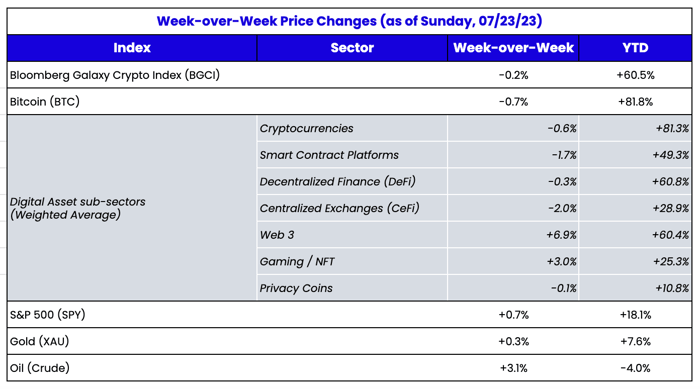

What happened this week in the Crypto markets?

Source: TradingView, CNBC, Bloomberg, Messari

An Example of Real-World Assets

Since we spend all of our time studying the digital assets industry, its evolution, and the investment opportunities that come with it, it is often difficult to decipher what has gone mainstream and what is still simply insider industry jargon. For example, at some point in the last two years DeFi, NFTs and stablecoins all went mainstream, but I’m not entirely sure when it happened. For a long time, many industry outsiders thought all tokens were just “another Bitcoin” or cryptocurrency, or some nonsense “memecoin”, and then slowly the investing world began to realize that this wasn’t true - that there were in fact many categories of tokens with different purposes, structures and value propositions. It certainly wasn’t obvious when

we launched our Digital Assets Taxonomy in 2021, as our categorization was one of the first attempts to educate, but it seems obvious now in retrospect.

To that end, I’m not entirely sure where “Tokens backed by Real World Assets” falls in today’s lexicon. Is this the 5th legit category of digital assets (after cryptocurrency, DeFi, NFTs, and Stablecoins), or is this just another buzzword that will soon fall off the map? From an investing perspective, tokens backed by RWAs aren’t that interesting yet. Most are securities, and therefore there is insufficient market liquidity, immature alternative trading systems, and lack of infrastructure available to trade these instruments in the same way that we’ve come to expect for other tokens that are not securities, or that reside in a regulatory gray area. But if this category continues to grow, you’d assume the infrastructure will catch up quickly.

Let’s clarify a few things about tokens backed by RWAs? For starters, it’s important to recognize that in many ways a digital asset on a blockchain is no different than an ETF – a wrapper that can house any asset inside of it. Much like ETFs started as S&P 500 Index tracking stocks and have ballooned to now represent everything from gold, to currencies, to bonds to real estate… tokens on a blockchain can represent just about any underlying instrument as well.

Eventually, IF the ability to trade blockchain-based assets continues to grow and expand, more and more traditional “real-world assets” will be tokenized to take advantage of the unique characteristics of blockchain-based trading and proof of ownership.

But RWAs have also snuck into the digital assets industry not as tokenized assets, but simply as cash investment substitutes. When interest rates were 0%, no one cared to put their cash in low (no) yielding instruments. But with short-dated Treasury yields now north of 5%, the game has changed. Parking cash in a bank was no longer a viable option financially, and became even more egregious when banks themselves became unstable earlier this year. Stablecoin issuers are now investing their cash into RWAs (Treasuries) to earn a yield. Both

USDC and

USDT (Tether) have diversified their holdings away from commercial paper and other riskier assets into U.S. Treasuries. And MakerDao (MKR), the entity behind the stablecoin DAI, has begun to back its stablecoin with U.S. Treasuries as well. These aren’t “tokenized bonds” per se, but rather, blockchain-based companies investing in RWAs. Either way, it’s clear that assets that were once confined to traditional finance are now seeping their way into the digital assets arena.

To illustrate the earnings impact, let’s dive deeper into MakerDAO. Maker has always had a significant amount of dollar-based assets on its balance sheet, but only recently have they begun to invest in treasuries. This newfound interest income is a huge boon for the project. In the last 3 months, Maker has been generating record revenues. By reducing USDC on its balance sheet and replacing it with yield-generating RWAs, Maker has managed to quadruple its earnings and the MKR token now trades at under 10x earnings.

This shift into the “real world” has had a major impact on MakerDAO’s financials. Simply by integrating real-world, yield-bearing financial instruments into its business, Maker has launched itself into the top 10 most profitable blockchain-based entities.

As

we discussed last week, the main goal of most digital asset investors is to be able to invest in all asset classes in one place, instead of the fragmented and separate ways in which we must currently invest in blockchain assets and traditional financial instruments.

“...I believe we all just want to invest in BTC, ETH, DeFi tokens, private startup equity, stablecoins, AAPL, TSLA, Gold, Oil, bonds, etc all in one place. We don’t care about the Howey Test. We don’t care what is a currency, commodity, security or other. We don’t need more than 5-10 pages of a company or project’s description, cap structure, and financials. “

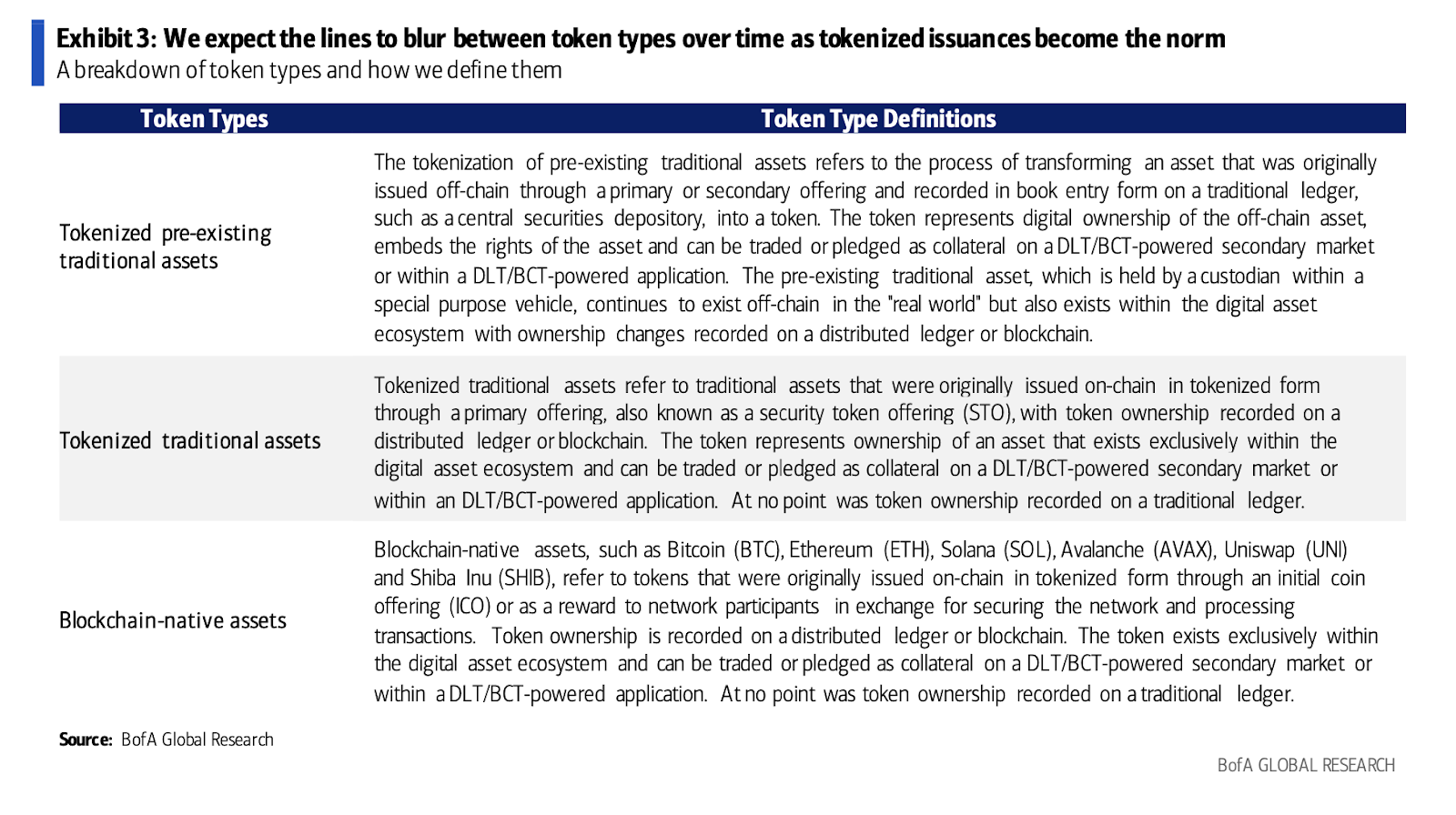

We’re not there yet, but it does feel like we’re getting closer to this reality. It was only two years ago when our industry was excited because Tesla and other corporations were putting Bitcoin on their balance sheets. Now, we as an industry are excited when blockchain-based companies are putting treasuries on their balance sheets. Eventually, the lines will blur between tokenized pre-existing traditional assets, assets issued in tokenized form, and blockchain-native assets. It remains to be seen whether a TradFi incumbent, or a Blockchain incumbent, will offer the “one-stop shop” experience, but it is definitely coming.