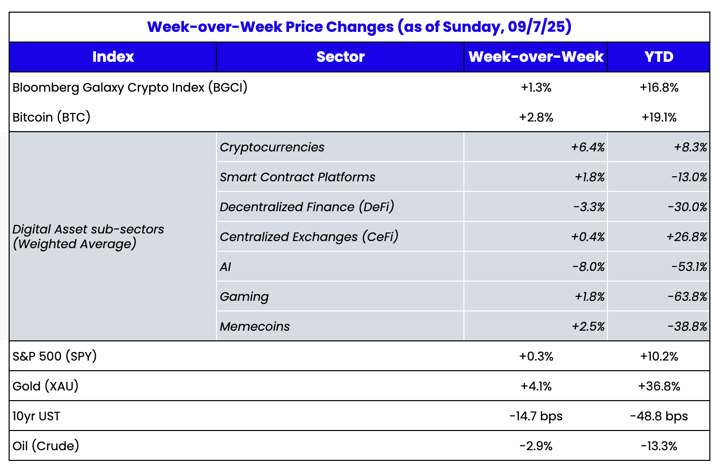

Source: TradingView, CNBC, Bloomberg, Messari

This week's edition is written by David Nage, Portfolio Manager at Arca

The "Red September" Myth Is Missing the Forest for the Trees

As we enter September, crypto Twitter is buzzing with the usual seasonal FUD. "Red September," or "The September Effect," has haunted markets for nearly a century, with Bitcoin falling an average of 3.77% each September since 2013. Since 2010, the largest cryptocurrency by market capitalization has posted an average loss of 4.5% in September, according to data from Glassnode and ETC Group. On the other hand, the S&P 500 SPX has generated an average monthly decline of 1.2% and ended higher only 44.3% of the time dating back to 1928, according to Dow Jones Market Data.

Yes, September has historically been challenging for risk assets. But what many seem to be missing is that we're operating in a fundamentally different market structure than we were even 12 months ago. The same crowd that religiously follows seasonal patterns somehow ignores the data, cited by Binance in August this year, that the number of publicly traded companies holding Bitcoin doubled in H1 2025 compared to 2024.

For years, we have opined about Bitcoin relative to other assets in the industry. For years, participants around the world have tried to put Bitcoin into one singular box: “it’s digital gold”, “it’s a hedge against inflation”, “it’s a store of value”. We have suggested this in the past as well, but what if Bitcoin is all of those things? What if Bitcoin is also like insurance against global fiscal calamity?

Insurance premiums fluctuate; hurricane insurance costs more during active storm seasons, less during calm periods. Similarly, when the Fed appears responsible (rate cuts to support growth), insurance premiums (in this analogy, Bitcoin) can decline rationally, and the inverse as well.

Look Around the Corner

While certain market participants obsess over historical September performance, the actual infrastructure supporting digital assets continues to mature at a considerable pace. This past week provided a perfect example: U.S. Bancorp, the fifth-largest commercial bank in the United States, has resumed Bitcoin custody services for institutional clients, reopening a product it first launched in 2021 but suspended in late 2022 during heightened regulatory scrutiny.

This isn't just another bank dipping its toe in digital asset waters. U.S. Bancorp's move follows the SEC's rescission of Staff Accounting Bulletin 121, which previously required banks to carry custodial crypto assets on their balance sheets. The Minneapolis-based lender will now also provide custody for spot Bitcoin exchange-traded funds (ETFs), reflecting institutional demand for secure handling of Bitcoin funds managed by firms like BlackRock and Fidelity.

Think about what this represents: a top-5 US commercial bank not only re-entering the digital assets custody space, but expanding to serve the ETF ecosystem that didn't even exist when they first launched custody services in 2021. Simultaneously, we're seeing the first blockchain-based prediction market, Polymarket, receive full CFTC regulatory clearance. This is infrastructure building in real-time, across multiple verticals.

More importantly, the ETF ecosystem that everyone took for granted after the initial Bitcoin ETF euphoria is proving its staying power. Even during recent consolidation periods, BTC-spot ETF issuers continued to increase their holdings, with BlackRock becoming the second-largest holder of Bitcoin after Satoshi Nakamoto. When the largest asset manager in the world is accumulating during "weakness," perhaps that weakness isn't quite what it appears to be.

Where Do I Wire?

While all the jostling is happening, from the Fed to new L1s being created by Stripe & Paradigm, early-stage start-ups are still getting funded in this market.

In the last two weeks $440M has been allocated to 52 start-ups during what is notoriously one of the slowest parts of the allocation cycle, the end of summer. We also continue to see M&A run at a healthy clip, with Kraken purchasing Breakout, Solowin buying AlloyX for $350 million, and RedStone acquiring Credora.

The Road to Recovery: What History Suggests, A Follow-Up

I wrote this in February after the new administration took over: “The 1981 experience provides a potential roadmap for crypto's recovery. The Reagan market began finding its footing after 6-7 months, when:

Policy implementation began to materialize:

- In August 1981, President Reagan signed the Economic Recovery Tax Act of 1981, which brought reductions in individual income tax rates, the expensing of depreciable property, incentives for small businesses, and incentives for savings.

- Market structure adjusted to new realities

- Institutional investors' sentiment improved, highlighted by a record-setting IPO market

What has occurred in the last six months as it relates to crypto and policy implementation? A lot:

- January 23, 2025: Executive Order on Strengthening American Leadership in Digital Financial Technology - This order rescinded previous Biden-era crypto policies, established the President’s Working Group on Digital Asset Markets to develop a federal regulatory framework, directed agencies to compile all existing crypto-related regulations, and prohibited the creation of a U.S. central bank digital currency (CBDC).

- March 6, 2025: Executive Order on Establishment of the Strategic Bitcoin Reserve and United States Digital Asset Stockpile - Directed the creation of a U.S. Strategic Bitcoin Reserve solely for Bitcoin and a broader digital assets stockpile for other assets, ordered the federal government to halt all Bitcoin sales, explore ways to acquire more Bitcoin in a budget-neutral manner, and limited acquisitions of other digital assets to those from forfeitures or penalties.

- April 10, 2025: Signed H.J.Res.25 into Law - Approved a Congressional Review Act resolution disapproving an IRS rule on gross proceeds reporting by brokers for digital asset sales, effectively excluding decentralized finance (DeFi) exchanges and other crypto entities from certain tax reporting requirements.

- July 18, 2025: Signed the Guiding and Establishing National Innovation for U.S. Stablecoins (GENIUS) Act into Law - Created a federal regulatory framework for payment stablecoins with a state pathway option, requiring 1:1 backing with U.S. currency or short-term liquid assets, monthly public disclosures of reserve compositions, strict marketing rules, anti-money laundering compliance, and mechanisms for seizing or freezing stablecoins in response to illicit activities.

- July 30, 2025: Released Comprehensive Crypto Policy Roadmap - Unveiled a 160-page report from the President’s Working Group on Digital Asset Markets, urging the SEC and CFTC to provide regulatory clarity on issues like registration, custody, and trading; calling for congressional legislation to integrate DeFi into mainstream finance; and recommending modernization of anti-money laundering rules to combat illicit finance in crypto networks.

The Bottom Line: September 2025 may go down as the month when institutional digital asset adoption shifted from narrative to reality. While retail traders position for historical seasonal weakness, we're witnessing the convergence of regulatory clarity, institutional infrastructure maturation, and systematic capital deployment. From U.S. Bancorp's custody expansion to $1.7 billion in corporate treasury allocations, from Polymarket's CFTC approval to $440 million in venture funding during summer's end—the infrastructure being built today will define the next decade of digital asset adoption.