discussing what needs to happen for the health of the market to return. The most powerful tool in an investor’s tool belt is the ability to thoroughly understand the history of markets. But one major topic that was ignored in the previous two bull market cycles must be addressed: the extreme importance of basic supply and demand economic balance for tokens (known as tokenomics). Not many people have gone in-depth on this topic, but once you understand how token design drives value accrual, you can see a bright future for digital assets – if addressed properly. To recap, most people believe that the 2022 bear market was caused by:

- The idea that the nascent digital assets market naturally works in extreme temporary boom or bust cycles as greed intersects with profit

- Fraud/hacks/scams such as FTX, Luna, 3AC, etc caused exogenous cascades of selling

- Capitulation from participants who were once excited about the potential of blockchain technologies but now have left due to preference to avoid points 1 and 2

Sure, the above points are contributing factors that triggered the price decline. However the bear market has persisted well into 2023 because of poor tokenomic designs, which is also taking a long time to reverse course. The vast majority of digital asset participants still do not have a basic understanding of token design and its importance to our current market dynamic. Why is that?

- Market euphoria is blinding to even the most knowledgeable investors. In 2017 and 2020, professionals and amateurs alike were making triple-digit returns by simply being in the market and buying the hot new thing. The history of markets teaches us that in these situations, people do not stop to think deeply about underlying fundamentals. At that time, there was so much opportunity to make money that hunting for the newest DeFi farm felt like a better use of time than deeply analyzing a 50-page token whitepaper to understand how the token accrues value. The thought of “being early” far outweighed logical thinking and basic supply/demand considerations.

- The concept of tokenomics is still relatively new. The observable history of equities spans centuries and hundreds of thousands of assets. The world, post-Graham, Dodd, and Buffett, generally has a good understanding of what drives the value/price appreciation of equities. Meanwhile, most still struggle to understand how Bitcoin and Ethereum work, yet alone how they accrue economic value. In previous crypto cycles, altcoins generally appreciated in value in tandem with Bitcoin and Ethereum despite their value propositions being very different.

In equities, it is very straightforward that holding a stock is holding true ownership in that company. Tokens are different because they grant the holder various sources of utility and financial value. In the long term, the price appreciation of a token is the result of the majority of participants making the conscious decision that they should use/hold a token (and maybe buy more) rather than sell. Price decline of a token is the result of the majority of participants making the conscious decision that they would rather hold a different asset. Pretty straightforward. New inflows and outflows also drive price action, but in the long term, flows are a second-order effect stemming from the true value and global significance of the tokens and protocols that make up our sector. Despite having utility, tokens are ultimately an investment, and therefore, classical rational investor logic applies. So understanding where supply and demand are coming from, as well as which designs are most compelling, is the first step in understanding how rational investors are behaving.

Sources of token supply:

- Initial token sales

- Airdrops

- Rewards for validating a network/protocol

- Rewards for using a network/protocol

- Token unlocks

- Staking rewards

- Grants

Sources of token demand:

- Governance voting rights

- Requiring users to hold X amount of a token to interact with or validate transactions for a protocol

- Sharing of revenue/profit generated by the protocol

- Speculative belief that a token is fundamentally undervalued and price will be higher in the future (this is a source of demand, but it is not something that can be built into a token’s design)

Our market has come up with many creative ways to design supply-side tokenomics, but demand-side economics have largely been underappreciated. Let's use an example to illustrate how the two dynamics interact. Let's say a new derivatives exchange comes to market, and it releases a token whose main design is to reward users for trading on their exchange - i.e., you earn the token IF you trade on the exchange. This design has solved for how the token will be distributed (supply) but has no demand dynamics. When a user receives the token, they then must make a decision: Should I continue to hold this token or would I rather sell it? If I choose to hold, what utility am I being granted? Is the value of that utility worth the risk of holding? In the absence of perceived utility (demand), the rational investor will choose to sell the token at this junction unless they have a generally bullish view of the market going forward. In this bear market, investors have not had forward-looking confidence in the market, so they continue to sell when the decision is presented to them. Protocols such as Uniswap, dYdX, Aave, Blur, and many others have shown that it does not matter how popular your protocol is or how significant it is to the world. In the long term, the price of the token will continue to trend lower without compelling demand side tokenomic design.

So we have established that demand-side tokenomics are necessary. But which of the demand sources are best? There are countless data points that show tokens whose demand side design tokenomics are solely governance voting rights are not compelling enough in the long term. If you truly cared about an upcoming governance vote, why not just buy the token the day of the vote, and sell it once the voting period ends? And will the vote even matter in the end if large investors (early VCs) or the team themselves hold the majority of the votes? Pure governance tokens will always lose. Token holding requirements for validating or using a protocol is a legitimate use case, but users will only continue to hold the token for as long as they need or want to use your protocol. The most fundamentally compelling design for demand is revenue/profit sharing (e.g. RLB and UNIBOT), but most token issuers are concerned in 2023's regulatory environment that this will make their token an unregistered security. It is difficult to reconcile that the best way to design a token that benefits investors is in direct conflict with U.S. current securities law. This dynamic also affects NFTs greatly and has likely caused more value destruction in our space than the collapse of FTX. True investor protection is being held up by the abstract interpretation of a broad securities law created in 1946... a period of time when color television, the world wide web, cell phones, AI, and blockchains did not exist. Frankly, most of these technological revolutions were unthinkable for humans in that time period.

In addition to the realization that poor token design has a compounding negative effect in bear markets, token inflation is now causing bearish conditions to persist further. For example, Layer 2 protocols are generally accepted in the community as the layer on which most consumer applications will be built in the future. With the releases of the Optimism (OP) token and Arbitrum (ARB) token in 2023, one would assume that the massive growth of development and usage of these L2 protocols should generally lead to price appreciation. But ARB and OP are down ~60% and ~51% from all-time highs, respectively. These tokens are designed as pure governance tokens, and both are inflating their circulating supply by over 300% in the next 365 days. If demand tokenomic design is not enhanced and/or the market as a whole does not turn bullish, it will not matter for price that L2s are extremely important and growing. The inflation will be overwhelming.

So yes, there is a lot of doom and gloom currently. But in the future, token design has to improve, inflation schedules have to slow down, and current regulatory roadblocks have to be lifted in order for major institutional capital to enter this space. They likely will scramble to allocate into every top 10 market cap token once the regulatory pendulum swings. Tokens issuers that do not attempt upgrades to tokenomics will be left behind, and tokens that remain as governance-only or reward-only tokens will underperform further and will likely die slowly. Some tokens with bad designs will still go up temporarily in a bull market, but there will be no long-term value if true demand side tokenomics is not addressed. Crypto-native participants will have an edge in generating alpha if they spend time understanding how the digital asset sector works.