What Happened This Week in the Digital Assets Markets?

What Happened This Week in the Digital Assets Markets?

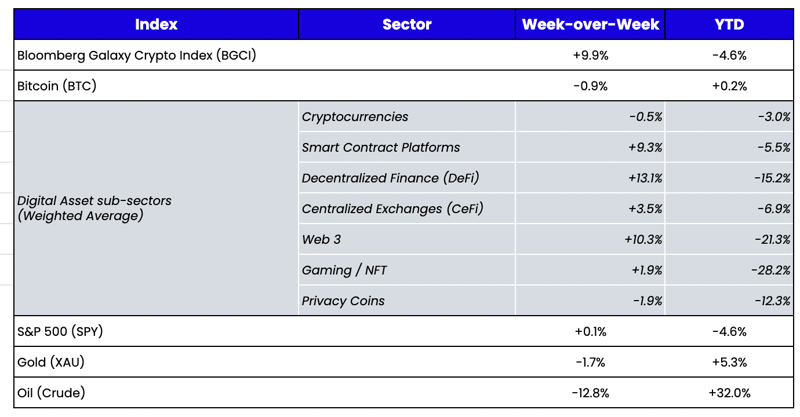

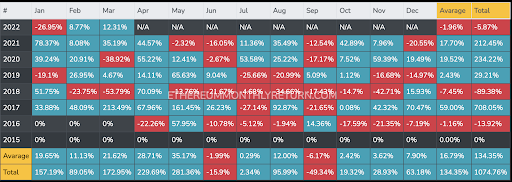

Week-over-Week Price Changes (as of Sunday, 4/02/22)

Source: TradingView, CNBC, Bloomberg, Messari

The digital assets market has performed relatively well despite the carnage seen across other asset classes, but the Ronin hack is a reminder that, while many of digital asset ecosystems are “too big to fail,” they are still a work in progress. Further, Terra Luna’s buys of $1.5 billion in Bitcoin may have been the catalyst that shifted digital asset investors sentiments.

Relative Strength in Digital Assets

The S&P 500 is -4.6% YTD.

The Bloomberg Galaxy Crypto Index is -4.6% YTD.

Considering the carnage seen across several other asset classes, the digital assets market as a whole has performed remarkably well, relatively, with an eclectic list of outperformers that have put up strong absolute returns. Over 50 tokens in our coverage universe are now positive YTD, stemming from DeFi (e.g. MPL +180%, RUNE +50%), CeFi (e.g. LEO +60% YTD, FTT +24%), and Layer 1s (e.g. ZIL +100%, LUNA +25%). Meanwhile, Bitcoin has been incredibly resilient compared to other macro assets.

.jpeg?width=512&name=unnamed%20(2).jpeg)

Source: NYDIG

It’s no secret that we believe digital assets will once again be the best performing asset class in 2022. Further, we believe the events of the past two months (recession looming, war, sanctions, etc.) are undeniably bullish for recession-proof pass-thru tokens and bearer assets. But even we didn’t anticipate that the market would shrug off negative sentiment as fast as it has, which leaves us at an interesting inflection point: cash balances are still near record highs, token supply on exchanges is at record lows, and DEX volumes are rising again (+10% WoW with DAUs +21% MoM). And this is happening right as we head towards what has historically been one of the best months (April) and best quarters (2Q) in digital assets’ short history. With catalysts for both Bitcoin (fiat and banking issues abroad) and Ethereum (ETH 2.0 merge), combined with what is now clearly a growing multi-chain world, it feels as though a powderkeg is about to explode.

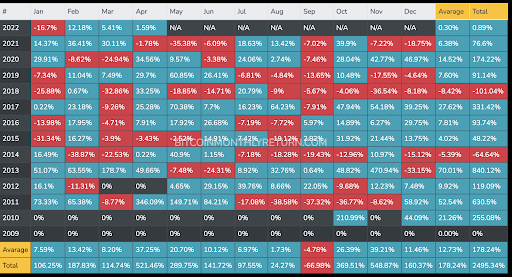

Bitcoin Monthly Returns

Ethereum Monthly Returns

The Ronin Hack in Layman’s Terms

The Ronin Bridge that connects Axie Infinity’s Ronin sidechain to Ethereum has been drained of 173,600 ETH ($590M) and 25.5M USDC in what may be DeFi’s biggest exploit to date. This latest hack occurred only two months after an attacker made off with the nearly $325M by exploiting the Solana side of the Wormhole bridge. A bridge occurs when you deposit tokens on one chain and get an IOU on another chain. A hack occurs when the original asset no longer backs the IOU. For example, it’s like owning MGM casino chips, going to the cashier to redeem for cash, and the cash ain’t there. As Arca’s own Peter Hans put it, another appropriate analogy would be if hackers compromised the Starbucks app and drained rewards points out of customer accounts (USD denominated). Starbucks would be on the hook for lost funds, or they could ignore it and severely damage their long-term business and brand reputation. Starbucks would obviously find a way to make their customers whole and ensure that their reward points were still “money good.”

On the one hand, this hack is yet another stark reminder that bridges between blockchains are still a work in progress. But on the other hand, it’s also a good reminder that many of these digital asset ecosystems are now “too big to fail.” In the Wormhole case, Jump Trading (Wormhole’s biggest backer), immediately plugged the hole. In the Ronin/Axie case, Sky Mavis (the owners of Axie Infinity, backed by a16z) is now on the hook for these customer losses; it’s unlikely that they will leave their customers hanging, and widely expected that they will plug the deficit.

Clearly, this is not demonstrative of the “decentralized” vision that many builders strive to achieve—it is very much centralized. But it’s also in the industry’s best interest that these incredibly well-funded and highly incentivized funds/companies do everything they can to keep the lights on until the tech becomes more bulletproof. Two years ago, SEC Commission Hester Pierce floated a 3-year safe harbor proposal, which “seeks to provide network developers with a 3-year grace period within which, under certain conditions, they can facilitate participation in and the development of a functional or decentralized network, exempted from the registration provisions of the federal securities laws.” This idea makes perfect sense in the context of DeFi, gaming, and other web 3 initiatives, which are better off being centrally backed in the early experimental days.

LUNA Continues to Make Headlines

If you’ve spent only a few minutes learning about digital assets, chances are you’ve heard of Bitcoin, Ethereum, and now Terra Luna—one of the most successful and polarizing digital asset projects. Terra Luna’s recent purchases of $1.5 billion of Bitcoin may have been the biggest driving force behind the turnaround in the sentiment of digital asset investors.

First, a quick background on Terra Luna (LUNA): LUNA is the governance and gas token of the Layer 1 Terra ecosystem. Additionally, LUNA is used to algorithmically stabilize Terra's decentralized stablecoin, UST. To mint a UST, one must deposit and burn the dollar equivalent in LUNA. At a high level, UST maintains its peg through the arbitrage opportunities presented when UST deviates. For example, when demand for UST exceeds supply, UST trades above $1. Since 1 UST is always redeemable for $1 of LUNA and vice versa, a savvy arbitrageur may deposit $1 LUNA for 1 UST (in this example, worth $1.03). In the process, the arbiter repegs UST at equilibrium by increasing its supply and is rewarded with the net difference (e.g., $1.03-$1).

We believe UST demonstrates a notable improvement on previous iterations of stablecoins. The first iteration of stablecoins were those backed 1:1 with fiat, such as Tether. Though practical, recent scrutiny regarding the legitimacy of Tether’s backing has highlighted the risks of a centralized counterparty. The second iteration of stablecoins were those backed by cryptocurrencies, like DAI. Though these mitigate the centralization risks posed by fiat-backed stablecoins, they are highly capital inefficient, as they account for volatility by requiring overcollateralization (often at 1.5:1 or 2:1 ratios). On the other hand, UST solves for both decentralization and efficiency, as it requires no collateral and relies on the decentralized verification mechanisms of Layer 1 technology.

Recently, the technological improvements of UST have been met with rising demand as UST surpassed a $16B market cap, growing 2x in the last four months alone. Demand has largely been driven by Anchor Protocol—a savings account offering ~20% yield—as well as Terra applications and cross-chain deployments. Given our conviction that a) stablecoin demand will continue to grow in tandem with (or faster than) the growth of the ecosystem and b) UST’s relatively low market share (10%) will likely grow, we believe UST’s growth outlook will be favorable in the near to medium term.

Source: Arca Estimates / Arca Research Associate Bodhi Pinkner on Twitter

Terra Luna is now buying BTC to back UST with real collateral

Recently, Terra Luna raised $1B from new investors in a private round. The Luna Foundation (TFL) is using these proceeds plus UST that they own to purchase Bitcoin—you can see their wallet and track their progress. Their goal is to buy $2-3B worth of BTC today (half done) and they have expressed interest in buying up to $10B BTC over time. This buying pressure has helped the price of BTC, but the narrative has helped even more. It is a powerful bull thesis for Bitcoin that a large stablecoin producer recognizes the importance of BTC as collateral, especially during a time when people all around the world are realize their money isn't really their money (Canadian citizens, Russian citizens, anyone in the SWIFT system, anyone with money on the London Metal Exchange). The Terra wallet now holds $1.5 billion worth of bitcoin, and Terra is pacing to surpass Tesla's current treasury holdings in bitcoin, which exceeds $2B.

- LUNA is the best pure-play way to bet on the growth of stablecoins (which is undeniable, and UST is currently the fastest horse).

- LUNA is an amortizing token, and amortizing tokens from high cash flow producing entities always work (LEO, BNB, FTT, etc.) -- and LUNA is amortizing as UST grows.

- Bitcoin maxis are now becoming "LUNAtics" because of the BTC purchases.

Regardless of how this plays out for LUNA, it’s likely that this is only the beginning in terms of Bitcoin as collateral.

What We’re Reading This Week