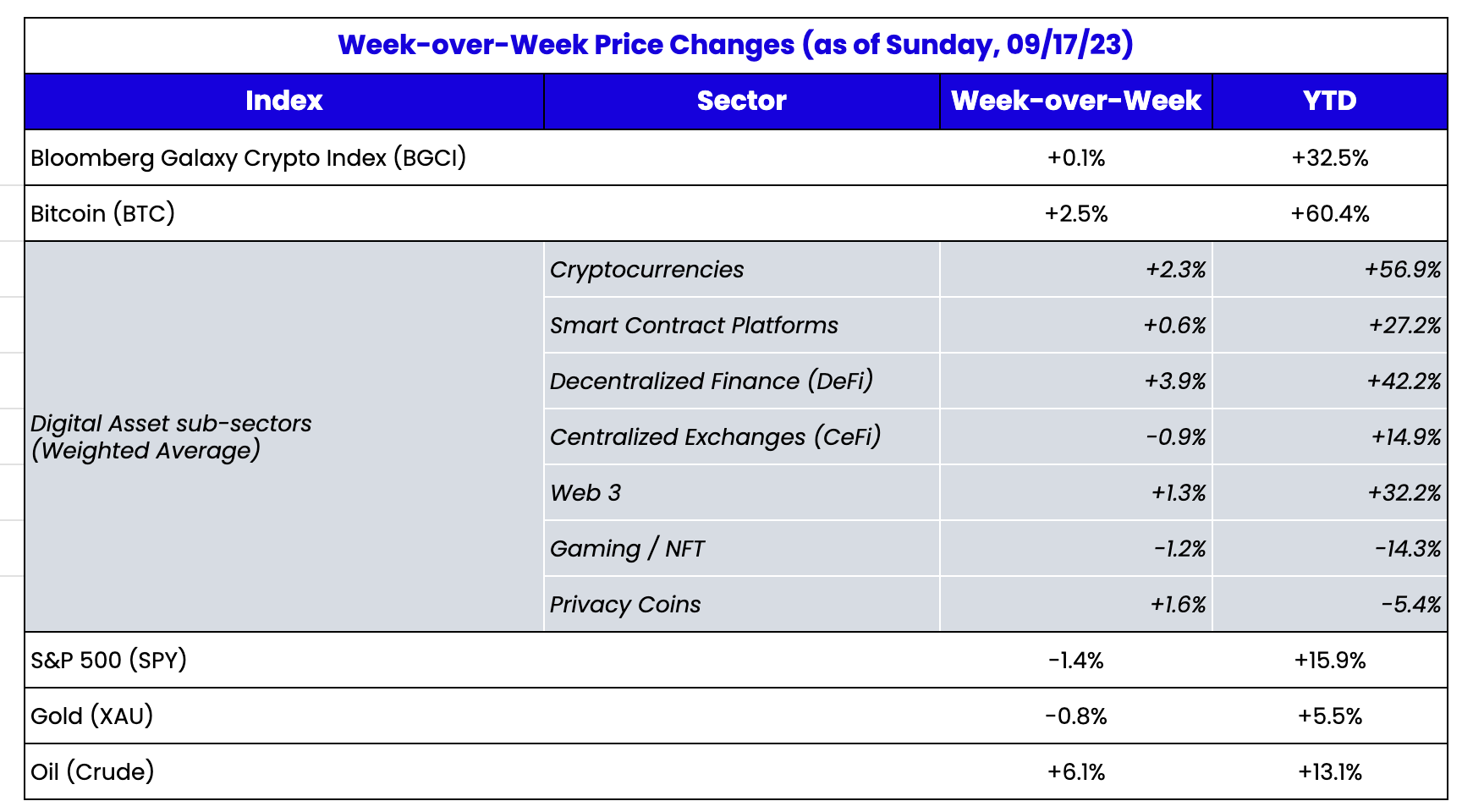

Source: TradingView, CNBC, Bloomberg, Messari

Progress in Digital Assets Isn’t Translating To Price

Imagine if every private company in the world was growing, and reporting record earnings and positive news, but not a single publicly traded company benefitted. Overall, this would benefit society and increase GDP, but the majority of investors would not directly benefit. Smart investors would start buying the debt and equities of publicly traded companies, knowing that these positive developments for private companies would eventually accrue value to other areas in their respective industries, as well.

A similar dynamic is playing out in crypto right now, but without the “smart investors”. Many private companies, and companies without tokens, are growing. For example"

- Coinbase’s BASE is the fastest growing Layer 2, but it’s not a big enough portion of Coinbase’s revenue base to influence its stock and there is no BASE token. In theory, smart investors should buy the tokens of other Layer 2 blockchains (OP and ARB for example), but the opposite is occurring (ARB and OP are underperforming the market presumably because of BASE’s success).

- Metamask, the most widely used crypto wallet, introduced a new feature called “Snaps” that allows users to install third-party developed applications directly to their wallets. Snaps essentially creates an application store for MetaMask, providing third-party developers with access to MetaMask’s 100M+ users. As Galaxy Digital wrote, “This will turn MetaMask into a much more customizable wallet, providing users the ability to design their own wallet experience specific to their preferences, similar to Chrome Extensions for Google’s Chrome browser. Snaps opens up the possibility for users to consolidate their cross-chain activity onto one wallet once a Snaps for that chain is made available.” In theory, smart investors should buy other wallet providers like GNO, along with buying other Layer 1 protocols (like SOL and ATOM) that would directly benefit from the easy multi-chain integrations. But GNO, ATOM and SOL are underperforming.

- Paypal and Visa are either rolling out stablecoin products or integrating with existing stablecoin projects, but, these are, again, fairly meaningless developments to Paypal and Visa’s overall revenues. Additionally, there are no “pure play” tokens to buy in order to take advantage of the likely rise in stablecoin AUM and transactions. The growth of stablecoins will influence Layer 1 and Layer 2 blockchains, as well as DeFi applications, but that 2nd order effect is not being bought up by investors.

And herein lies the problem for investors. Startup companies are still getting funded by VCs, but their success is years away and the ability to quickly monetize with a token like we saw in 2020-2022 is gone. Crypto equity investors have a limited playbook (BTC via various trusts like GBTC, Bitcoin mining stocks, or Coinbase stock), none of which accrues any real value from recent initiatives. And liquid token investors are stuck buying and selling the same Layer 1 and Layer 2 blockchain tokens, in the absence of any meaningful apps to invest in. While these apps will directly benefit from today’s growth and excitement, it is hard to measure the impact. In short, when most of the investable universe are infrastructure tokens, it’s hard to see when a tipping point happens even though it very well may already be happening.

Meanwhile, last week we did see some activity. The total volume for the exchange sector grew by 29% WoW, reaching $318B. This growth was primarily driven by the increase in derivatives volumes, with both centralized exchange derivatives and decentralized exchange derivatives growing by 36% WoW. Unfortunately, this growth in volumes was not tied to the myriad of positive news, but instead, was tied to traders front-running the upcoming FTX estate liquidations. Long-term investors are taking a back seat to fast money traders.

The Market Completely Misunderstands How the FTX Estate Sale Will Happen

Though broader crypto markets were unchanged to slightly higher week-over-week, there was a brief selloff to recent lows on Monday due to news of

FTX's decision to liquidate its digital asset holdings in order to meet the demands of its creditors in the bankruptcy case. According to the court filing, the firm holds around $1.16B in SOL (Solana), $560M in BTC, $192M in ETH, and $1.49B in various other tokens. However, the sale process only permits a maximum of $50M in digital asset sales during the first week, followed by $100 million per week thereafter, with court permission. Ultimately, FTX may be allowed to sell up to $200 million worth of digital assets per week, again with the court's approval.

Not surprisingly, the market sold off on this news, despite it being telegraphed for weeks. It seems the market was expecting a fire sale, which is just not going to happen.

For starters, Galaxy Asset Management, not the Galaxy trading desk, won the bid to manage the estate. They must act as a fiduciary so they will sell gradually and opportunistically. When asset management arms win the right to manage a bankruptcy estate’s assets, it is very different from when an estate runs an auction process. An auction is designed to find the best bid immediately. However, an asset manager’s goal is to maximize the estate, and potentially even earn a return over the course of the bankruptcy, rather than just liquidate indiscriminately. This process will take many months, and potentially even years. Further, most of the assets that do find their way to new buyers won’t trade via exchanges. Galaxy is already receiving massive amounts of reverse inquiry (some from real funds that are interested; some from fishing expeditions looking for information). It is likely that OTC sales will dominate the buying, and therefore it will be less likely to see a lot of selling on exchange or via TWAPs. As good bids come in, Galaxy will engage.

The $100M max selling per week is really not relevant. Galaxy can ask for court approval if they get a bigger block bid and there’s no pressure to have to sell anything in any given week. The $100M was just a guideline to prevent dumping and destroying value for the estate and was likely based on Galaxy’s own pitch to win the business. Others are worried about Galaxy’s ability to hedge by shorting futures. But in our opinion, hedging will be opportunistic (i.e. long puts to offset a large drop in the portfolio). This will have little to no impact on the market.

Some have even suggested that Galaxy will front-run the supply from FTX. That’s just absurd. Galaxy cannot front-run the sales and profit internally -- that is highly illegal, and their asset management business is completely walled off from their prop desks and Novgratz's personal account. These trades, if they happen, will be on the level.

Bankruptcies take a long time, especially one as complex as FTX. This is not some half-baked plan. Galaxy worked for months with the courts to win this business. The goal is to maximize the estate, not speed up distributions. This, perhaps, caps short-term gains due to opportunistic sales into strength, but it is not a fire sale into weakness. It’s also worth noting that market makers and traders almost ALWAYS sell more ahead of known block sales than what actually comes to market. For example, if you know PIMCO is selling $100M of bonds, and ten funds sell $50M each to make room for it, how much of the $500M sold to make room for $100M actually cover their shorts profitably? Most of the time, those who sell early end up buying back higher.

As we approach the next few weeks, if the selling does happen quickly, it's simply because the market became well-bid, and there was enough demand to absorb a lot of the supply at strong levels. This, of course, can be read as bullish due to the demand. Conversely, if bids aren't there right now, then the selling will be slow (or not at all), which can also be interpreted as bullish (or at least less bearish than the market perceives currently).

Regardless, it’s a big win for Galaxy Digital, and the best outcome for markets given Galaxy Digital is one of the few firms that has proven the ability to manage risk in a tough crypto winter. In a perfect world, they’d bring all of these assets on-chain, and run a completely transparent process to show both the power of blockchain and the need for TradFi intervention together. But given the sensitivity around the portfolio and no reason for the estate to showcase their every move, this likely won’t happen.

The SEC Went After… (Checking Notes)...Stoner Cats?

The

SEC recently protected investors by shutting down and fining a project called Stoner Cats. Um, what? This project was released in 2022 and was backed by celebrities such as Ashton Kutcher, Mila Kunis, and Jane Fonda. The purpose of the project was to create an animated TV series based on five house cats who mysteriously become sentient. I recall at the time thinking that this was a great way to use a token – to bootstrap a creator series by selling ownership rights on certain characters of the show.

The SEC ruled that selling the NFTs was an unregistered offering of securities. The project is required to return the $8M they raised, pay a $1M fine, and scrub all online presence on Twitter and their website. The language they used in the ruling implies that basically, all PFP collections in our space are securities. Per usual, SEC Commissioner Hester Peirce

wrote a more thorough statement expressing her dissent, which unfortunately is meaningless. Of particular note is a great analogy, which brings to light how ridiculous and over-reaching this latest action was:

“While updated for the digital age, the Stoner Cats NFTs are not that different from Star Wars collectibles sold in the 1970s. On the heels of the very successful release of Star Wars in 1977, fan excitement was high. To the delight of millions of children that holiday season, the toy company Kenner sold “Early Bird Certificate Packages,” redeemable for future Luke Skywalker, Princess Leia, and R2-D2 action figures and membership in the Star Wars fan club. The sales of these certificates helped to build a die-hard community of Star Wars fans. Would those I.O.U. certificates, which could be re-sold, constitute investment contracts? Using the analysis of today’s enforcement action, the SEC should have parachuted in to save those kids from Star Wars mania.”

We have argued over the past few months that regulatory fear has hit NFTs harder than any other sector in crypto, and this recent action seems to confirm that view. Without regulatory clarity, NFT project founders are unwilling to implement the creativity we saw during the NFT bull market in 2021. As it stands today, only pure art projects seem to be outside of the SEC’s crosshairs