Source: TradingView, CNBC, Bloomberg, Messari

A Quick Recap of Frequently Discussed Topics

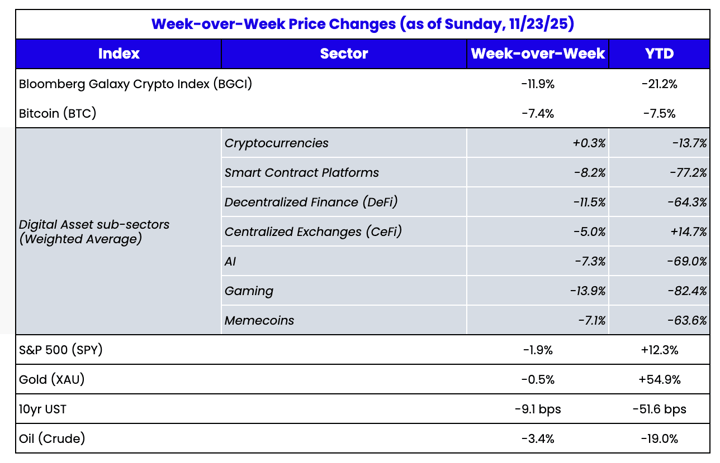

Last week, crypto markets dropped 5-10% for the second straight week and the 3rd in the last 4. But unlike previous weeks, a bid began to form following a dovish statement from the New York Federal Reserve, blowout earnings from Nvidia (NVDA), and some retail buying. While we wait to see if crypto markets can regain strength ahead of the new year, we wanted to follow up on a few items we’ve been discussing regularly in recent months.

1. We spent all of last week talking about DeFi and other cash-flow-producing digital assets that value investors are largely ignoring amid the broader crypto sell-off. We were wrong about one thing. DeFi isn’t just growing, it’s literally blowing the doors off of every other digital asset. In this amazing report from 1kx, they show just how fast revenue-producing apps are growing at the expense of Layer-1 protocols.

"Blockchain valuations aggregate north of 90% of the total market cap of fee generating protocols, despite their share in fees declining from over 60% in 2023 to 12% in Q3 ‘25. Conversely, DeFi/Finance protocols accounting for 73% of all fees, though in aggregate their market cap share remains well below 10%"

Goodness. It’s even more drastic than I thought.

Source: 1kx

2) We’ve been on a big “lack of education is the biggest problem in crypto” kick for most of this year, and continue to believe so. The constant misinformation is making it really hard for any investors to take this asset class seriously. But let’s take this a step further.

Institutional investors will never buy crypto in meaningful size until we stop calling it all "crypto".

For instance, in Coinbase’s weekly market commentary, their first sentence stated “Macro continues to remain the dominant crypto market driver.” If all of the major firms in this space simply write and talk about macro all the time, and call everything "alts", then investors are right to ignore this space. Why spend time on an investable universe that is marketed as if the entire asset class moves as one single asset?

If we called every ETF that wasn't SPY an "altstock", then no one would buy ETFs or stocks either. If we called U.S. Treasuries "bonds" and every other debt instrument an "altbond", then no one would buy fixed income either.

But we don't because that would be stupid. And the leaders in debt and equity markets know this.

The platforms that sell stocks (exchanges, brokerages, research firms) recognize that ETFs are just wrappers, and that many different assets can be put inside them. As such, these brokerages, exchanges, and research firms don't spit out macro commentary generically about ETFs, because that would be stupid. Instead, they teach about sectors and assets INSIDE of the wrapper, not the wrapper itself.

Similarly, brokerages, investment banks, and research firms separate government bonds from corporate bonds, and IG bonds from HY bonds, and convertible bonds from straight bonds. None of these firms spits out macro commentary about all of fixed income as one vehicle. Because that too would be stupid. Who issues the debt matters, and the unique features of that debt matter (coupons, maturities, covenants, call features, convertibility features, etc).

The token investing world is no different.

- There are different issuers of tokens (individuals, companies, decentralized protocols, etc)

- There are different features (inflation vs amortization, staked vs unstaked, asset-backed vs equity-like, etc)

- There are different sectors (L1s, DeFi, DePIN, stablecoins, memecoins, etc)

There is nothing similar about most crypto assets besides the wrapper. We should never discuss BTC, USDT, XRP, ETH, TAO, HYPE, BNB, DOGE, HNT and other assets that have LITERALLY NOTHING TO DO WITH EACH OTHER besides the wrapper ("crypto") in the same conversation.

So until the leaders of the crypto industry (exchanges, brokerages, data providers, and large asset managers) start intelligently differentiating between the types of token issuers and the features of the token from the wrapper itself, this industry will remain dead to real investors.

3) Microstrategy (MSTR)

I will never understand the fascination with Michael Saylor / MSTR. Nor will I know how people can confidently spout such inaccurate takes that are so easily disprovable.

I’ve been refuting the misconceptions about MSTR for years, and yet every time Bitcoin falls, the same nonsense spouts up again about MSTR being a forced seller of Bitcoin, or MSTR having their holdings “liquidated,” as if it were some sort of levered perp future.

It takes less than 5 minutes talking to any debt/equity expert to understand that MSTR will never have to sell their BTC unless Bitcoin has already fallen so far that their selling is an irrelevant afterthought.

MSTR may never buy a meaningful amount of BTC again if the capital markets are no longer open to them. And that removes one of the largest buyers of the past few years. So if your entire Bitcoin thesis is that one buyer will buy forever, you definitely need to question that view. Saylor and MSTR may no longer be relevant as marginal buyers compared to ETFs.

But MSTR selling BTC is not even remotely a concern.

- It would be almost impossible for an activist investor to gain control of the board, given Saylor’s 42% ownership.

- There are no covenants in the debt that force a sale.

- Interest expense is low and manageable (don’t forget the core tech business still has positive cash flow).

- Very few companies ever default because of debt maturities (Investors are sheep and will almost always roll the debt - extend and pretend).

If you follow anyone who says MSTR is a risk to BTC, tell them to call me. MSTR shares and their convertible debt and preferred shares may keep falling, but that does not pose a risk to Bitcoin itself.

4) Wow - Arca made an impact. Many of you have seen that Arca has been trying to change the industry standard for market cap definitions. We have been pushing for the big exchanges and data providers to stop using “market cap” (which is just float) and “FDV” (which is total supply) because the token structure has evolved. Adjusted market cap is much more prevalent and more similar to “outstanding shares” in the equity world.

Well, CoinMarketCap was the first to listen, as they announced their own version of Adjusted Market Cap to better reflect reality for tokens that have amortizing supply structures. Way to go CMC! Your move next, CoinGecko, Coinbase, Binance, et al.

5) Tokens – they’re just like stocks! We’ve been working overtime trying to exemplify why tokens like PUMP, AERO and HYPE are more like stocks than cryptocurrencies. We have consistently emphasized that tokenholders have rights and that token issuers have a fiduciary responsibility to their tokenholders.

Well, we’ve had a few examples last week that show both the good and the bad of tokenholder rights.

- GRASS – Grass announced its first “token holder call”, akin to an investor call, last week. In a related story, GRASS was one of the best-performing tokens last week, rising by over 27% (up as much as 50% at one point). It doesn’t take much effort to help your token holders; it just takes some simple blocking and tackling

- We talked a few weeks ago about how Pump.fun did an acquisition, and voluntarily swapped the tokens of the acquired entity into PUMP tokens to make them whole. A voluntary, but important gesture to make tokens more “equity-like”.

Well, the flipside of that is Coinbase. Coinbase announced an agreement to purchase Vector.Fun, a Solana-native on-chain trading platform with infrastructure that can surface new assets immediately at creation and plug directly into Coinbase’s DEX trading integration. Well, here’s the rub. Vector has a token, Tensor (TNSR), and Coinbase announced it is acquiring only the Vector team, not Tensor, leaving TNSR tokenholders high and dry. It would not have cost much to take care of token holders, but Coinbase chose not to. Two steps forward, one step back.

Drunk on Token Buybacks

Written by Christopher MacPherson, Analyst at Arca

Buybacks are a crucial concept in crypto, and it's essential to have a deep and nuanced understanding of them. If you're clear on what buybacks are (and what they aren't), you'll gain insights into how tokens function. This knowledge will help you understand why token values fluctuate, which tokens are likely to trend towards zero over time, the reasons behind the market's volatility, and the factors contributing to the current bear market.

Crypto is at a crucial juncture.

The ironic aspect of Hyperliquid being such a unicorn to the point of almost comedic, has altered the community's understanding and expectations of buybacks, though not due to any fault of their own.

"Fundamentals are bearish" --> Hyperliquid launches --> Play of the cycle --> We fall in love with HYPE's 99% buybacks --> Buybacks pump the token! --> Every project must do 100% buybacks --> Confusion/anger when tokens aren’t up only forever

Crypto is now wasted, drunk on buybacks–euphoric about teams giving back to holders, angry when 100% buybacks aren’t implemented, and disoriented when price does not go up only forever.

It's very crypto to see something become successful, copy it 50 different ways, take the idea to euphoric extremes, and ultimately leading to losses for traders. Then, it gets labeled a scam. Its, important to note that tokens do not “pump the price” of other tokens, and 100% buybacks can hurt tokenholders. And that’s okay.

What a buyback does do…

- Creates four types of demand

- Connects the success of the project with the value of the token

- Strengthens trust in an otherwise trustless system

- Enables new inflows of capital to crypto

Buybacks Create Four-In-One Demand

- Direct Demand: The emphasis is on the actual price appreciation from market buying of a token, but buying back via market orders is typically not impactful in the short term. Consider a 20x multiple to revenue on a $1B token. This equates to a ~$5,700 purchase of the token every hour—impactful in aggregate but negligible against expected liquidity for a $1B FDV token.

- Amortizing Demand: To realize the full benefit of tokens, teams need to drip new supply into the circulating supply to support marketing incentives and community/team/investor alignment. This is dilution. Participants severely underestimate that every additional token entering circulation dilutes their holdings. Removing the bought-back tokens from circulation creates reverse dilution. Supply and demand.

- Floor Value Demand: Why do the stock market indices not go down by 90%? Investors understand there is inherent value in the business, which connects with the asset. Stock market investors view downturns as opportunities. Crypto traders sprint to the exits because, historically, tokens have lacked real value. The rebuttal that public equities have liquidation rights is overblown, given that common shareholders typically realize only ~0.97% of their share value on average in a liquidation. There have also been cases of liquidation pro rata to tokenholders in token-only structures such as Aragon DAO.

- Alignment Demand: The most impactful aspect of buybacks is the alignment it creates between the team, tokenholders, and the success of the project. Thankfully, crypto has mostly moved away from fully decentralized governance voting structures. But with that change comes added trust dynamics that the team’s discretion will be in a tokenholder’s best interest. So what can build trust in its place? Showing instead of telling—sacrificing revenue that could have been otherwise funneled to a “Labs” division (roughly translates to the team) is the ultimate trust-building mechanic a team can implement.

Sunday Scaries

Crypto is beginning to resemble the dreaded "Sunday Scaries," with individuals online sharing theories about cryptocurrency. These include:

- "The Value of the Network"

- Governance Tokens

- "L1s are worth at least $1B"

- Attention Value

- Exhausting “New Meta"

- Meme Theses

What is the commonality here?

Misnomers from crypto’s past that attempted to artificially assign tokens' value (demand drivers) when no such value exists beyond temporary speculative demand.

The "Tier 1" VCs, KOLs, and underwater holders creatively conceived these concepts in the hopes of defying the most basic concept of markets: supply & demand. There are no greater offenders than L1/L2 tokens. Since HYPE’s TGE, there have been very few timeframes when it would have been beneficial to buy and hold L1/L2s.

These concepts have distorted the market’s understanding of how to invest in crypto. And this is also why the crypto market trades like a never-ending game of chicken.

Goal: Up Only Forever

Nothing has ever, or will ever, go up only forever.

So, why do people invest in tokens? Specifically for app tokens, investment is primarily driven by the belief that the application (business) will grow, and that buying the token gives them a piece of that upside. That, of course, only works if the asset is designed to grow in line with the business’s success.

The true goal of a company is to create a product that people are willing to buy without needing any incentives. When this happens, the business's value can grow, which in turn affects the token's value; the token's value increases or decreases based on the business's performance. The aim is for the token to outperform the market average during both growth and decline, with the ultimate objective of achieving sustained growth.

Perfect Buyback Execution:

“Do what is best for tokenholders long-term.”

- 100% buyback of revenue is short-term thinking: HYPE and PUMP are the exception, not the rule. Most early-stage startups need to prioritize growth and building a healthy treasury first, then increase the buyback as the company matures. Take Uber in the early days. A 100% buyback of fees, as they try to expand from San Francisco to nationwide ride-sharing, would be illogical. The same applies here.

- Net profits, not revenues: Businesses need to pay for OpEx: salaries, marketing, legal fees, partnerships, etc. After building an emergency reserve, 100% of net profits (what is left after these expenses) makes the most sense for a team that prioritizes what is best for holders.

- Don’t Pasternak It: Believe App is the perfect example of why hyping up a buyback program hurts more than it helps. I think Hyperliquid and Pump Fun have the best and most regulatory-compliant approach—just start doing it and give the community a dashboard & wallets to track.

- Maker Not Taker: Provide liquidity below the current price, whether in bid form on a CLOB perp DEX or single-sided liquidity band under the current price (maker). Providing liquidity this way reduces painful volatility, dissuades indiscriminate shorting, and helps funds & other large participants participate more comfortably in investment.

- Don’t Burn: The reason why teams burn after buying back is to make FDV look smaller and receive a more attractive valuation. FDV is a flawed metric that we should not kowtow to. What is best for holders is not burning the team’s most important weapon in their arsenal. The optimal approach is to set up an Assistance Fund, where bought-back tokens are removed from circulation and placed in a segregated wallet. The tokens only re-enter in emergency situations.

- Transparency Is The Final Puzzle Piece: Monthly reports of holdings, basic transaction logs, fully on-chain processes, strong communication, and building in public hold this process together. These are basic, reasonable asks for teams that expect the public to hold their tokens long-term.

TLDR:

- The concept of what buybacks are and aren’t has been distorted. It is extremely important to understand these nuances if you want to win in crypto.

- Tokens are experiencing growing pains because the community was taught value equals: Metcalfe’s Law, attention value, network value, and L1s being automatically worth $1B+

- Buybacks create demand in 4 ways: buying, reverse dilution, creating a price floor, and aligning the ecosystem.

- Buybacks correlate the growth of the project to the value of the token

- Expecting 99-100% buybacks of revenue is ridiculous and illogical. How will the business pay bills? 100% of net income (Revenue - OpEx) should be the base expectation. HYPE and PUMP are the exception, not the rule.

- Making a huge announcement about buybacks isn't what matters—doing it is.

- Good riddance to the idea that projects should be solely driven by governance voting. But that comes with the commitment to be very transparent about finances & a commitment to build in public.

.png?width=512&height=405&name=unnamed%20(10).png)