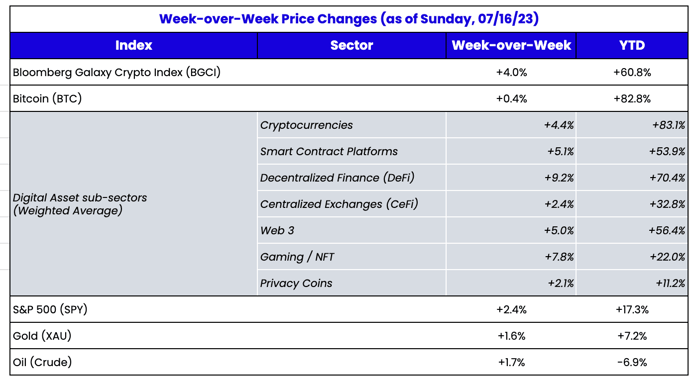

What happened this week in the Crypto markets?

Source: TradingView, CNBC, Bloomberg, Messari

We’ve Lost The Plot With Regulation

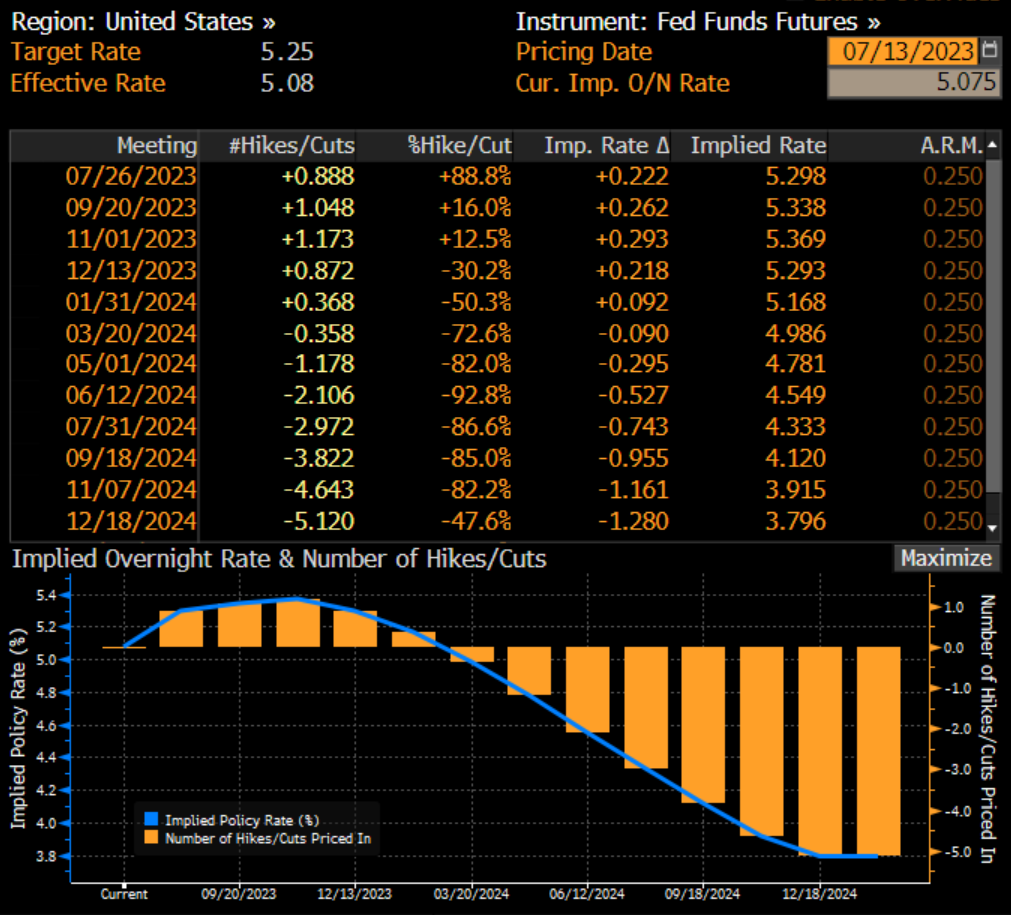

Twas a good week for digital assets. First, a cooler-than-expected CPI report set the stage for all risk assets to continue the rally, with the Nasdaq adding another +1.3%, which now sits +42% YTD. Fed fund futures are still pricing in about a 90% chance of a 25 bps rate hike at the upcoming July meeting in line with the forward guidance at the last FOMC meeting, but following the CPI release, the market now believes this may be the last hike in the cycle compared to the two hikes projected in the Fed’s dot plot.

Source: Bloomberg immediately after the CPI report

Next, on July 13, a federal judge granted partial summary judgment on the SEC’s lawsuit against Ripple Labs, indicating that Ripple’s XRP token “is not in and of itself a ‘contract, transaction, or scheme' that embodies the Howey requirements of an investment contract". In short, the court’s conclusions include:

- Institutional sales - PASSES the Howey Test as tokens sold by Ripple via investment contracts to sophisticated buyers are a security offering

- Programmatic sales - FAILS Howey Test step 3 - reasonable expectation of profit from the efforts of others. Tokens sold by Ripple and others via centralized exchanges to the general public are not a security offering because:

- Buyers could not know their money was going to Ripple

- Any profit expectations were not derived from Ripple’s efforts, and the court rules that a mere speculative intent is not sufficient to establish this

- the sales were not made pursuant to contracts that contained lockups, resale restrictions, indemnification clauses or statements of purpose

- Other distributions (payment to employees, and third parties via Ripple’s Xpring accelerator) - FAILS Howey Test step 1 - no investment of money. Recipients did not pay money or “some tangible and definable consideration” to Ripple.

Now, there still needs to be a case-by-case review of the underlying actions by the promoters that will ultimately determine whether Ripple is an unregistered investment offering (and the SEC is likely to appeal), but this was still a huge moral victory for Ripple, token investors, and token issuers. It shows a clear pathway for coins and tokens other than Bitcoin to be deemed “not a security”. The initial winners (from an investment perspective only):

- Good for any other current pending lawsuits -- COIN, GBTC

- Good for service providers of tokens besides Bitcoin - COIN, GLXY

- Good for other non-currency tokens, specifically those that Robinhood just recently delisted (ADA, MATIC, SOL) based on fears that these were securities

- Good for DeFi, whic arguably had the highest regulatory overhang

- Good for XRP in that it now joins BCH, LTC, BTC and ETH as tokens that will be listed on Paypal, EDX, Robinhood and other non-crypto native platforms since it is potentially in the clear from a regulatory perspective

The market agreed. All of the above had significant rallies post the XRP ruling.

Source: TradingView

But lost in the celebration from armchair lawyers and newfound regulatory experts is the silliness around all of this. For example, when people fly, they mostly care that someone cannot easily bring a gun or knife onboard. However, TSA makes us take off our shoes because of a single attempted shoe bomber. There will always be outlier risks, but the TSA is unlikely to protect us from them, so why makes lives more difficult?

Similarly, holistically, the U.S. is the best financial market in the world because of its robust investor protections including those offered by the SEC. But if you asked Americans what they care about most with regard to the SEC, most would tell you something along the lines of “I just want to know a little bit about what I’m buying, and that companies can’t lie, misstate facts, or steal my money”. Somehow this sentiment turned into 300-page prospectuses loaded with more information than necessary for the average investor and seemingly endless debates over which entity can or cannot trade certain financial instruments. But all we really want is protection against the Enrons, Madoffs, and FTXs, none of which were prevented due to regulatory actions.

Speaking on behalf of Americans, I believe we all just want to invest in BTC, ETH, DeFi tokens, private startup equity, stablecoins, AAPL, TSLA, Gold, Oil, bonds, etc all in one place. We don’t care about the Howey Test. We don’t care what is a currency, commodity, security or other. We don’t need more than 5-10 pages of a company or project’s description, cap structure, and financials.

Stop making us take off our shoes – just let us onboard and we can deal with the rare, outlier consequences.

The Smartest Arb in Crypto History

One of the smartest things I have seen in crypto happened on Monday – and it went nearly unnoticed. On July 6th, Multichain, the cross-chain bridge, was hacked for $125m. Multichain has had its fair share of problems, with the CEO being unreachable for the past month and rumored to be arrested in China. However, the important part is that Multichain has been the dominant way to bridge to and from Fantom (FTM), an EVM-compatible L1. Out of the $125m bridged, $120m was stolen from the Fantom Multichain bridge, with $63m in USDC.

Given that it's a cross-chain bridge and the assets backing the bridged assets were taken, all stablecoins on FTM depegged. This led to USDC trading at 50 cents on the dollar for the past three days, with no way to arbitrage it back to $1. Essentially, 1 USDC on FTM did not equal 1 USDC everywhere else since Multichain froze their contracts and did not allow tokens to be bridged back to Ethereum or other chains.

Source: Dex Screener USDC on FTM(SpookySwap) up to June 9th

Or so we thought. It turned out that there was a way to bridge back to the Ethereum mainnet, and it became painfully obvious when one address (0xfad7) started transferring FTM from a centralized exchange, purchasing discounted USDC, and subsequently sending it out to acquire more FTM. This process was repeated, and as a result, this wallet managed to drive the price of USDC up from 50 cents to 90 cents, clearly finding a way to arbitrage the USDC price.

Source: Dex Screener USDC on FTM(SpookySwap) up to June 10th

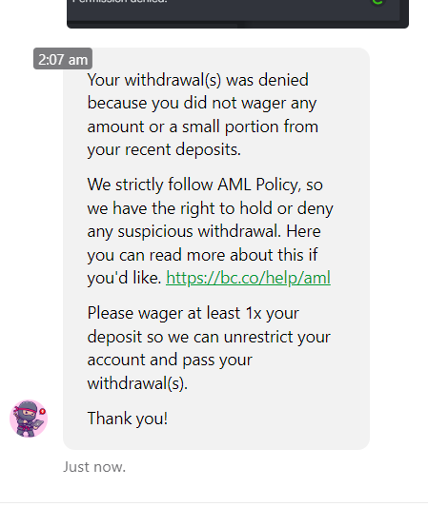

It turns out, 0xfad7 was sending the discounted USDC to BC.Game, an offshore crypto casino similar to Rollbit. BC.Game accepts crypto from various different L1s and L2s including stables from Fantom. However, BC.Game made a mistake of instantly crediting USDC from any network at $1, without anticipating or preparing for a de-peg. This oversight completed the arbitrage.

With a way to get USDC off Fantom, the trade was simple:

What made this even funnier was the casino wasn’t allowing withdrawals unless you bet 1x your deposits. So the final trade likely looked something like this:

Buy FTM from a centralized exchange -> withdraw to Fantom Network -> swap to USDC on Spookyswap -> send to BC.Game -> bet on low-risk games to hit withdraw threshold -> withdraw to another network with USDC worth $1 again.

Source: Telegram user

After a few hours of arbitrage, it appeared that BC.Game became aware of the situation and realized that they were left with a considerable amount of worthless USDC. Consequently, they stopped allowing withdrawals and proceeded to dump their USDC on Spookyswap:

These selloffs caused the price of USDC on Fantom to drop back to its current trading value of $0.56. The exact amount of losses incurred by BC.Game and the profits made by 0xfad7 and the few other wallets engaged in this arbitrage are unclear. However, BC.Game sent well over 1 million USDC to Spookyswap to be sold at a discounted price below $1.

Source: Dex Screener USDC on FTM(SpookySwap) as of 7/14/23

We all hate hacks. But you have to appreciate the hustle of this arbitrageur.

Disclosures: Arca did not trade this arbitrage given the risks of offshore casinos. Huge Hat tip to Bob and others for figuring out what was happening.

Casino Wakes Up