Source: TradingView, CNBC, Bloomberg, Messari

Another Yawn-Fest

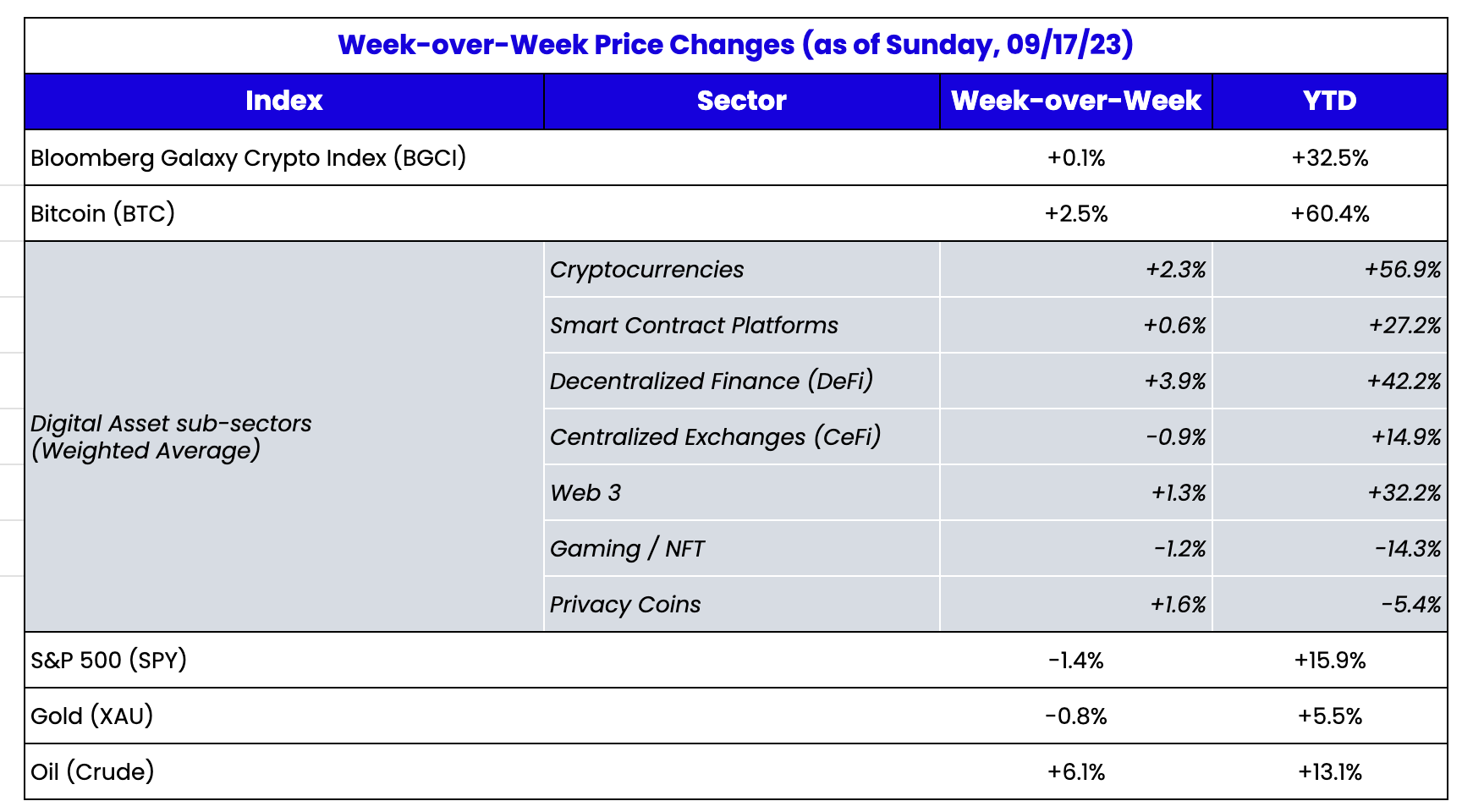

Another week went by without a lot of movement in the crypto secondary market. The FOMC meeting was the big event, ultimately sending Treasury yields higher once again and equities lower, but the minutiae of “higher rates for longer” had little to no effect on the digital assets market. Ironically, the Treasury market is now more volatile than the crypto markets. In fact, a 30-year Treasury bond issued 3 years ago is now down over 50%, barely outperforming BTC and ETH’s declines from 2021 all-time highs (-61% and -67% respectively). Perhaps more ironically, today’s higher Treasury yields are just about the only interesting thing happening in the digital assets industry, as projects with high cash balances are parking assets in Treasuries to earn fat yields and hundreds of millions (if not billions) in revenues. While Tether and USDC are earning the most, some DeFi projects are doing the same thing. Per our friends at Cumberland:

“It’s no wonder, then, how much focus within crypto is on importing treasury yields onchain. Maker (MKR) is up 40% since the start of July, a period where ETH is down 20%. YTD, MKR has nearly doubled. Maker is driving revenue of over $150m annually, a level of revenue generation nearly unheard of in the crypto space. The second-best performer YTD in the DeFi sector is Lido (LDO), which derives revenue from another “risk-free rate” ETH staking yields. MKR and LDO are, in fact, the only blue-chip DeFi names to outperform ETH this year.”

Away from yields, most of the market’s focus is on supply changes rather than demand drivers. For example, last week Mt. Gox, the defunct crypto exchange, said it

would not be able to complete repayments by the October 31, 2023 deadline set earlier this year, and has pushed it back by 12 months to October 31, 2024. The Mt. Gox trustees

are set to repay 141,686 BTC and 143,000 Bitcoin Cash (BCH) as part of the repayment plan. Last week, we discussed how the entire market was focused on the supply of digital assets being

potentially sold out of the FTX bankruptcy estate. Further, the market has been glued to Optimism’s (OP) increased supply due to a private round issued out of their Treasury, and upcoming VC unlocks for tokens like dYdX (DYDX).

This is a problem with the market right now. Every noteworthy event is supply-based, but a market rally can only happen when there is new demand, not just less supply. The three hottest areas of digital assets in years past – Stablecoins, DEXs, and NFTs - have stalled. Stablecoin supply (AUM) is falling.

DEX volumes are once again on track for their lowest volume month since we began tracking.

Source: Token Terminal & Arca Internal Calculations