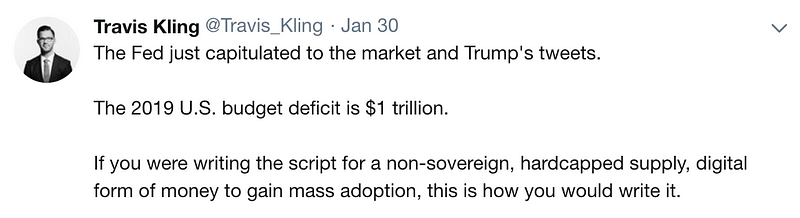

After posting their worst December in 87 years, stocks bounced back in spectacular fashion in January as the S&P 500 Index rose 2.0% last week to finish January 8% above its year-end closing level. The stock market has now gained 16% since the December 24 lows, afterMnuchin called the banksto force reassure them. We’ve highlighted the lack of correlation between the stock market and the crypto markets many times in the past, so the equity returns themselves don’t matter much to crypto as an asset class. What does matter is why this rally occured. The Fed has done a complete “about face” on its policy, ignoring strong employment data and inflation figures which normally drive motivation, and instead have focused purely on stock market returns and sentiment. As our friends at Ikigai stated last week, “the now dovish Fed is great for risk-on assets and validates the idea that Central Banks are irresponsible, thus reinforcing Bitcoin’s original value proposition.” Once again, we remind all investors, even those who think digital assets are irrelevant, to rememberwhy Bitcoin and other cryptocurrencies exist in the first place. You can only push something so far until it finally breaks

So Equity Markets are Fragile, What About Crypto?

Meanwhile, crypto markets were largely unchanged last week, but January still concluded with a sixth straight negative monthly performance, the longest stretch ever.

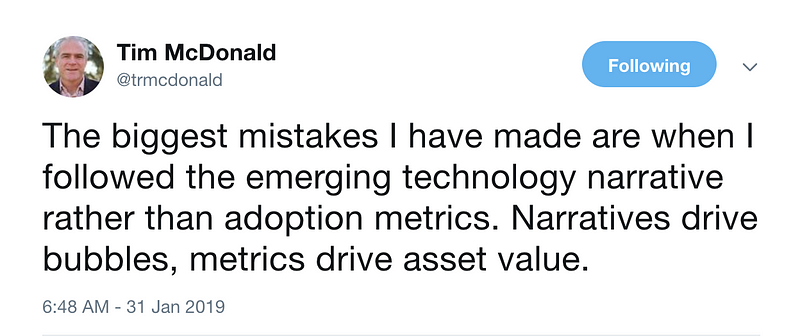

While February is historically a very good month for crypto prices, there doesn’t seem to be enough tangible data to sink your teeth into in order to make this market move materially higher or lower.Last week we even highlightedall of the positive announcements that are on the horizon in crypto, but the fact is, none of these events are actually happening today. All of the positives are important, but remain highly speculative and forward looking. Until we witness some actual substance to support all of the great announcements and infrastructure investments, it’s unlikely that this market can go materially higher. Even when certain protocols and projects deliver positive results or outcomes, the boost to token prices is often short-lived as the increased valuations can’t be sustained. As long-time technology investor, Tim McDonald,wisely stated this week:

The crypto narrative is still strong, but adoption remains weak.

Bubbles vs Adoption

So that leaves us at an impasse. We have a technology that is undoubtedly promising, coupled with major investments across the whole ecosystem reinforcing the future role that Digital Ledger Technology (DLT) will have on financial services and beyond. Yet prices of today’s digital assets don’t necessarily reflect this future. It’s become clear that investors are now demanding that these investments in the infrastructure begin to bear fruit before the asset class can grow any further. And that takes time. Daniel Heyman, a developer working on Ethereum projects at Consensys,put it best(paraphrasing):

In many ways, the bubbles created by the frenzy in the installation phase makes it possible for the new technology to succeed. The bubble creates a burst of (over-) investment in the infrastructure of the new technology (railways, canals, fiber optic cables, etc.). This infrastructure makes it possible for the technology to successfully deploy after the bubble bursts. The bubbles also encourage a spate of experimentation with new business models and new approaches to the technologies, enabling future entrepreneurs to follow proven paths and avoid common pitfalls. While the bubble creates a lot of financial losses and economic pain, it can be crucial in the adoption of new technologies.

The bubble [in crypto] came early because blockchain technology enabled liquidity earlier in its life cycle. More bubbles are likely.

Although there are no “good bubbles,” bubbles can have good side effects. During Canal Mania and Railway Mania, canals and railways were built that had little hope of ever being profitable. Investors lost money, but after the bubble, these canals and railways were still there. This new infrastructure made future endeavors cheaper and easier. After the internet bubble burst in 2001, fiber optic cables were selling for pennies on the dollar. Investors did terribly, but the fiber optics infrastructure created value for consumers and made it possible for the next generation of companies to be built. This over-investment in infrastructure is often necessary for the successful deployment of new technologies.

This analysis suggests that the best case scenario for crypto in the near-term may be more speculative bubbles, which will ultimately crash as all previous bubbles have. During this time, many investments will ultimately be wiped out, but each building block created will ultimately accrue value to those companies/projects/protocols/users that remain relevant during the subsequent phase(s). Different investing strategies will take advantage of this in different ways… quant funds will take advantage of the elevated volatility, VC funds will patiently wait for the cycle to conclude, and liquid strategies will adapt to what is most profitable. This is a key rationale for why active management matters in crypto, today and in the future, as fund managers offer the ability to navigate these bubbles and crashes to discover where value will ultimately accrue.

Notable Movers and Shakers

A choppy week left most tokens largely unchanged week-over-week. Those that outperformed generally were caused by news of increased future adoption via enhancements that are still months if not years away.

NEM (XEM) token saw a 26% selloff last week followinglayoffs from the NEM Foundation. According to the foundation, the organization is nearing bankruptcy and making a last ditch effort to sell some of their tokens to stay afloat.

Augur (REP) is still feeling thepositive effects of Veil’s launch two weeks ago, gaining 11% week-over-week. User experience is one of the major hurdles to mainstream crypto adoption and Veil seeks to solve this problem for Augur, 0x and other Ethereum dapps.

Ripple (XRP) posted overnight gains of 14% on Thursday aftervideo footage went viral of Christine Lagarde, head of the IMF, mentioning Ripple as one of the “new technologies that will actually change the way intermediation is conducted”. Although speculative, positive endorsements of blockchain technology from groups like the IMF is huge for the tiny world of crypto.

Haseeb Qureshi, GP at crypto fund Metastable, penned this article speaking to a central debate in crypto: the role of institutions. In a space that has thumped the table for decentralized and unseating large players from power, we forget that the rise of centralized institutions drove much of the progress in mankind’s history, and that these newly created decentralized institutions are fundamental to crypto.

Last week, messaging app Kik spoke out stating they would fight any enforcement action from the SEC levied against their 2017 ICO, when they raised over $100m. Kik received a Wells Notice last month which theypublicly responded to. While it’s good that Kik is looking to defend themselves in court instead of settle,publishing their rebuttal is an easy way to invite the world to critique your defense. Our own CLO, Phil Liu, thinks that Kik is unlikely to win as there is a rebuttal to every one of the arguments that Kin (their token) is not a security.

According to trading platform Caspian, the next wave of crypto traders will be High Frequency Traders (HFT). The fragmented and volatile nature of crypto provides opportunities for HFTs to capitalize on the price discrepancies common in the market. In addition, exchanges have begun to provide tools to allow for these HFT strategies. Although algo strategies have the potential for great success in crypto, such strategies may be short lived as the market develops, spreads tighten and exchanges consolidate.

Arwen, a crypto startup out of Boston, released a testnet this week for its Arwen protocol. The protocol is designed to allow traders of centralized exchanges to trade without providing the exchanges access to their private keys, essentially letting traders keep custody of their tokens. To start, the protocol will be available with a beta version through the KuCoin exchange, with an expected launch in Q2. Arwen is an example of one of the many good solutions we’re seeing developed in the crypto space that complement existing infrastructure.

Andreas Utermann, CEO of Allianz Global Investors, made comments this week that might have ruffled some feathers, including that cryptocurrencies are “entirely unsuitable for investing in”, and “look like something dreamt up by and most useful for the criminal underworld”. Putting aside the motivations of such comments (crypto and blockchain are afterall poised to disrupt businesses like Allianz), Utermann claims his intention was to point out that cryptocurrencies require far more regulation than has been applied to date.

SWIFT’s CEO revealed this week that the group is working with R3, the company behind the Corda blockchain, to integrate their Global Payments Innovation (GPI) Link Gateway to Corda for use in payment transfer and settlement. SWIFT has made a massive effort over the last year to step into the blockchain space as businesses like Ripple have made strides in cross-border payments. Althoughrumors circulated late last year that SWIFT was partnered with Ripple, it’s clear now that these two giants will be in direct competition.

JPMorgan’s Chair of Global Research, Joyce Change, commented last week that although cryptocurrency performance is down, the potential for blockchain technology to succeed is ever increasing. Chang believes that adoption will be slow and mostly concentrated in trade finance, estimating real impact over the next three to five years.

David Nage, Arca’s Head of Distribution,published an article in Block Tribunelast week discussing how crypto investing has revived the Fund of Funds model, which up until 2017 was considered dead.

Subscribe For the Latest Blockchain News & Analysis

Disclaimer: This commentary is provided as general information only and is in no way intended as investment advice, investment research, legal advice, tax advice, a research report, or a recommendation. Any decision to invest or take any other action with respect to any investments discussed in this commentary may involve risks not discussed, and therefore, such decisions should not be based solely on the information contained in this document. Please consult your own financial/legal/tax professional.

Statements in this communication may include forward-looking information and/or may be based on various assumptions. The forward-looking statements and other views or opinions expressed are those of the author, and are made as of the date of this publication. Actual future results or occurrences may differ significantly from those anticipated and there is no guarantee that any particular outcome will come to pass. The statements made herein are subject to change at any time. Arca disclaims any obligation to update or revise any statements or views expressed herein. Past performance is not a guarantee of future results and there can be no assurance that any future results will be realized. Some or all of the information provided herein may be or be based on statements of opinion. In addition, certain information provided herein may be based on third-party sources, which is believed to be accurate, but has not been independently verified. Arca and/or certain of its affiliates and/or clients may now, or in the future, hold a financial interest in investments that are the same as or substantially similar to the investments discussed in this commentary. No claims are made as to the profitability of such financial interests, now, in the past or in the future and Arca and/or its clients may sell such financial interests at any time. The information provided herein is not intended to be, nor should it be construed as an offer to sell or a solicitation of any offer to buy any securities, or a solicitation to provide investment advisory services.

.jpg)