In our minds, price and value are intrinsically linked. This only holds true in a world where price is calculated in a stable currency. The current easy-money environment raises unsettling questions about what is real. Blockchain technology and cryptocurrencies offer a possible solution.

The renewed volatility in traditional financial markets coupled with broader societal trends has made me look for connections and correlations. There is mounting evidence we are at a turning point in some of the dominant narratives that have been guiding society overall — and the financial markets in particular. The excellent Epsilon Theory has a post You Are Here suggesting that the investment zeitgeist is changing in three major ways:

Identifying and capitalizing on these changes in zeitgeist are how fortunes are made or preserved. It is these shifts in broad societal mood and understanding that cause large movements in asset prices and swings in poles of power.

Below, we will evaluate these broad shifts through the lens of blockchain and how current trends indicate that this is a particularly opportune time for blockchain to shine as an asset class.

Trend #1: Deflation to Inflation

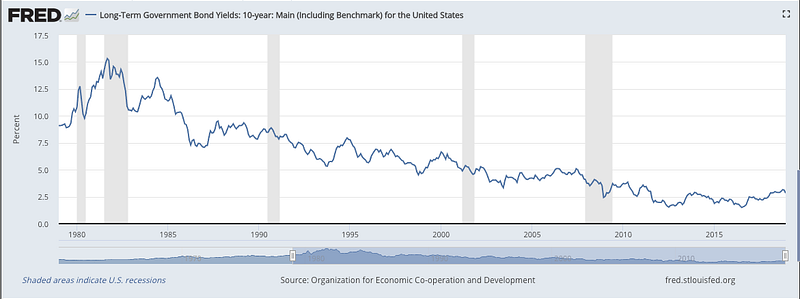

For decades, we have been in a deflationary environment. A fairly good indication of long term inflationary expectations is the yield of the long bond- but this has been relentlessly falling nearly four decades as shown in the graph below.

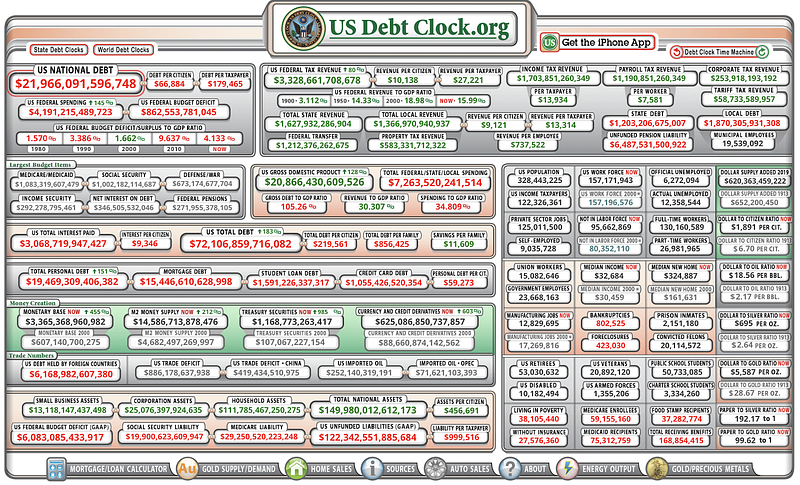

With lowered interest rates, we have seen an explosion in every form of debt. The always sobering Debtclock shows us where the US stands in terms of its federal obligations:

There are many worrisome numbers, but the one I want to focus on is the $122 trillion in unfunded liabilities. That is 564% of fiscal 2018 GDP. If we paused every other government expenditure, including the accumulation of interest, and devoted 10% of GDP to pay that down, it would take 50+ years! Additionally, pay attention to the section on money creation:

From 2000, all figures have increased multiple hundreds of percentage points. At some point, reality will catch up to us and the proverbial piper will have to be paid. And the only way to repay this will be through an incredibly debased currency.

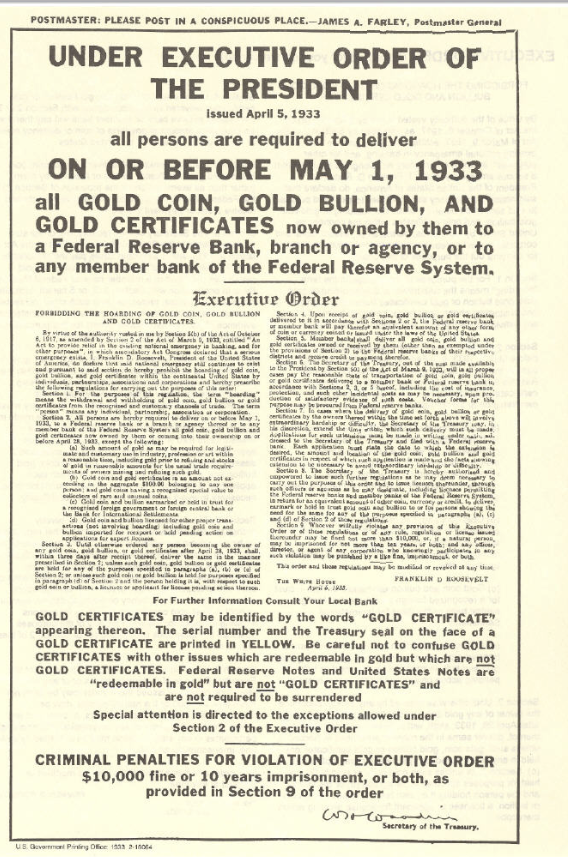

This type of inflationary, central bank-debased currency environment is what Bitcoin was designed to address. Bitcoin was created to be a store of value with all the convenience of a digital asset, without the drawbacks of inflationary, centrally controlled fiat currencies. Before Bitcoin, the de facto store of value was precious metals, particularly gold. Recent government actions, such as freezing of Venezuela’s gold suggests that some of their theoretical “safe haven attributes” are coming into question. By contrast, cryptocurrencies, secured correctly, are unseizable.

Even more importantly though, the major central banks messaged that they would intervene to unlimited lengths and the markets believed them. Epsilon Theory has two fantastic posts on the communication theory of Central Bankers, Risk Analysis in the Golden Age of Central Bankers and The Silver Age of the Central Banker. In these two pieces (amongst others), Ben Hunt outlines how the communication strategies of central banks have been the most important factors for markets over the last decade.

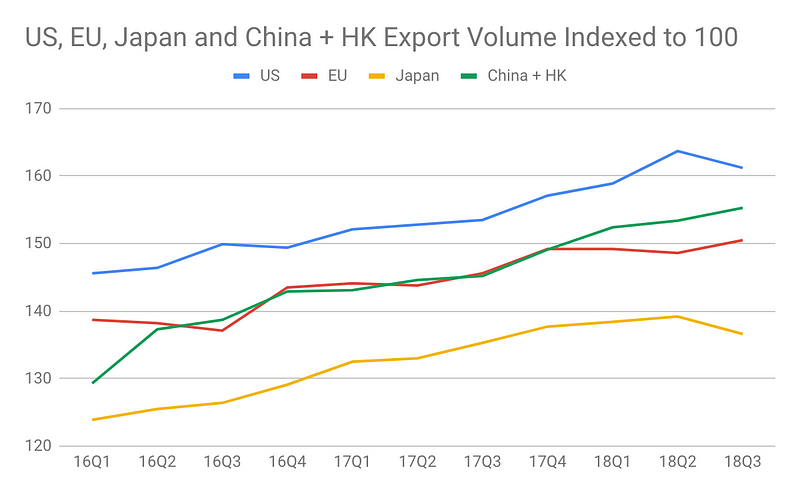

But what now? We have seen the collapse of international cooperation. The US is in a costly and chilling trade war with China. The free trade agreements such as NAFTA are coming under fire. Global trade volumes from the four economic powerhouses have begun to roll over:

Central bank policy has also begun to diverge. Jerome Powell, the most recent appointee to the Chairman role of the Fed, has embarked on the first policy tightening cycle since the great recession. This action is widely blamed for the global asset price decline at the beginning of 2018 and the US Equity collapse in Q4 2018. He has already had to beat a hasty retreat in the face of this violent market selloff. It remains to be seen if Powell will be able to do enough, or, more importantly, if the market believes he will do whatever it takes.

These developments are important in regards to crypto and blockchain because they expose the fragility in the system as it currently stands. US equities were down 20% in November to December of 2018, only to come roaring back for the best January in history, all on the utterances of one man (Powell). Is this honest price discovery? Crypto and blockchain have had wild swings in value, but we must not forget the ecosystem is only 10 years old with $200 billion in total market cap vs the traditional financial system that is 100+ years old with a $300 trillion total market cap. Right now crypto is being moved around in the much greater financial ocean but it serves as a potential answer to the larger problem of the movement of hundreds of trillions of dollars in value being dictated on one man’s comments.

Few have been as vocal or as transparent as Trump, but most would admit that all markets to some extent have become political tools. This causes all sorts of distortions as they are no longer means of honest price discovery and are bent to serve the will of elites. At the epicenter are the central banks that control interest rates and money supply, the most important being the Federal Reserve, as the US dollar serves as the world reserve currency. When these actions become too transparent, the manipulation too obvious and the activity is no longer beneficial to the majority of players, one begins to see disruptions in the system. We are seeing evidence of this all over, not just in the financial system. Populism and nationalism are one the rise and there has been a fracturing of the body politic. These trends are global and increasing.

Again, this environment favors crypto and blockchain as it is designed to be resistant or impervious to central control. While the technology and ecosystem are young, the promise of removing these political influences from markets is attainable through the implementation of this technology. It is the first viable solution to the centralization problem that sophisticated systems seem to demand in order to operate efficiently.

Then the Gods of the Market tumbled, and their smooth-tongued wizards withdrew

And the hearts of the meanest were humbled and began to believe it was true

That All is not Gold that Glitters, and Two and Two make Four

And the Gods of the Copybook Headings limped up to explain it once more.

This is where blockchain and crypto shine. A technology that allows everything to be publicly verifiable, unalterable and unable to be manipulated. The true antidote to a world awash in empty words and IOUs from bankrupt governments.

.png)